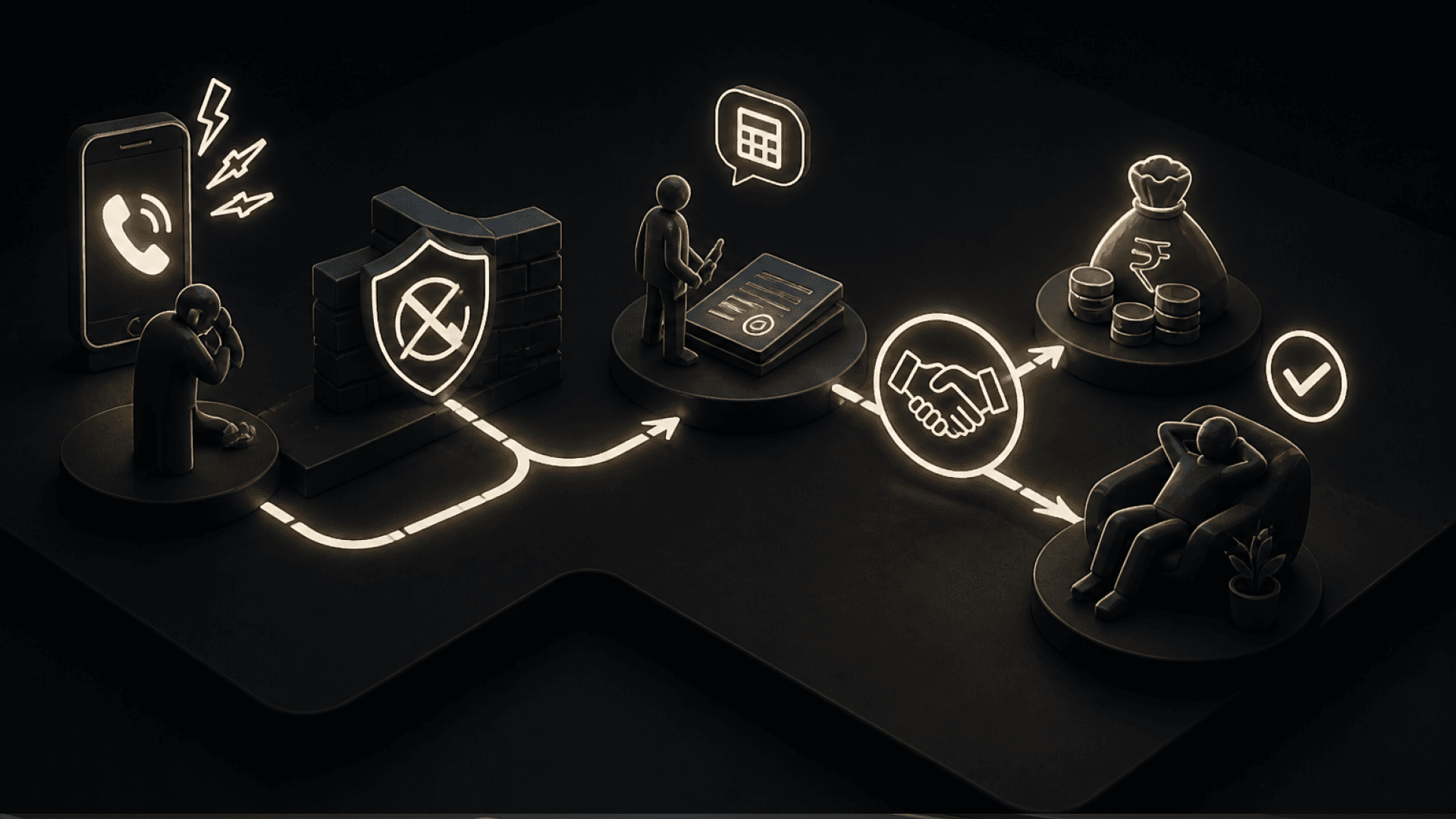

Quick answer: A recovery agent has legal limits; they can only call you between 8 AM and 7 PM and cannot threaten or harass you. The most reliable way to stop these calls for good is loan settlement: a legal agreement to close your loan for a reduced amount your lender accepts. Platforms like Zavo Settle help borrowers settle directly with lenders with no fees, no middlemen so the account closes and the calls end.

The phone rings at 7 AM. Again at lunch. By evening, a recovery agent is messaging your family. If this sounds familiar, you're not alone and you're not without options.

Here's what most borrowers never hear: recovery agents operate under strict RBI rules. They cross those lines often, but you have rights. And when your loan is legally closed through settlement, the calls stop because there's nothing left to recover.

What Is a Recovery Agent and What Are Their Legal Limits?

A recovery agent is a third party hired by banks to recover overdue loan amounts. They contact you by phone, message, or home visit. But the RBI sets firm limits on what they can do:

- Can only contact you between 8:00 AM and 7:00 PM. Outside this window counts as harassment.

- Cannot use threats, abusive language, or physical force.

- Cannot contact you during festivals or mourning periods.

- Cannot disclose your debt to your employer, neighbors, or family.

If a recovery agent breaks these rules, file a complaint with your bank's grievance cell or the RBI Ombudsman. Many borrowers tolerate harassment simply because they don't know where the line is.

Why Do Recovery Calls Escalate?

The first missed EMI triggers a reminder. Miss two or three, and your account moves toward being classified as a Non-Performing Asset (NPA) generally after 90 days. That's when lenders hand things over to recovery teams and call volume spikes.

The triggers are rarely careless spending. Job loss, medical emergencies, and rising EMIs push responsible borrowers into default. India's household debt reached 41.9% of GDP by end-December 2024, and unpaid credit card bills rose 44% in one year. Ignoring the calls doesn't make them stop, it makes them worse. Closing the account does.

What Is Loan Settlement and How Does It Provide EMI Relief?

Loan settlement is a negotiated agreement where your lender accepts a one-time lump-sum payment usually less than the full amount owed to permanently close your account. The RBI formally supports this through its One-Time Settlement (OTS) guidelines.

How settlement delivers real EMI relief:

- You stop the EMI cycle entirely. One final payment, and the loan is done.

- You pay less than you owe. Lenders often accept 40–60% of the outstanding principal on defaulted accounts.

- The account is legally closed. You receive an NOC or settlement letter. No more EMIs. No more recovery calls.

Settlement does mark your loan as "Settled" on your credit report, which affects your score. But it's far better than staying in prolonged default.

What Happens When You Skip EMI Payments?

Skipping one EMI triggers a late fee. Skip a few more, and things escalate quickly:

1 - Late penalties and rising interest inflate your total debt.

2 - Your credit score drops with each missed payment.

3 - Your account is classified as an NPA after roughly 90 days.

4 - Recovery agents step in, increasing calls and visits.

There is a silver lining: once in default, you become eligible for settlement. Lenders are more willing to negotiate a reduced payoff on a defaulted account and this is where a structured settlement turns a tough situation into a clean exit.

How Can a Loan Settlement Expert Help?

Facing a recovery agent alone is stressful. A loan settlement expert changes the dynamic. They understand lender behavior, RBI rules, and the realistic range a bank will accept. Here's what they bring:

- Knowledge of your rights - and how to push back on illegal harassment.

- Negotiation leverage - knowing what lenders will realistically accept.

- Proper documentation - ensuring you get a valid NOC so the account stays closed.

Instead of reacting to pressure, you follow a clear plan toward closure.

How Does Zavo Settle Help You Stop Recovery Agent Pressure?

Zavo Settle is India's loan and credit card settlement platform built for borrowers who want to resolve dues directly with lenders, without agents, middlemen, or hidden fees.

What sets Zavo Settle apart:

- No middlemen. You negotiate directly with the lender. Zavo just facilitates.

- 97% success rate. Near-97% settlement success across its user base.

- Up to 2% cashback on every successful settlement.

- Trusted by 30 lakh+ borrowers, rated 4.3/5.

- Covers personal loans, home loans, and credit cards.

Once your account is settled and closed, the recovery agent calls have no reason to continue.

Step-by-Step: How to Settle Your Loan With Zavo

Step 1: Select Your Account - Choose the loan or credit card you want to settle and fill in basic details.

Step 2: Enter Your Settlement Offer - Set an amount you can genuinely afford. This is your opening offer to the lender.

Step 3: Lender Reviews the Offer - Zavo submits your offer. The lender evaluates based on account age, default status, and recovery benchmarks.

Step 4: Settle and Close the Account - Once approved, complete the payment. The account closes, you receive confirmation, and the recovery pressure ends.

Some borrowers complete settlements within days of submitting their offer.

Take Back Your Peace of Mind

A recovery agent thrives on pressure. But you have rights, and you have a legal way out. The moment your loan is settled and closed, the calls lose their reason to exist.

Loan settlement is a structured, lender-approved resolution for borrowers in or approaching default. It closes the account, ends the harassment, and gives you space to rebuild.

Zavo Settle makes it simple: no agents taking a cut, no hidden fees, just a direct process between you and your lender.

Visit Zavo Settle to check which accounts are eligible and submit your first settlement offer today.

Frequently Asked Questions

1. Can recovery agents call me at any time of day?

No. RBI rules allow recovery agents to contact you only between 8 AM and 7 PM. Calls outside these hours, or any threats, count as harassment and can be reported.

2. Will loan settlement stop recovery agent calls completely?

Yes. Once your loan is settled and the lender issues an NOC, the account is closed. With nothing left to recover, the calls stop.

3. Is loan settlement legal in India?

Yes, fully legal. RBI's One-Time Settlement guidelines let banks settle NPAs through negotiated lump-sum payments. Zavo keeps the process lender-approved and documented.

4. Can I settle my loan if I've only skipped a few EMIs?

Settlement usually applies to accounts in or near default. Skipping EMIs actually makes lenders more open to negotiation. Zavo helps you check eligibility first.

5. How much does Zavo Settle charge?

Zero fees. You pay only what you agree with your lender, no commission, no hidden charges plus up to 2% cashback on every successful settlement.