If you're faced with an unexpected expense, such as a medical emergency, urgent home repairs, or a golden opportunity that requires immediate funding. A personal loan could be the perfect financial tool to bridge the gap. But before you rush to apply, do you know if you’re eligible?

Getting approved for a personal loan isn’t as simple as clicking “Apply Now.” Lenders carefully evaluate your creditworthiness, income, and financial history before granting a loan. So, who qualifies for a personal loan, and what do you need to get approved?

In this blog, we’ll break down who can apply for a personal loan, the key eligibility criteria, and how you can improve your chances of getting approved.

Who Can Apply for a Personal Loan?

Unlike home or car loans, personal loans are flexible and not restricted to specific expenses. Whether you’re a salaried employee, self-employed professional, or freelancer, you can apply for a personal loan, as long as you meet the lender’s eligibility criteria.

The Real Question: Are You Eligible?

Just because you can apply doesn’t mean you’ll get approved. Lenders assess multiple factors to determine your loan eligibility.

✅ Are you employed or earning a steady income?

✅ Do you have a good credit history?

✅ Is your debt-to-income ratio manageable?

✅ Are you within the age limits set by the lender?

If you answered yes to these questions, you have a good chance of qualifying for a personal loan. Let’s break down each of these factors in detail.

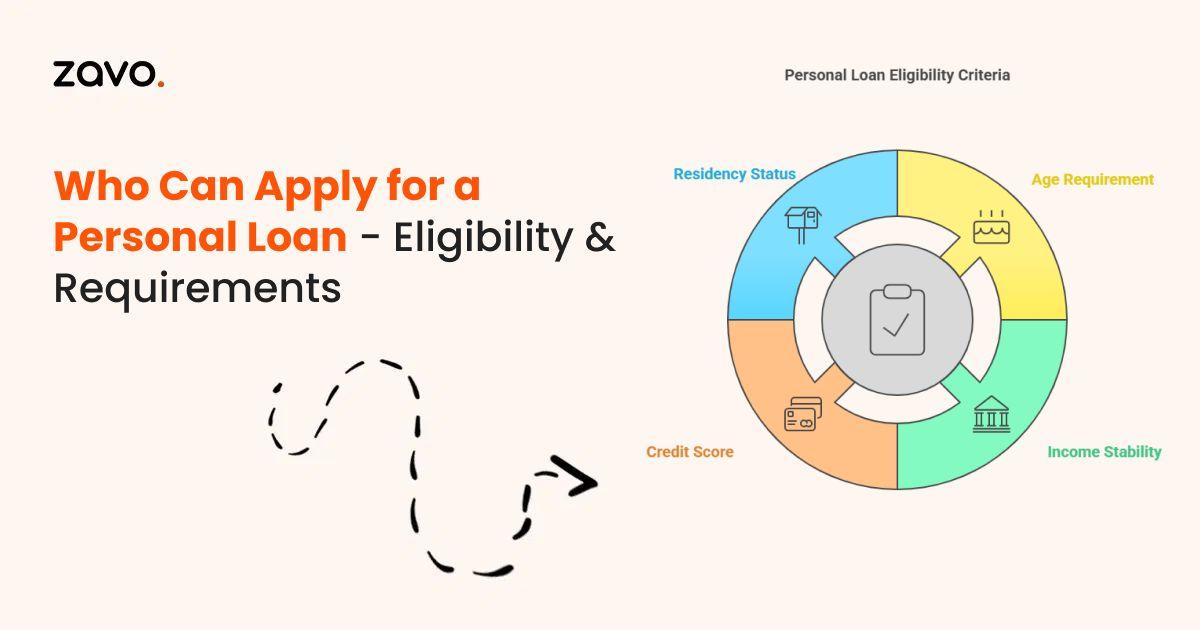

Personal Loan Eligibility Criteria

Every lender has different requirements, but most assess the following:

1️⃣ Age Criteria: Are You Old Enough (or Too Old) to Borrow?

Most lenders set an age range for borrowers:

- Salaried Employees: 21 to 60 years

- Self-Employed Individuals: 25 to 65 years

Lenders want to ensure you have enough working years left to repay the loan comfortably. If you’re close to retirement, getting approved can be harder unless you show strong financial stability.

Pro Tip: If you’re nearing retirement, consider opting for a shorter loan tenure to increase your chances of approval.

2️⃣ Income Stability: Can You Afford the Loan?

Your income level and stability directly impact how much you can borrow.

✔️ Salaried employees must show regular monthly earnings from a reputable employer.

✔️ Self-employed individuals & freelancers need a stable income history, supported by tax returns and bank statements.

Pro Tip: Lenders usually require a minimum income of ₹20,000 - ₹30,000 per month (varies by lender). Higher income = higher eligibility!

3️⃣ Credit Score: The Make-or-Break Factor

Your CIBIL score (or credit score) is one of the most crucial factors in getting approved for a personal loan.

🔹 750+ – Excellent (Best interest rates, easy approval)

🔹 650-749 – Good (Decent rates, moderate approval chances)

🔹 550-649 – Fair (Higher interest rates, possible rejection)

🔹 Below 550 – Poor (Low chances of approval)

Pro Tip: Check your credit score before applying—if it’s low, improve it by clearing outstanding dues and avoiding multiple loan applications.

4️⃣ Debt-to-Income Ratio: Are You Overloaded with Debt?

Lenders assess your Debt-to-Income (DTI) Ratio to ensure you aren’t taking on too much debt.

🔹 DTI Formula: (Total Monthly Debt Payments ÷ Monthly Income) x 100

Example: If you earn ₹50,000 per month and already pay ₹20,000 in EMIs, your DTI ratio is 40%.

📌 Ideal DTI Ratio: Below 40% – Higher chances of loan approval.

📌 Above 50%? Lenders may reject your application.

Pro Tip: If your DTI is high, pay off some existing loans before applying for a new one.

5️⃣ Employment History: Stability Matters

✔️ Salaried applicants should have at least 6-12 months of work experience.

✔️ Self-employed professionals should have a minimum of 2 years of stable income.

Frequent job changes or unstable income can lower your approval chances.

Pro Tip: Stick with one employer for at least a year before applying to show financial stability.

Documents Required for a Personal Loan

Lenders require various documents to verify an applicant’s identity, income, and financial stability. Commonly required documents include:

1. Identity Proof

Lenders require government-issued identity proof to verify your identity and prevent fraudulent applications. Acceptable documents include:

- Passport – A widely accepted identity document, especially for international verification.

- Driver’s License – Serves as both an identity and address proof in many cases.

- Voter ID – Confirms your citizenship and identity.

- Aadhaar Card (for Indian applicants) – A unique identification number mandatory for many financial transactions in India.

Why is it required?

- Ensures the loan application is genuine and belongs to the right person.

- Helps lenders comply with KYC (Know Your Customer) regulations.

2. Address Proof

Lenders need proof of residence to ensure they can contact you in case of any communication regarding the loan. Commonly accepted address proofs include:

- Utility bills (electricity, water, or gas) – These serve as proof of residence if they are in your name.

- Rental/lease agreement – If you’re a tenant, this document proves your place of residence.

- Bank statements – Many banks accept official bank statements as address proof if they contain your residential address.

Why is it required?

- Helps lenders verify your permanent or current address.

- Ensures that the borrower has a stable residence, reducing the risk of default.

3. Income Proof

Lenders assess your income stability to determine whether you have the financial capacity to repay the loan. The required income proof varies depending on your employment type:

- For Salaried Employees:

Recent salary slips (typically last 3–6 months) – These show your consistent monthly income and salary trends.

Form 16 – Some lenders might require this document as proof of tax deduction at source (TDS).

- For Self-Employed Individuals:

Income tax returns (ITR) – Usually, lenders require the last 2-3 years’ ITRs to analyze your financial standing.

Profit & loss statements – If you own a business, lenders may ask for this to understand your company’s financial health.

Business financials – Includes audited balance sheets and bank statements to assess income consistency.

4. Employment Proof

Employment verification is essential for salaried applicants to confirm job stability. Lenders typically ask for:

- Appointment letter – A document from your employer confirming your position and salary.

- Company ID card – Proof that you are employed with the stated organization.

- Employer verification letter – Some lenders may require an official letter from your employer confirming your designation and salary.

5. Bank Statements

Most lenders require bank statements from the past 6 months to assess your financial stability and transaction history.

- Salaried employees need to provide salary account statements.

- Self-employed individuals need to show business account transactions.

6. PAN Card (For Indian Applicants)

A Permanent Account Number (PAN) card is a mandatory financial document for loan applications in India.

Why is it required?

- Required for most financial transactions, including loan approvals, credit card applications, and tax filings.

- Helps prevent tax evasion and financial fraud.

- Required for income tax verification and KYC compliance.

How to Improve Your Chances of Getting Approved

If you don’t meet some eligibility criteria, don’t lose hope! Here’s how you can boost your approval chances:

✔️ Improve your credit score – Pay bills on time, reduce outstanding debts.

✔️ Lower your debt-to-income ratio – Clear some loans before applying.

✔️ Increase your income – Show additional sources of income like rent, side gigs.

✔️ Apply with a co-applicant – A joint application (spouse/parent) improves approval chances.

✔️ Opt for a lower loan amount – Don’t apply for more than what your income can support.

Pro Tip: Use a Personal Loan Eligibility Calculator to check how much you qualify for before applying!

Final Thoughts

With the RBI kicking off its rate-cut cycle, we could be entering a phase where loan interest rates gradually decrease. This is great news for borrowers, as it means personal loans might become more affordable in the coming months. However, while lower interest rates make borrowing more attractive, approval is still not guaranteed.

A personal loan can be a lifesaver, but only if you qualify for one. Understanding what lenders look for and preparing in advance can significantly improve your chances of getting approved with the best interest rates.

Before you apply, ask yourself:

✔️ Do I meet the lender’s eligibility criteria?

✔️ Can I afford the EMIs without financial strain?

✔️ Have I checked my credit score and reduced my debt?

✔️ Do I have all the required documents ready?

If you answered YES to these, you’re ready to apply for a personal loan .

At zavo, we make personal loans fast, easy, and stress-free, with instant approvals, flexible repayment terms, and zero hidden fees.

Need funds urgently? Apply now with zavo and get money in your account in minutes!

Frequently Asked Questions (FAQs)

1. Can I apply for a personal loan if I have a low credit score?

Yes, but your interest rates may be higher. Consider improving your score or applying with a co-borrower.

2. How much personal loan can I get on my salary?

Most lenders offer loans up to 30 times your monthly salary, but approval depends on your DTI ratio.

3. Can self-employed individuals apply for a personal loan?

Absolutely! You’ll need to show a stable income history and valid tax returns.

4. Is age a factor in personal loan approval?

Yes, you must be between 21-60 years (salaried) or 25-65 years (self-employed) to apply.

5. How long does it take to get loan approval?

With online lenders, you can get approval within minutes and disbursal in 24 hours!