If you’re comparing loan settlement and loan closure, the short answer is simple: one is a relief option during hardship, and the other is the ideal way to finish a loan. Many borrowers confuse these two terms, but they have very different effects on your credit profile, future loan approvals, and financial reputation.

What Is the Difference Between Loan Settlement and Loan Closure?

The main difference is how much of the debt is repaid.

- Loan settlement means the lender accepts less than the total outstanding amount because the borrower cannot pay in full.

- Loan closure means the borrower repays the full amount due, either through regular EMIs or by paying the balance early.

This matters because lenders and credit bureaus treat both outcomes differently.

What Does Loan Settlement Mean?

Loan settlement is a negotiated agreement between a borrower and a lender. It usually happens when someone is facing serious financial problems and can no longer continue monthly repayments.

In this process:

- The borrower explains the hardship

- The lender reviews the account

- A reduced payoff amount may be offered

- The borrower pays the agreed sum

- The account is often marked as “settled”

This option is usually considered only after missed EMIs or prolonged repayment trouble.

When do people choose this option?

Borrowers often consider it during:

- Job loss

- Medical emergencies

- Business slowdown

- Sudden income drop

- Multiple overdue payments

It can provide short-term relief, but it may also create long-term borrowing challenges.

What Does Loan Closure Mean?

Loan closure means the full debt has been repaid according to the lender’s terms. This can happen in two ways:

- Regular closure – all EMIs are paid until the final month

- Pre-closure – the remaining balance is paid before the loan term ends

Once the full amount is cleared, the lender marks the account as “closed.” This is the best outcome from a credit perspective.

Loan Settlement vs Loan Closure: Quick Comparison

|

Factor |

Settlement |

Closure |

|

Amount Paid |

Less than total due |

Full amount due |

|

Credit Report Status |

Settled |

Closed |

|

Credit Score Impact |

Often negative |

Positive or neutral |

|

Future Loan Approval |

May become harder |

Usually easier |

|

Best For |

Serious financial hardship |

Normal repayment |

|

Lender View |

Partial recovery |

Full repayment success |

Fast answer

If you can afford full repayment, closure is almost always the better choice.

How Does the Settlement Process Work?

The process usually starts when a borrower falls behind on payments and cannot recover quickly.

Typical steps

1 - Contact the lender and explain the issue

2 - Request a hardship review

3 - Share income or emergency proof if needed

4 - Receive a negotiated offer

5 - Confirm the final amount in writing

6 - Pay the agreed sum

7 - Collect the final settlement letter

Important document checklist

Always keep:

- Written approval letter

- Payment receipt

- No-dues or final acknowledgment

- Updated loan statement

Without paperwork, future disputes can become messy.

How Does Loan Closure Work?

Loan closure is much simpler and safer.

Regular closure

You continue paying EMIs until the loan term ends.

Pre-closure

You repay the remaining balance before the final EMI date.

After closure, collect these documents:

- NOC (No Objection Certificate)

- Closure letter

- Final receipt

- Original documents for secured loans

This ensures the account is fully completed and properly recorded.

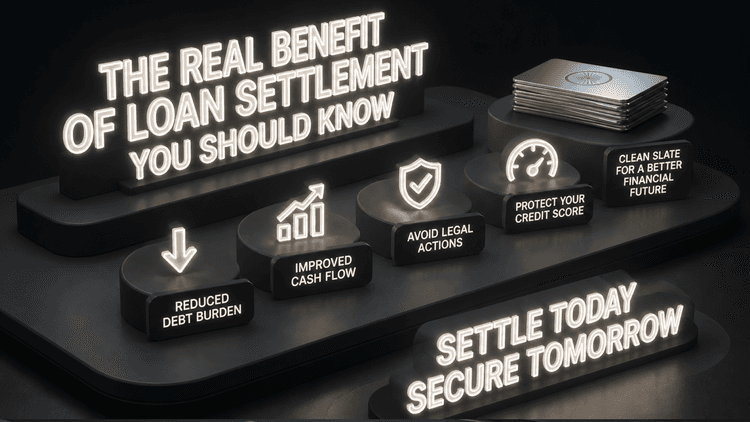

Benefits of Choosing Loan Settlement

There are situations where loan settlement can be useful, especially when repayment is no longer realistic.

Key benefits

- Reduces immediate debt pressure

- Helps stop recovery stress

- Can resolve a defaulted account faster

- May prevent further penalties from growing

- Offers a way out during severe hardship

For someone in crisis, this may be better than letting the account spiral further.

Risks You Should Know Before Choosing It

This is where borrowers need to be careful. The biggest issue with loan settlement is not the short-term relief, it's the long-term impact.

1. Credit score can be affected

A “settled” status may tell future lenders that the full debt was not repaid.

2. Future borrowing may become harder

Banks may become cautious when reviewing applications for:

- Credit cards

- Home loans

- Business funding

3. You may face higher interest rates later

Even if approved in the future, lenders may treat you as higher risk.

4. Verbal deals can cause problems

Never rely only on phone calls or informal promises. Written proof is essential.

Why Loan Closure Is Usually Better

From a financial planning point of view, loan closure is the stronger option.

Main advantages

- Keeps your repayment record clean

- Protect your credit score

- Builds trust with lenders

- Improves future approval chances

- Supports better loan terms later

If you have the ability to pay the full amount, closure is the smarter long-term move.

Which Option Should You Choose?

The answer depends on your current financial condition.

Choose closure if:

- You can still manage repayment

- You can prepay the balance

- You plan to apply for credit again soon

- You want to protect your credit history

Choose settlement if:

- You are in real financial distress

- Full repayment is impossible

- Your account is already overdue

- You can arrange only a partial lump sum

Best rule to remember

- If you can pay, close the account

- If you truly can’t, negotiate carefully

Should You Try Other Options First?

Yes, before choosing a loan settlement, always ask the lender about alternatives.

Safer options to explore first

- EMI restructuring

- Lower temporary EMI

- Tenure extension

- Moratorium support

- Balance transfer

- Partial prepayment plan

In many cases, these options can reduce pressure without harming your future borrowing as much.

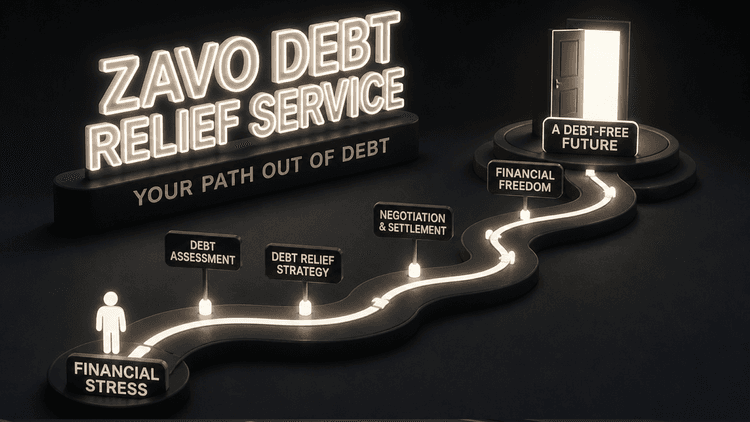

How Zavo Can Help During Debt Stress

If you are struggling with repayments and exploring practical debt solutions, professional guidance can make the process easier. This is where Zavo can be useful. Instead of handling lender conversations alone, many borrowers prefer support from a platform that helps them understand available options and take the next step with more confidence.

Zavo is positioned as a support resource for people dealing with financial pressure and looking for a structured path toward resolving outstanding debt. For borrowers who feel overwhelmed by missed EMIs, recovery calls, or confusion about what to do next, the platform can help simplify the process and point them toward a more manageable solution.

Why borrowers may consider Zavo

- Helps users understand debt resolution options

- Can support borrowers during financial hardship

- Useful for people who want clarity before speaking with lenders

- May reduce confusion around settlement-related decisions

- Offers a starting point for people seeking a practical action plan

When to explore Zavo

You may want to check Zavo if:

- You are already behind on EMIs

- You are facing serious financial pressure

- You want to understand debt resolution before negotiating

- You need help deciding between repayment options

- You want guidance before taking a major financial step

Common Mistakes to Avoid

Borrowers often make avoidable mistakes when dealing with overdue accounts.

Avoid these errors

- Ignoring lender communication

- Paying without written confirmation

- Assuming “settled” equals “closed.”

- Not checking the credit report later

- Skipping the final letter or NOC

- Rushing into a deal without comparing options

A careful approach can protect you from future trouble.

Conclusion

Understanding the difference between loan settlement and loan closure can save you from a costly financial mistake. One option offers relief during a crisis, while the other protects your long-term credit health.

Final takeaway

- Full repayment is the better path whenever possible

- Loan settlement should be used only when repayment is genuinely not possible

- Always get written proof

- Review your credit report after the process ends

If your goal is long-term financial stability, think beyond the immediate pressure and choose the option that protects your future.

Frequently Asked Questions

1. Is loan settlement good or bad?

It can help in serious hardship, but it may affect your credit record. It should usually be a last-resort choice.

2. Does loan settlement reduce the amount I owe?

Yes, the lender may agree to accept a lower lump sum than the full outstanding balance.

3. Is closure better than settlement?

Yes. Full repayment is usually better because it keeps your credit history stronger.

4. Can I get another loan after settling?

Yes, but approval may be harder and the terms may not be as favorable.

5. Should I settle after missing a few EMIs?

Not always. If the issue is temporary, try restructuring or other support options first.