Imagine walking into a bank, confident and ready to apply for a loan, only to be told that your credit score isn't good enough. Frustrating, right? Your credit score is like a financial report card and it determines whether you get approved for loans, credit cards, or even a new house rental. The higher your score, the better your financial opportunities.

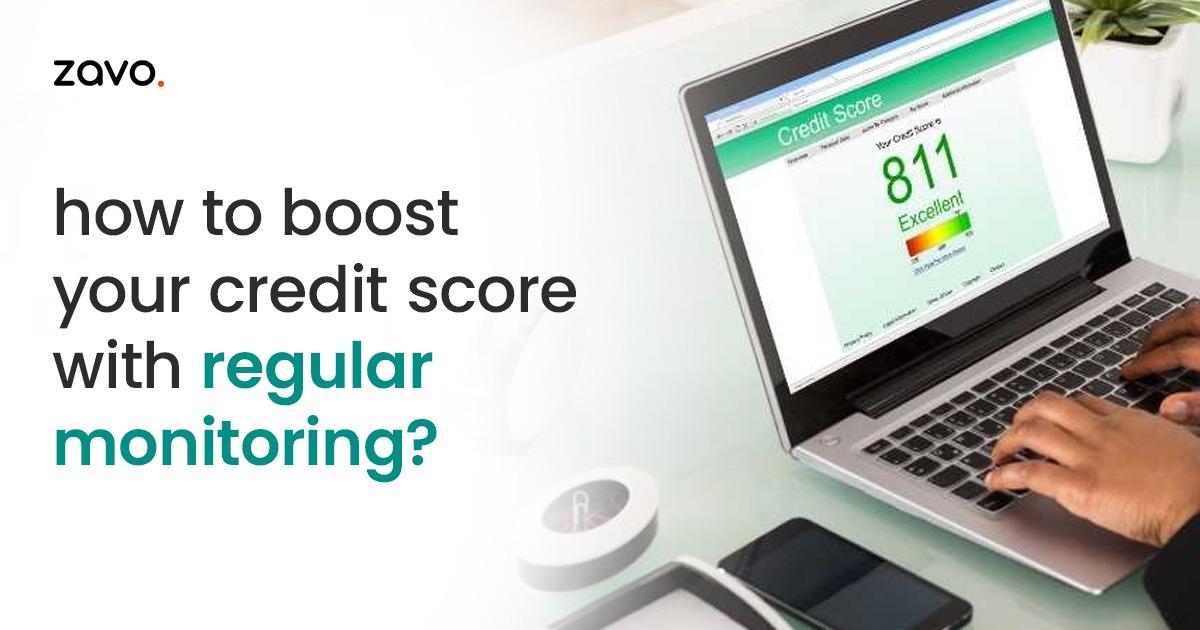

But here’s the good news: improving your credit score isn’t rocket science! Regular credit monitoring can help you identify issues, fix errors, and adopt smart financial habits that gradually push your score up. Think of it as checking your fitness tracker and staying on top of your credit health ensures you’re always in good financial shape.

In this blog, we’ll uncover why monitoring your credit is essential, how it impacts your financial well being, and the best strategies to give your score a well deserved boost!

1. Understanding Your Credit Score

Before you can improve your score, you need to understand how it’s calculated. In India, credit scores are maintained by credit bureaus like CIBIL, Experian, Equifax, and CRIF High Mark. The score usually ranges from 300 to 900, with 750+ being considered excellent.

Factors that Influence Your Credit Score :

- Payment History (35%) – This is the most crucial factor. If you consistently pay your bills on time, your score will improve. However, even a single late payment can significantly impact your credit rating.

- Credit Utilization (30%) – Using too much of your available credit limit signals financial stress to lenders and can lower your score. Keeping utilization below 30% of your credit limit is recommended.

- Credit Age (15%) – The longer your credit history, the better it is for your score. This is why maintaining old credit accounts is beneficial.

- Credit Mix (10%) – A variety of credit types, such as secured (home, car loans) and unsecured loans (personal loans, credit cards), helps demonstrate responsible credit behavior.

- New Credit Inquiries (10%) – Frequent loan or credit card applications result in hard inquiries, temporarily lowering your score.

Pro Tip: Check your credit score at least once every three months to track progress and identify potential issues early.

2. Identifying and Correcting Errors

Errors in your credit report can unnecessarily drag down your score. Even a minor mistake like a wrongly reported late payment or an account you didn’t open can have a negative impact.

How to Spot and Fix Errors:

- Obtain a free credit report from a recognized credit bureau.

- Check for incorrect personal details, payment discrepancies, or fraudulent accounts.

- Raise a dispute with the credit bureau and your bank if you spot any errors.

- Follow up to ensure corrections are reflected in your report.

Around 20% of consumers find errors on their credit reports that lower their scores

3. Monitoring Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you’re using compared to your total credit limit. A high ratio signals financial stress and negatively affects your score.

Steps to Maintain an Optimal Credit Utilization Ratio:

- Keep credit card utilization below 30% of your total limit.

- If you have a high utilization rate, request a credit limit increase to lower the percentage.

- Pay off outstanding balances before the due date.

- Distribute expenses across multiple credit cards instead of maxing out one card.

- Avoid making large purchases on your credit card unless you can repay them immediately.

Example: If your total credit limit is ₹1,00,000, keep usage below ₹30,000 per month for a healthy credit score.

4. Making Timely Bill Payments

Timely payments make up the biggest chunk of your credit score (35%). Missing due dates, even by a day, can seriously damage your score.

How to Ensure On Time Payments:

- Automate payments through your bank to never miss a deadline.

- Set up payment reminders via SMS or email.

- Use your credit card’s billing cycle smartly and plan expenses around the due date to avoid high outstanding balances.

- Prioritize paying at least the minimum due amount to avoid a negative impact on your score.

- Make multiple small payments throughout the billing cycle instead of a lump sum at the end.

A single missed payment can drop your credit score by 50 to 100 points.

5. Avoiding Too Many Loan Applications

Every time you apply for a credit card or loan, lenders conduct a hard inquiry, which temporarily reduces your credit score. Too many inquiries in a short time can make you seem like a risky borrower.

How to Manage Credit Applications Wisely:

- Apply only for credit you genuinely need.

- Avoid applying for multiple credit cards or loans simultaneously.

- Use a loan eligibility checker before applying to avoid rejections that could hurt your score.

- If denied a loan, wait before reapplying and work on improving your creditworthiness first.

If you need a loan, consider zavo, which offers quick approvals without excessive hard inquiries.

6. Diversifying Your Credit Portfolio

Lenders prefer borrowers with a healthy mix of credit types. If your credit profile only includes credit cards, consider adding a secured loan to show better repayment behavior.

Good Credit Mix Examples:

✅ Credit Card + Personal Loan

✅ Home Loan + Car Loan

✅ Secured Loan + Small Credit Card Usage

- Avoid depending only on one type of credit and diversification improves your score over time.

- Do not take unnecessary loans just for credit mix; balance is key.

7. Keeping Old Credit Accounts Active

Older accounts positively impact your credit score, as they reflect a long history of responsible borrowing.

How to Benefit from Credit Age:

- Don’t close old credit cards even if you don’t use them frequently.

- Keep your oldest account active by making small transactions and paying them off immediately.

- Avoid transferring debt from old accounts to new ones unless necessary.

- The longer your credit history, the better lenders perceive you.

Conclusion

We hope this blog has helped you understand how regular credit monitoring can boost your credit score. Whether you’re working towards better loan options or financial stability, zavo makes credit management easier.

With expert tools and insights, we help you track, improve, and maintain a strong credit profile effortlessly. Don’t let a low score hold you back and start monitoring today and take control of your credit health!

Get started with zavo and build a stronger credit future today!

Frequently Asked Questions (FAQs)

1. How often should I check my credit score?

Ideally, every 3-6 months to monitor changes and detect errors early.

2. Can checking my credit score lower it?

No, checking your own credit score is considered a soft inquiry and does not impact your score.

3. What’s the fastest way to improve my credit score?

Pay bills on time, keep credit utilization low, and avoid unnecessary loan applications.

4. How long does it take to see improvements in my credit score?

Depending on your financial behavior, positive changes can reflect within 3-6 months.

5. Which credit bureau is the most reliable in India?

CIBIL, Experian, Equifax, and CRIF High Mark are all widely recognized credit bureaus in India.