Have you ever wondered how your spending habits on credit cards affect your overall financial health?

One crucial factor that plays a significant role in your credit score is credit utilization. Understanding this concept can be the key to unlocking better interest rates and more favorable loan terms.

In this blog, we’ll explore what credit utilization is, how it impacts your credit score, and actionable tips to manage it effectively.

What is Credit Utilization?

Credit utilization refers to the ratio of your outstanding credit card balances to your total available credit. It is calculated by dividing your total credit card balances by your total credit limits across all your credit cards. This percentage reflects how much of your available credit you are currently using and is a crucial factor in determining your credit score.

How to Calculate Credit Utilization?

Calculating your credit utilization is straightforward. For example, if you have two credit cards—one with a limit of $5,000 and another with a limit of $3,000—and your current balances are $1,000 and $500 respectively, your total credit card balances would be $1,500, and your total credit limits would be $8,000. In this case, your credit utilization rate would be 18.75%.

Why Does Credit Utilization Matter?

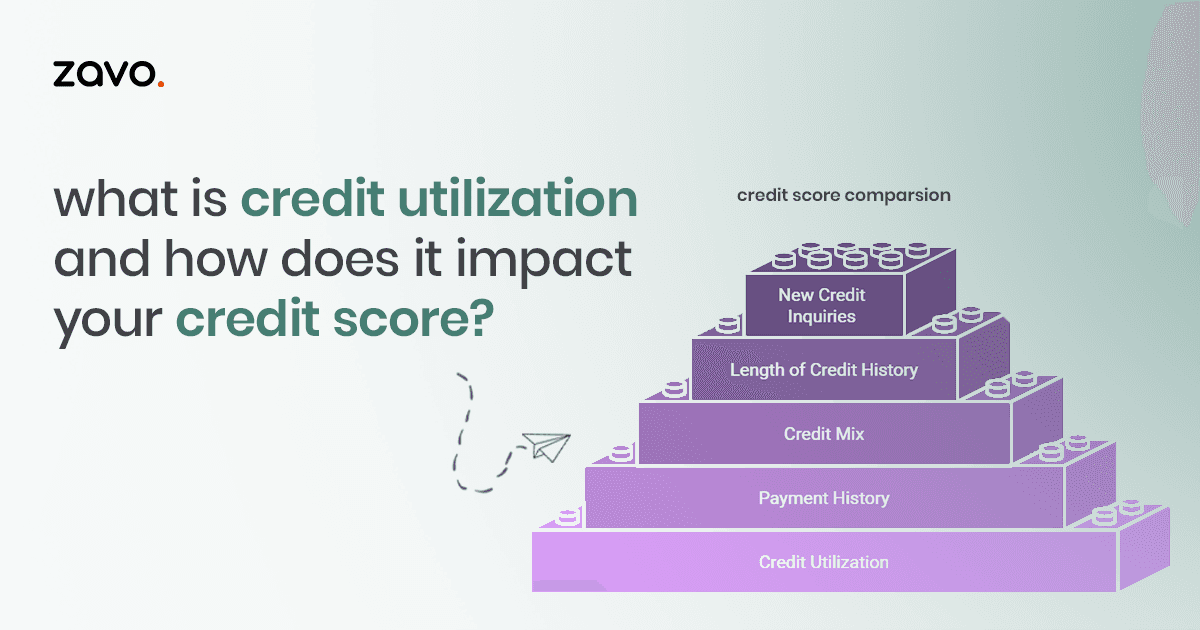

Credit utilization is one of the most significant factors influencing your credit score, accounting for about 30% of the score calculation. Lenders view credit utilization as an indicator of your financial behavior and ability to manage debt. Here’s how it impacts your credit score:

-

Indicates Financial Responsibility:

A lower credit utilization ratio suggests that you are not overly reliant on credit and can manage your finances effectively. Conversely, a high utilization rate can indicate that you may be over-leveraged or struggling to keep up with payments.

-

Influences Risk Assessment:

Lenders use credit scores to assess risk. If your utilization is high, it may signal to lenders that you are at a higher risk of defaulting on loans, which could lead to higher interest rates or even denial of credit.

-

Affects Your Credit Score:

High credit utilization can lead to a lower credit score, while maintaining a lower utilization rate can help boost your score. Keeping your utilization under 30% is generally considered good practice, but the lower, the better.

The Ideal Credit Utilization Rate

While the general guideline is to keep your credit utilization below 30%, many financial experts recommend aiming for a rate of 10% or lower for optimal credit health. A lower utilization rate shows that you are managing your credit responsibly and not relying heavily on borrowed funds.

Another important detail many borrowers overlook is that credit utilization is calculated both per card and across all cards combined. Even if your overall utilization is low, maxing out a single credit card can still negatively impact your credit score. Lenders and credit bureaus evaluate how you manage each account individually, so spreading balances evenly and keeping every card’s utilization low is a smart way to protect your score.

Example of Ideal vs. Poor Utilization

Ideal Utilization: Let’s say you have a total credit limit of $10,000 across all your credit cards and a balance of $800. This rate of 8% is considered excellent and can positively impact your credit score.

Poor Utilization: Now, if your balance increases to $3,500 with the same credit limit, your credit utilization would be 35%. This rate is above the recommended threshold and can negatively affect your score.

How Credit Utilization Is Calculated Per Card vs Overall

Credit utilization is calculated both for each individual credit card and across all cards combined. Even if your total utilization is low, using a high percentage of one card’s limit can still negatively affect your credit score. Credit bureaus and lenders assess how responsibly you manage every account, not just your overall credit. Keeping utilization low on each card helps maintain a stronger and more stable credit profile.

Tips for Managing Credit Utilization

To maintain a healthy credit utilization ratio and improve your credit score, consider the following strategies:

-

Pay Your Balances in Full: Whenever possible, pay off your credit card balances in full each month. This practice helps keep your utilization low and avoids interest charges.

-

Make Multiple Payments: If you can’t pay off your entire balance, consider making multiple payments throughout the month. This can help reduce your reported balance before your statement date.

-

Increase Your Credit Limits: If you have a good payment history, consider requesting a credit limit increase on your existing cards. This action can lower your utilization rate without changing your spending habits.

-

Keep Old Accounts Open: Lengthening your credit history by keeping older accounts open can positively impact your score. Closing older accounts reduces your total available credit, which may increase your utilization rate.

-

Monitor Your Credit Regularly: Regularly check your credit report and score to track your utilization rate. This awareness allows you to take proactive steps to improve your financial health.

The Consequences of High Credit Utilization

If you consistently maintain a high credit utilization rate, you may face several consequences:

-

Lower Credit Scores: As mentioned, a high utilization rate can significantly lower your credit score, making it harder to obtain loans or credit at favorable terms.

-

Higher Interest Rates: Lenders may view you as a higher-risk borrower if your credit utilization is consistently high. This perception can lead to higher interest rates on loans and credit products.

-

Difficulty in Approval: A poor credit score due to high utilization can lead to denial of credit applications, especially for significant loans such as mortgages or auto loans.

-

Increased Financial Stress: High credit utilization can signal financial strain, potentially leading to increased stress and difficulty in managing debt.

How Credit Utilization Affects Different Types of Credit?

Credit utilization is not only essential for credit cards; it can also impact other forms of credit, such as personal loans, auto loans, and mortgages.

Credit Cards: For credit cards, the utilization ratio is often scrutinized the most. Keeping this ratio low can help maintain a healthy credit score and improve the chances of getting approved for more credit in the future.

Installment Loans: While credit utilization primarily applies to revolving credit accounts (like credit cards), having high balances on installment loans can also impact your overall credit profile. Lenders may consider your total debt load when assessing your creditworthiness.

Mortgages: For mortgages, while the credit utilization rate is less of a factor compared to payment history and length of credit history, having a lower utilization can still contribute to a better credit score, which can affect the interest rate you receive on your mortgage.

Conclusion

Credit utilization is a critical aspect of your credit health that directly impacts your credit score. By understanding what credit utilization is and how it works, you can take proactive steps to manage it effectively. Keeping your utilization low not only helps maintain a healthy credit score but also opens doors to better financing options and interest rates in the future. Remember, financial responsibility is key; manage your credit wisely to secure a prosperous financial future.

Frequently Asked Questions (FAQs)

What is a good credit utilization ratio?

A good credit utilization ratio is typically considered to be below 30%. For optimal credit health, aim for a ratio of 10% or lower.

How often should I check my credit utilization?

It’s advisable to check your credit utilization monthly or before applying for new credit. This way, you can manage it effectively and make necessary adjustments.

Does closing a credit card affect my credit utilization?

Yes, closing a credit card can reduce your total available credit, which may increase your credit utilization ratio if you have existing balances on other cards.

Can I improve my credit score by lowering my credit utilization?

Absolutely! Lowering your credit utilization can lead to an improved credit score, as it reflects responsible credit management.

How long does it take for changes in credit utilization to affect my credit score?

Changes in credit utilization can impact your credit score relatively quickly, often within one billing cycle, as long as the new utilization rates are reported to the credit bureaus.