Have you ever wondered how a routine credit check might influence your financial health?

Whether you’re applying for a credit card, securing a home loan, or even renting an apartment, your credit score is often a deciding factor. However, the impact of a credit inquiry goes beyond just a number—it reflects your financial habits and influences how lenders perceive you. Understanding the distinction between hard and soft inquiries is key to managing your credit effectively and safeguarding your score.

In this blog, we will explore the differences between hard pulls and soft pulls, their effects on your credit score, and actionable tips to minimize their impact. By the end, you’ll have a clear strategy for navigating credit inquiries without jeopardizing your financial well-being.

What Are Credit Inquiries?

A credit inquiry occurs whenever someone—be it you, a lender, or a third party—accesses your credit report. Your credit report contains detailed information about your credit history, including your payment patterns, outstanding debts, and the types of credit you’ve used.

Credit inquiries are classified into two types: hard pulls and soft pulls. Hard inquiries, also known as hard pulls, are usually initiated when you apply for credit, such as a loan or credit card. On the other hand, soft inquiries, or soft pulls, occur when your credit is checked for informational purposes, like when you monitor your credit score or get pre-approved for a financial product.

Although both types of inquiries involve accessing your credit report, only hard inquiries can affect your credit score. Knowing when and how these inquiries occur can help you make informed decisions about your financial actions.

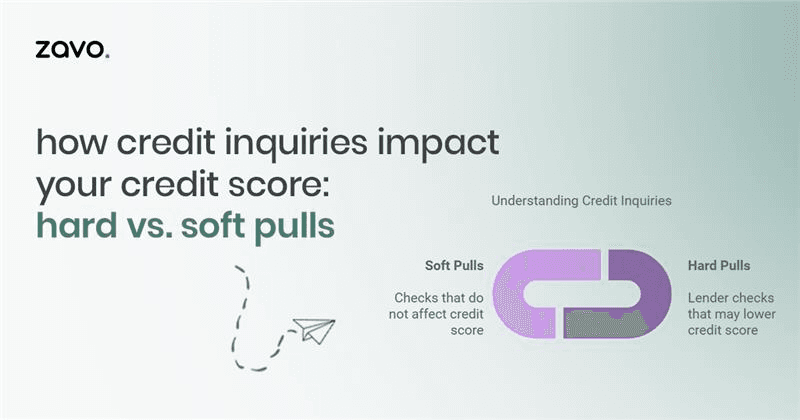

Hard Pulls vs. Soft Pulls: Understanding the Difference

Credit inquiries are classified into two main types: hard pulls and soft pulls, each serving a specific purpose and having a distinct impact on your credit score.

Hard Pulls: The Credit-Seeking Indicator

A hard pull, also called a hard inquiry, is triggered when you apply for a financial product, such as a mortgage, car loan, or credit card. These inquiries are conducted by lenders to evaluate your creditworthiness, helping them decide whether to approve your application.

Hard pulls are significant because they signal to credit bureaus that you are actively seeking credit. As a result, they can temporarily lower your credit score. The reduction is usually minor, around 5 to 10 points, but multiple hard pulls in a short timeframe can compound the effect.

Key points about hard pulls:

They are visible to other lenders on your credit report.

-

The impact on your credit score lasts up to one year, but the inquiry itself remains on your report for two years.

-

Lenders use them to assess the risk associated with lending to you.

Soft Pulls: The Informational Check

In contrast, a soft pull (or soft inquiry) is non-intrusive and does not impact your credit score. These inquiries are often conducted for informational purposes, such as when:

-

You check your own credit report.

-

A lender pre-approves you for a financial product.

-

An employer or landlord performs a background check.

Soft pulls are only visible to you on your credit report and are not shared with lenders, making them harmless to your credit profile.

Key points about soft pulls:

-

They are invisible to lenders and have no impact on your score.

-

Commonly used for pre-qualifications and background checks.

-

Allow you to monitor your credit regularly without negative effects.

The Critical Difference

The primary distinction lies in their visibility and impact:

-

Hard pulls can temporarily lower your credit score and are visible to lenders.

-

Soft pulls have no effect on your score and are private to you.

Because hard pulls carry more weight, it’s essential to be strategic about when and how often you allow them. Properly managing credit inquiries can help you protect your credit score and maintain financial stability.

How Hard Inquiries Affect Your Credit Score?

When a hard inquiry is made, it signals to credit bureaus that you are actively seeking credit. While a single hard pull may only reduce your score by 5 to 10 points, multiple inquiries in a short period can have a compounding effect.

Temporary Impact on Your Score : A hard inquiry’s impact is usually short-lived, affecting your score for about 12 months. However, it stays visible on your credit report for two years, giving potential lenders a broader view of your credit-seeking behavior.

Multiple Inquiries: If you apply for multiple credit cards or loans within a short time, lenders may interpret this as financial instability. To mitigate this risk, credit scoring models like FICO and VantageScore group similar inquiries—such as those for mortgages or auto loans—made within a specific window (typically 14 to 45 days) as a single inquiry. This practice is known as rate-shopping protection and allows borrowers to shop for competitive rates without significant score reductions.

Understanding this can help you plan your credit applications more strategically, avoiding unnecessary hits to your score.

Soft Pulls and Their Role in Credit Checks

Soft inquiries are far less invasive than hard pulls. These credit checks are generally done for informational purposes and do not affect your credit score in any way. They are a great way for individuals and companies to gather insights without impacting financial health.

Soft pulls occur in situations such as:

-

Checking Your Own Credit Score: Regular monitoring helps you stay on top of your financial health.

-

Pre-Approved Credit Offers: Lenders may check your credit to determine your eligibility for pre-approved offers.

-

Background Checks: Employers and landlords may conduct soft inquiries to evaluate your reliability.

Unlike hard inquiries, soft pulls are only visible to you when you review your credit report, ensuring that lenders cannot see these checks.

Why Too Many Hard Inquiries Can Raise Concerns?

While one or two hard inquiries may only cause a slight dip in your score, a pattern of frequent hard pulls can raise red flags for lenders.

Lenders’ Perspective on Multiple Inquiries: Too many hard inquiries can make you appear financially overextended or desperate for credit. Lenders may view this as a sign of risk, which could result in higher interest rates or even credit denials.

Timing Matters: If you are planning a major purchase that requires a credit check—such as buying a home or car—try to limit other credit applications around the same time. This helps preserve your credit score and makes you a more attractive borrower.

Tips to Minimize the Impact of Credit Inquiries

1. Be Selective About Credit Applications: Before applying for credit, research lenders and their requirements. Pre-qualifying for loans or credit cards can help you determine eligibility without triggering hard inquiries.

2. Monitor Your Credit Regularly: Use free or paid credit monitoring tools to track your credit health. Checking your score frequently (via soft pulls) helps you identify and address issues proactively.

3. Time Your Applications Strategically: If you’re shopping for loans, aim to submit all applications within the inquiry window offered by credit scoring models. This ensures that multiple hard inquiries are treated as one.

4. Strengthen Your Credit Profile: A strong credit history can buffer the impact of hard inquiries. Focus on maintaining low credit utilization, making timely payments, and diversifying your credit mix.

Recovering from the Effects of Hard Inquiries

If recent hard inquiries have caused a dip in your credit score, don’t worry—it’s not a permanent setback. With the right financial habits and some patience, you can recover and even strengthen your credit profile. Here are key strategies to help you bounce back:

1. Make On-Time Payments: Your payment history is the single most influential factor in your credit score, accounting for 35% of it. To recover from the effects of hard inquiries, it’s crucial to ensure that all your bills—credit cards, loans, or utilities—are paid on time. Late payments not only damage your score further but also make it harder to regain lender confidence. Establish reminders or automate payments to stay consistent.

2. Reduce Credit Utilization: Credit utilization, or the percentage of your credit limit that you’re using, is another vital component of your score. High balances on credit cards can signal financial stress to lenders, which might compound the negative impression of multiple hard inquiries. Aim to keep your credit utilization below 30% of your total credit limit. Paying down outstanding balances and avoiding unnecessary spending can help improve this metric quickly.

3. Hold Off on New Credit Applications: While it might be tempting to apply for additional credit, doing so immediately after hard inquiries can harm your score further. Each new hard inquiry can lower your score slightly, so it’s best to give your credit profile time to stabilize. Lenders tend to look more favorably on applicants who haven’t sought new credit recently, so pausing applications for a few months can enhance your credibility.

4. Patience and Consistency Pay Off: Hard inquiries have a diminishing impact over time, usually affecting your score most during the first 12 months. Beyond that period, their influence lessens, and they drop off your credit report after two years. By maintaining healthy financial habits—such as responsible borrowing, timely payments, and low credit utilization—you can offset the effects of hard inquiries and steadily improve your credit score.

Remember, rebuilding your credit is a gradual process. By focusing on these strategies, you not only recover from hard inquiries but also build a stronger, more resilient credit profile for the future.

Conclusion

Credit inquiries are an essential part of your financial journey, but managing them wisely can help you maintain a healthy credit score. Always consider whether a hard inquiry is necessary and look for opportunities to pre-qualify using soft inquiries.

By staying informed, timing your applications carefully, and focusing on good credit habits, you can minimize the impact of credit inquiries and ensure your financial health stays strong. After all, your credit score is more than just a number—it’s a reflection of your financial responsibility.

Ready to take control of your credit health? With zavo, you can monitor your credit score, receive personalized tips to improve it, and track your progress—all without affecting your score. Join the thousands of users who trust zavo to simplify credit management. Download the zavo app today and start your journey toward financial empowerment!

Frequently Asked Questions (FAQs)

1. How much does a hard inquiry lower my credit score?

A single hard inquiry can lower your credit score by 5 to 10 points, depending on your credit history.

2. How long do hard inquiries stay on my credit report?

Hard inquiries remain on your report for two years but only affect your score for the first year.

3. Can soft inquiries be seen by lenders?

No, only you can see soft inquiries when reviewing your credit report.

4. What happens if I shop for multiple loans in a short period?

If done within the allowed timeframe (14 to 45 days), multiple inquiries for the same loan type are treated as one.

5. Can I dispute a hard inquiry?

Yes, if the inquiry is unauthorized, you can file a dispute with the credit bureau to have it removed.