What makes credit cards more than just a payment method?

Credit cards are more than just a convenient way to pay for purchases—they’re a powerful financial tool that offers flexibility, rewards, and additional perks like cashback, travel benefits, and exclusive privileges.

However, the advantages of credit cards can quickly become financial burdens if you don’t understand one critical aspect: credit card interest rates.

Interest rates determine the cost of borrowing when you carry a balance on your credit card.

Understanding how these rates work, when they’re charged, and how to minimize them is essential for managing your finances effectively and avoiding unnecessary debt

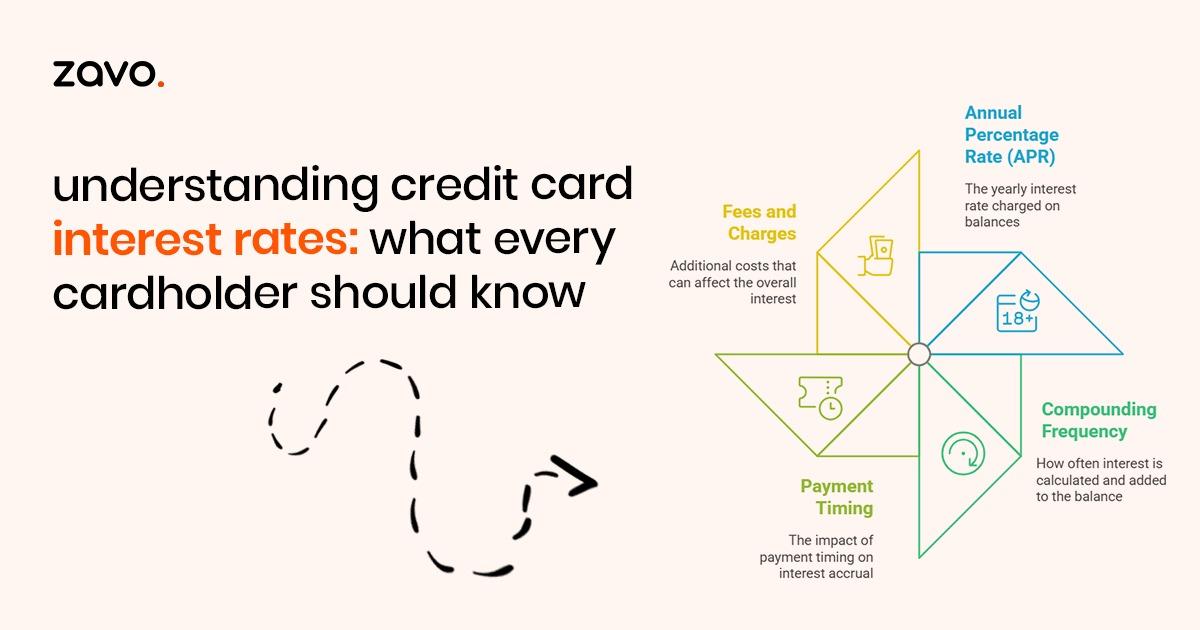

What Are Credit Card Interest Rates?

A credit card interest rate is the cost charged by the issuer when you carry an unpaid balance past the payment due date. Expressed as the Annual Percentage Rate (APR), this rate represents the yearly interest cost. If you pay your total credit card balance by the due date, you can completely avoid interest charges.

However, any unpaid balances will accrue interest, which compounds over time, significantly increasing your total debt. In a recent ruling, the Supreme Court overturned a 16-year-old decision by the National Consumer Disputes Redressal Commission (NCDRC), allowing banks to charge interest rates exceeding 30% on credit card dues, no longer considering such rates an unfair trade practice.

Key Factors Influencing Credit Card Interest Rates

1. Type of Credit Card: Credit cards with premium features (e.g., travel benefits, high reward points, or exclusive perks) often have higher interest rates to offset the additional privileges. Basic cards, which offer fewer benefits, typically come with lower rates.

2. Credit Score: A credit score reflects your financial reliability. A score of 750 or higher can qualify you for lower interest rates, while a lower score may result in higher rates due to the perceived risk of default.

3. Income and Financial Stability: Banks assess your income and stability when determining your interest rate. Higher, consistent income reduces your risk as a borrower, often resulting in more favorable rates.

4. Issuer Policy: Different banks have varying policies for setting interest rates, influenced by market competition, risk appetite, and card features.

How Do Credit Card Interest Rates Work?

Credit card interest is calculated daily on unpaid balances, compounded over time. The formula for calculating interest is:

Example Calculation

At the end of the billing cycle, ₹147.90 is added to your ₹10,000 balance. If left unpaid, this total becomes the basis for the next cycle’s interest calculation, leading to compounding debt.

When Is Interest Charged on Credit Cards?

Banks charge interest in several situations:

1. Carrying a Balance

If you don’t pay the full outstanding balance by the due date, interest is charged on the unpaid amount. This is the most common way cardholders incur interest.

2. Cash Advances

Using your credit card to withdraw cash incurs immediate interest, usually at a higher rate than regular transactions. Additionally, there’s no grace period, so interest starts accruing from the day of withdrawal.

3. Partial Payments

If you pay only part of the total due amount, interest is charged on the remaining balance. For example, if your total due is ₹15,000 and you pay ₹10,000, interest will be charged on ₹5,000.

4. Late Payments

Missing the payment due date triggers interest charges on the full outstanding balance, along with late payment fees. This can also negatively impact your credit score.

5. New Transactions with an Existing Balance

If you carry a balance from the previous billing cycle, any new purchases will immediately start accruing interest from the transaction date.

How to Lower Credit Card Interest Rates

While interest rates are often fixed, there are several ways to reduce your overall interest payments:

1. Negotiate with Your Issuer

If you have a strong payment history and a good credit score, you can request a lower interest rate from your credit card issuer. Banks often accommodate long-term, reliable customers.

2. Pay in Full and On Time

Clearing your full outstanding balance by the due date ensures you avoid paying any interest. This is the easiest and most effective way to manage credit card debt.

3. Leverage the Grace Period

Use the 20–50 day interest-free grace period to your advantage. Plan major purchases at the start of the billing cycle to maximize this interest-free window.

4. Convert Balances to EMIs

If you’re unable to pay off a large balance, consider converting it into Equated Monthly Instalments (EMIs). EMIs often come with lower interest rates and allow for manageable monthly payments.

Credit Card Interest-Free Period

The interest-free period is the time between the transaction date and the payment due date during which no interest is charged, provided the previous balance is fully cleared.

Example of an Interest-Free Period

- Billing Date: 5th of every month.

- Transaction Date: 6th May.

- Grace Period: 50 days.

- Payment Due Date: 24th June.

Transactions made later in the billing cycle have shorter grace periods. For instance, a purchase on 5th June will have a grace period of only 20 days.

Note: The grace period doesn’t apply to cash advances or unpaid balances carried forward.

Credit Card Interest Rates by Top Bank

(Note: Rates are subject to change and vary by card type.)

How to Avoid Paying Credit Card Interest

1. Pay Your Full Balance

The most effective way to avoid paying credit card interest is to clear your total outstanding balance by the due date every month.

- Why It Matters: When you pay the full amount on time, you avoid interest charges completely. This ensures that you stay within the interest-free grace period provided by your card issuer.

- How It Helps: Paying the full balance every month allows you to use your credit card as a free credit facility. You borrow money for your purchases and repay it without incurring additional costs.

- Example: Suppose your total due amount for the billing cycle is ₹10,000. If you pay the full ₹10,000 by the due date, you won’t be charged any interest. However, if you pay only ₹5,000, the remaining ₹5,000 will start accruing interest, which increases your overall financial burden.

Tip: Automate your credit card payments or set reminders to ensure you never miss paying the full balance on time.

2. Avoid Cash Advances

Using your credit card to withdraw cash from an ATM is known as a cash advance, and it’s one of the costliest features of a credit card.

- Why It Matters: Unlike regular purchases, cash advances don’t have a grace period. Interest starts accruing from the date of withdrawal, and the rates are usually higher than those for purchases. Additionally, many banks charge a cash advance fee, which is a percentage of the withdrawn amount (typically 2–3%).

- Example: If you withdraw ₹5,000 as a cash advance and the monthly interest rate is 3.5%, you’ll incur ₹175 in interest for the first month, plus a cash advance fee of ₹100–150. This adds up quickly if the amount isn’t repaid promptly.

Tip: Reserve the cash advance feature only for emergencies, and repay the amount as soon as possible to minimize costs.

3. Plan Purchases

Timing your purchases strategically can help you take full advantage of your credit card’s grace period, which typically ranges from 20 to 50 days.

- Why It Matters:The grace period is the time between the date of purchase and the payment due date when no interest is charged if the full balance is paid. Transactions made earlier in the billing cycle have a longer grace period, allowing you more time to repay without incurring interest.

- How It Helps: By planning large purchases at the beginning of your billing cycle, you can enjoy nearly the full grace period to arrange funds and repay the amount.

- Example: If your billing cycle starts on the 1st of the month and ends on the 30th, and your payment due date is the 20th of the following month, a purchase made on the 2nd will give you around 48 days of interest-free credit. A purchase made on the 29th, however, will have only about 21 days.

Tip: Check your billing cycle dates and make purchases accordingly to maximize your interest-free period.

4. Monitor Spending

Tracking your credit card usage is essential to ensure you stay within your financial limits and avoid unnecessary charges.

- Why It Matters: Missed due dates, overspending, or forgetting payments can result in interest charges, late fees, and a negative impact on your credit score. Monitoring your spending helps you stay aware of your total dues and ensures timely payments.

- How It Helps: By regularly reviewing your transactions and setting payment reminders, you can avoid missed payments and unnecessary interest charges. Many banking apps and credit card issuers offer tools to track spending, set alerts for upcoming due dates, and monitor your credit utilization.

- Example: Suppose your total credit limit is ₹50,000, and you’ve already spent ₹40,000 in a month. Monitoring your spending allows you to avoid exceeding your limit, which can trigger over-limit fees. Additionally, you can plan to repay the amount on time to avoid interest charges.

Tip: Use your bank’s mobile app or third-party budgeting tools to track transactions and receive alerts for due dates or unusual activity.

By adopting these strategies, you can make the most of your credit card while avoiding unnecessary interest charges and fees. Staying disciplined with your payments and planning your purchases wisely will help you maintain financial health and enjoy the benefits of your credit card without added stress.

Conclusion

Credit cards offer convenience, flexibility, and rewards, but they also require responsible usage to avoid unnecessary financial strain. Understanding how interest rates work empowers you to make smarter decisions, whether it’s choosing the right card, paying on time, or negotiating better terms. By adopting disciplined spending and payment habits, you can enjoy the benefits of credit cards while staying debt-free.

Get in Touch with us today to learn more about strategies to enhance your credit score and make smarter financial choices.

Frequently Asked Questions (FAQs)

1. Do all credit cards have the same interest rate?

No, credit card interest rates can vary significantly depending on the type of card, its features, and the issuer’s policies. For example, basic cards may have lower rates, while premium cards with rewards, cashback, or travel perks may come with higher rates. Additionally, promotional offers, such as introductory 0% APR, can impact rates temporarily. Always check the terms and conditions of a card before applying.

2. What happens if I only pay the minimum amount due?

Paying only the minimum due helps you avoid late fees and keeps your account in good standing, but it can lead to costly consequences. Interest will be charged on the remaining balance, increasing the overall amount you owe over time. Worse, if you carry a balance, new purchases typically lose their grace period, meaning interest starts accruing on those transactions immediately. This can make it harder to pay down your debt in the long run.

3. Can I lower my credit card’s interest rate?

Yes, it’s possible to negotiate a lower interest rate, especially if you’ve demonstrated responsible credit behavior. Lenders may agree to reduce your rate if you have a strong credit score, a history of on-time

payments, or if you’ve been a loyal customer. To improve your chances, research competitive rates, highlight your good payment history, and reach out to your issuer with a clear and polite request.

4. Why are credit card interest rates so high?

Credit card interest rates are high because they represent unsecured loans, meaning lenders don’t require collateral to approve your credit line. To offset the risks associated with potential defaults, issuers charge higher rates compared to secured loans like mortgages or auto loans. Credit card rates also account for administrative costs, rewards programs, and the convenience of revolving credit

5. How can I avoid paying interest on my credit card?

To steer clear of interest charges, focus on these key strategies:

- Pay your balance in full each month: By paying the total amount owed by the due date, you can utilize the card’s grace period and avoid interest on purchases.- Avoid cash advances: These transactions often come with no grace period and higher interest rates, leading to immediate charges.

- Plan your spending: Stay within your budget and ensure you have enough funds to pay off your statement balance on time.

- Be mindful of the grace period: Understand how your card’s grace period works, and make purchases accordingly to maximize interest-free days.