Credit cards are evolving rapidly to keep pace with the needs of modern consumers.

One of the latest trends is the rise of UPI-enabled credit cards, which have seen a staggering 20% monthly growth and average around 40 transactions per user.

These cards combine the convenience of Unified Payments Interface (UPI) with the benefits of credit, offering unparalleled flexibility and rewards.

In this blog, we’ll break down how to choose the best credit card that aligns with your financial goals, leveraging these innovations and more.

What Are Credit Cards?

A credit card is a financial tool that allows you to make purchases now and pay later. Beyond convenience, credit cards often come with benefits like rewards points, cash back, and travel perks. However, to unlock their full potential, you must use them responsibly - paying balances in full every month to avoid interest charges.

Proper credit card usage not only avoids debt but also helps build a strong credit history, opening doors to better financial opportunities.

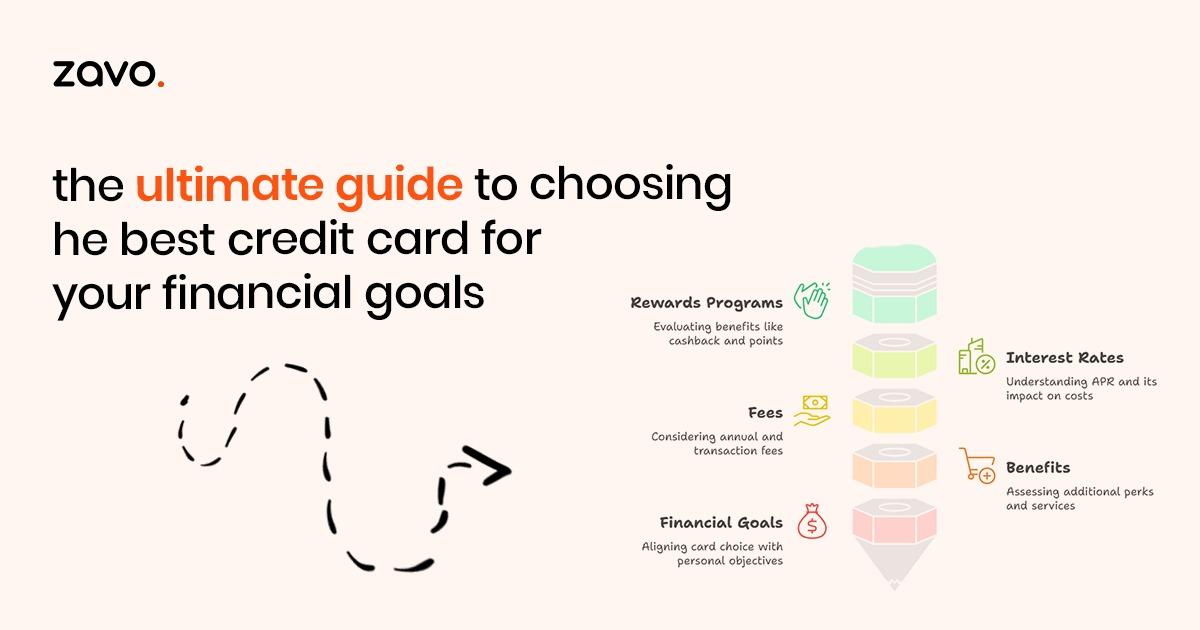

8 Key Tips for Choosing the Right Credit Card

1. Set Financial Goals

Your financial goals should dictate your choice of a credit card. Are you looking to improve your credit score, save on interest, or earn rewards? Analyze your spending habits. For instance, if most of your money goes toward dining or travel, prioritize cards with rewards in those categories. Travel-focused cards can save frequent travelers up to Rs.300 annually in perks like free lounge access, complimentary travel insurance, and more. Identifying your primary financial objectives will narrow down your options and ensure the card you choose aligns perfectly with your lifestyle.

2. Check Your Credit Score

Your credit score determines your eligibility for credit cards and influences the interest rates you’re offered. If your score is below 750, focus on improving it by paying bills on time, reducing outstanding debt, and limiting new credit inquiries. Many financial tools, like zavo, allow you to check your score for free. With a higher credit score, you can qualify for cards that offer better rewards, lower interest rates, and higher credit limits.

3. Compare Interest Rates

Interest rates, or APRs, vary significantly among credit cards. If you carry a balance month-to-month, opt for a card with a low APR to save on interest charges. The average credit card APR in 2024 is 20.09%, but some low-interest cards offer rates as low as 12%. However, if you pay off your balance in full every month, interest rates may not be a primary concern. Consider your payment habits before prioritizing interest rates.

4. Evaluate Rewards Programs

Reward cards offer incentives like cash back, travel points, or discounts on specific categories. Enhanced rewards for travel and dining, making them ideal for frequent travelers. If you spend more on groceries or fuel, select a card that maximizes rewards in those areas. Always quantify the rewards against your spending to ensure you’re getting value for your money.

5. Factor in Additional Benefits

Beyond rewards, some credit cards provide valuable perks such as extended warranties, travel insurance, concierge services, and priority boarding. For instance, premium cards often offer benefits like free checked bags or airport lounge access, which can be worth hundreds of dollars annually. Before choosing a card, assess whether these benefits align with your lifestyle. For example, if you rarely travel, lounge access may not be a valuable perk.

6. Assess Annual Fees

While some credit cards are free, others come with annual fees. Weigh the fee against the card’s benefits to determine its value. For instance, if a card’s annual fee is ₹5,000 but it offers ₹20,000 worth of travel rewards annually, the fee is justified. However, if you don’t utilize the card’s perks, it’s better to opt for a no-annual-fee alternative.

7. Consider Credit Limits

Credit limits vary based on the card and your creditworthiness. A higher credit limit can be beneficial for frequent spenders, as it helps maintain a low credit utilization ratio —a key factor in maintaining a strong credit score. However, avoid overspending simply because you have a higher limit. Always stay within a budget and use credit responsibly.

8. Look for Easy Application Processes

Choose a card issuer that offers a seamless digital application process. Many banks now allow online applications with just basic details like PAN, mobile number, and e-KYC. This not only saves time but also ensures a smoother experience from application to approval.

Benefits of Using the Right Credit Card

Choosing the right credit card isn’t just about rewards; it’s about aligning with your financial habits. Here are some key benefits

- Improved Credit Score: Using a card responsibly builds your credit profile over time.

- Savings on Everyday Expenses: Cashback programs can save up to 5% on groceries or fuel.

- Convenience and Security: Credit cards offer fraud protection and easy tracking of expenses.

Conclusion

The right credit card can simplify your financial life, boost your credit score, and unlock rewards that enhance your lifestyle. By assessing your spending patterns, credit score, and financial goals, you can find a card that maximizes benefits and minimizes costs. Remember, responsible usage is the cornerstone of credit card success. Never spend beyond your means and always pay your bills on time.

Need Guidance? Get in Touch with Experts Today!