Did you know your credit score can shape your financial future? From unlocking lower interest rates to securing premium loan products, a good credit score can be your golden ticket to financial freedom.

But what happens if managing your credit card payments becomes more challenging?

Starting July 1, customers with credit cards from major banks like HDFC Bank and Axis Bank will no longer be able to use third-party apps like PhonePe, Amazon Pay, and Paytm to settle their credit card bills. This change underscores the importance of having a clear strategy for managing your credit effectively.

Improving your credit score might seem like a daunting task, but it doesn’t have to be. By following simple, actionable tips, you can take control of your finances, build your credit score, and open the door to better opportunities.

Below, we’ll explore ten proven strategies to help you elevate your credit score quickly and confidently.

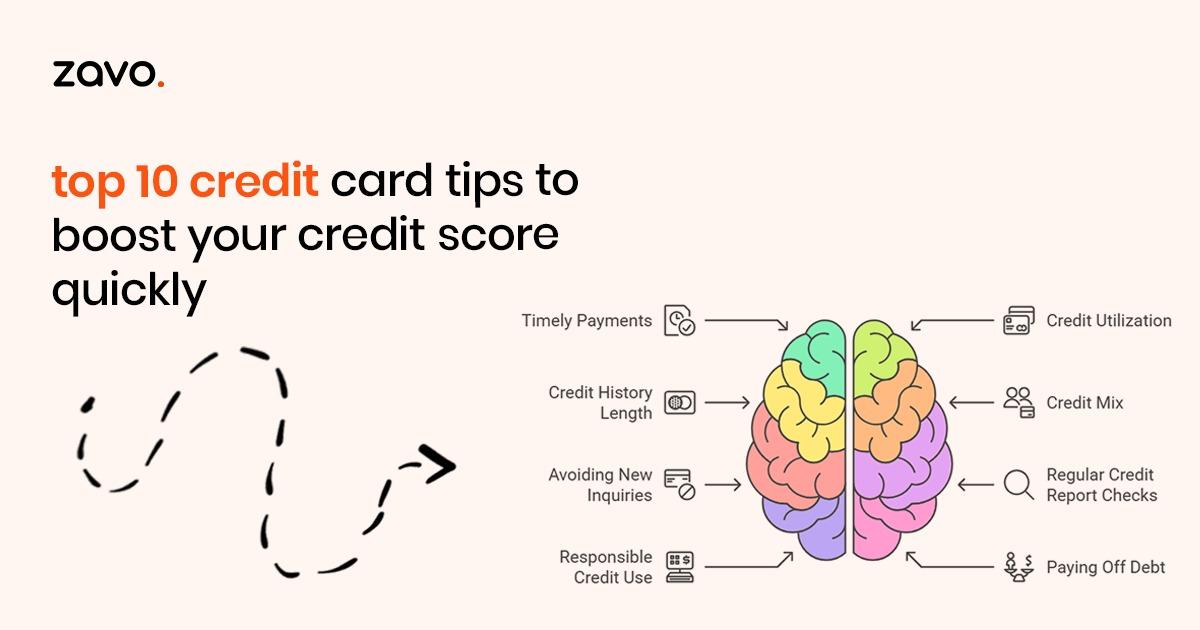

1. Pay Down Revolving Balances Early and Often

One of the fastest ways to increase your credit score is by tackling your credit card balances. Your credit utilization ratio, or the percentage of your available credit that you use, plays a significant role in your score—making up about 30% of it. Keeping your utilization below 30% is ideal, but staying under 10% can result in an even quicker boost.

To achieve this, pay off your credit card balances early and often. Instead of waiting for your statement date, make payments as soon as you’ve charged expenses to your card. You can also make multiple payments within a billing cycle to consistently lower your balance before creditors report it to the bureaus.

Pro Tip: Call your card issuer to learn when they report balances to credit bureaus. This allows you to time your payments strategically and ensure low utilization during reporting periods.

2. Increase Your Credit Limit

A higher credit limit lowers your credit utilization ratio, making it a quick win for your credit score. You can request a credit limit increase on an existing card or open a new credit card account. However, it’s important to use this strategy responsibly—a higher limit is only beneficial if you don’t increase your spending.

To request an increase, reach out to your card issuer via phone or their online portal. Be prepared to provide information about your income or any financial improvements. Alternatively, consider applying for a new credit card with attractive terms to boost your available credit.

Remember, every time you apply for credit, a hard inquiry is added to your credit report, which can temporarily lower your score. To minimize this impact, avoid applying for multiple cards in a short time frame.

3. Review Your Credit Reports for Errors

Errors on your credit report could be silently dragging down your score. In fact, studies show that one in four Americans have at least one error on their report. These errors can include duplicate accounts, incorrect payment histories, or even fraudulent activities.

Take advantage of your right to free annual credit reports from zavo. Review each report thoroughly and look for discrepancies. If you spot an error, dispute it with the relevant credit bureau. Most disputes can be filed online, and the bureaus are required to investigate and resolve disputes within 30 days.

4. Pay Off Collection Accounts

Unpaid collection accounts can have a major negative impact on your credit score. If you have outstanding debts in collections, prioritizing their repayment is crucial. Once paid, contact the collection agency and request that they remove the account from your credit report entirely.

This process, known as a “pay-for-delete” agreement, can be more effective than simply having the account marked as “paid” on your report. Be persistent and polite in your negotiations with the collection agency. Removing paid-off collections from your report can lead to a significant improvement in your credit score.

5. Keep Old Credit Accounts Open

The length of your credit history accounts for 15% of your credit score. Closing old accounts can shorten your average account age and lower your score. Even if you no longer use a particular card, keeping it open can help maintain your credit history.

If the card carries an annual fee, consider downgrading to a no-fee version. Just make sure you use the card occasionally to prevent the issuer from closing it due to inactivity.

6. Set Up Automatic Payments

Late payments are one of the biggest factors that can damage your credit score, with the potential to lower it by 100 points or more. Setting up automatic payments ensures that you never miss a due date, even if life gets busy.

While auto-pay can handle the minimum payment, aim to pay off your balance in full each month to avoid interest charges. Combine auto-pay with email or calendar reminders to check your account balances and stay on top of your finances.

7. Use Secured Credit Cards Wisely

Secured credit cards are an excellent tool for building or rebuilding your credit. They require a deposit, which acts as your credit limit, but they report your payment activity to the credit bureaus just like regular credit cards.

To maximize their benefits, use your secured card for small, manageable purchases and pay off the balance in full each month. Over time, responsible use can help you qualify for unsecured credit cards with better terms.

8. Diversify Your Credit Mix

Your credit score also benefits from having a mix of different types of credit, such as credit cards (revolving credit) and installment loans (like auto loans or mortgages). If you only have one type of credit, consider adding another to your profile.

For example, taking out a small personal loan or financing a purchase with a credit builder loan can demonstrate your ability to manage different forms of credit responsibly. Just be sure not to overextend yourself financially.

9. Avoid Multiple Hard Inquiries

Each time you apply for a credit card or loan, a hard inquiry appears on your credit report. Too many hard inquiries in a short period can signal to lenders that you’re a risky borrower, which may lower your score.

Instead, space out your applications and research credit products thoroughly before applying. Many issuers offer pre-qualification tools that use a soft inquiry, allowing you to check your eligibility without affecting your score.

10. Keep Balances Low on All Cards

While paying down one card is great, don’t overlook balances on your other cards. Credit utilization is calculated across all your accounts, so high balances on one or two cards can still hurt your score.

Distribute your payments across multiple cards to maintain low utilization rates on each. Use budgeting tools to track your expenses and avoid overspending.

Conclusion

Improving your credit score doesn’t have to be overwhelming. By following these actionable credit card tips, you’ll be on your way to a stronger financial future.

Remember, patience and consistency are key. If you’re ready to take charge, zavo offers tools and resources to help you monitor your credit score and achieve your financial goals.