Your credit score is like a financial report card—are you acing it, or are you falling behind?

Many people don’t realize how much their credit impacts their financial health until they apply for a loan, a credit card, or even a mortgage.

A good credit score can open doors to better financial opportunities, while a poor score can limit your options and cost you more in interest over time.

But what exactly is credit, and how does it affect your financial well-being? Let’s break it down in simple terms.

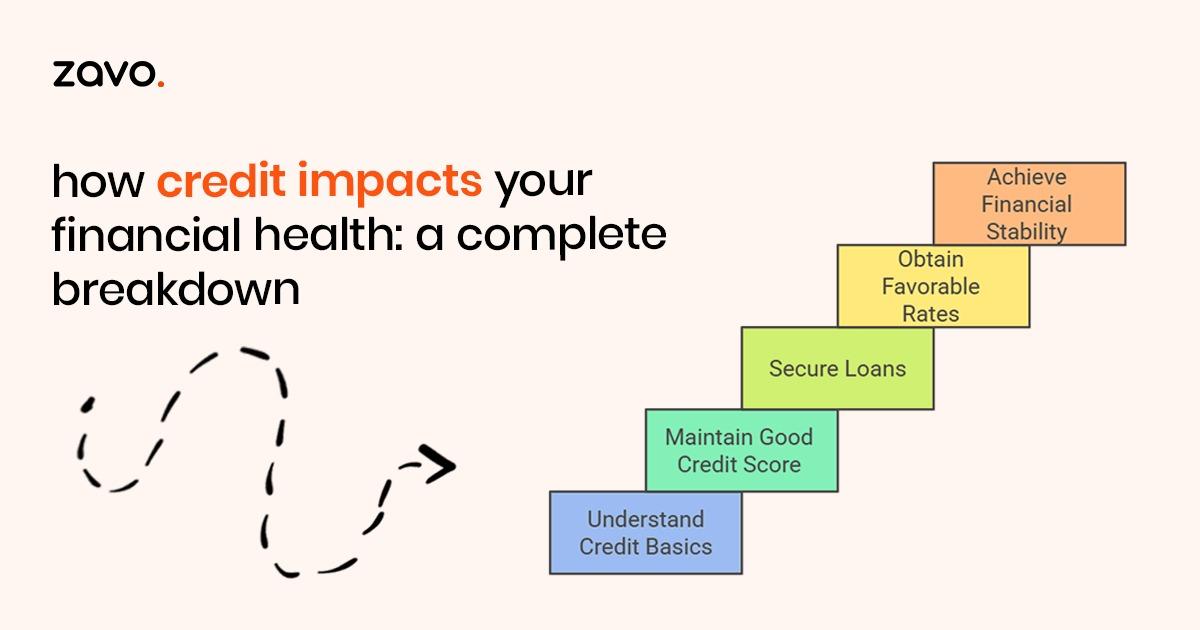

1. What is a Credit Score, and Why Does It Matter?

Your credit score is a three-digit number that represents your creditworthiness. It ranges from 300 to 900, with higher scores indicating a lower risk to lenders. Think of it as your financial reputation—lenders use this score to decide whether to approve your applications for loans, credit cards, and even rental agreements.

If your score is in the higher range (typically above 750), you’ll enjoy perks like lower interest rates, faster approvals, and access to premium financial products. On the other hand, a lower score can mean higher interest rates or outright rejections, making financial growth more challenging.

2. The Role of Credit in Managing Financial Products

Good credit management leads to more favorable terms on financial products like loans and credit cards. For example, if you have an excellent credit score and apply for a 30-year mortgage of Rs.200,000, you might secure an interest rate of 3.3%, resulting in lower monthly payments. Conversely, a lower credit score could mean an interest rate of 5% or more, increasing your financial burden by thousands over the loan’s lifespan.

Your credit score also determines whether you qualify for premier credit cards with higher limits and better rewards. These cards often come with perks like cashback, travel rewards, and exclusive deals that can make your spending more efficient.

3. Components of Your Credit Score

Understanding how your credit score is calculated can help you take control of it. The five main components are:

a) Payment History (35%)

Your payment history is the most significant factor in your credit score. It tracks whether you pay your bills on time. Even one late payment can negatively affect your score, so consistency is key.

b) Credit Utilization (30%)

This measures how much of your available credit you’re using. A good rule of thumb is to keep your utilization below 30%. For example, if you have a total credit limit of $10,000, aim to use no more than $3,000 at any given time.

c) Length of Credit History (15%)

The longer you’ve been using credit responsibly, the better. Older accounts show lenders that you’re experienced in managing credit.

d) Credit Mix (10%)

Lenders like to see a variety of credit types, such as credit cards, installment loans, and mortgages. Having a balanced mix demonstrates that you can handle different forms of credit.

e) New Credit (10%)

Each time you apply for credit, a hard inquiry is added to your report, which can slightly lower your score. Avoid opening multiple accounts in a short period to keep your score stable.

4. How Credit Affects Your Financial Health

Your credit score impacts almost every financial decision. Here are some ways it directly affects your financial health:

- Loan Approvals: Higher credit scores increase your chances of approval for personal loans, car loans, and mortgages.

- Interest Rates: A good credit score can save you thousands of dollars over the life of a loan by securing lower interest rates.

- Insurance Premiums: In some cases, insurers check credit scores to set premium rates.

- Employment Opportunities: Certain employers may review credit reports as part of their hiring process.

5. What Hurts and Helps Your Credit Score

What Hurts:

- High credit utilization.

- Applying for multiple credit accounts in a short period.

- Defaulting on loans or declaring bankruptcy.

What Helps:

- Making timely payments.

- Keeping credit utilization low.

- Maintaining a long credit history.

- Diversifying your credit mix.

Your credit score is a vital part of your financial health, influencing everything from loan approvals to the cost of borrowing. Fortunately, it’s never too late to start improving it. By adopting smart credit habits, such as making timely payments and keeping your credit utilization low, you can steadily build a stronger financial foundation.

At zavo, we’re here to help you monitor and improve your credit score. With tools and resources designed to simplify credit management, you can take charge of your financial future. Start your journey to better credit today and unlock the financial opportunities you deserve!

Frequently Asked Questions (FAQs)

1. How often should I check my credit score?

It’s a good practice to check your credit score at least once every quarter to ensure accuracy and monitor any changes.

2. Will checking my own credit score hurt it?

No, checking your own credit score is a soft inquiry and does not affect your score.

3. How can I improve my credit score quickly?

Pay down outstanding balances, avoid late payments, and dispute any errors on your credit report.

4. Does closing old accounts improve my score?

No, closing old accounts can actually lower your score by shortening your credit history and increasing your credit utilization.

5. How long does negative information stay on my report?

Most negative items, such as late payments, remain on your credit report for seven years.