What’s the best way to borrow money—without borrowing trouble?

Choosing between a personal loan and a home equity loan can feel like a financial puzzle, but the decision becomes easier once you understand the differences. Whether you’re consolidating debt, funding home improvements, or covering unexpected expenses, picking the right loan type can save you money and stress. Let’s dive into the key differences, so you can make the smartest choice for your needs.

What is a Personal Loan?

A personal loan is a financial product that allows you to borrow money without offering collateral, such as a house or car, as security. This makes it an unsecured loan. Banks, credit unions, and online lenders offer personal loans with fixed terms (typically 2–7 years) and fixed interest rates, so your monthly payments stay consistent.

Since there’s no collateral, lenders determine whether to approve your loan and what interest rate to charge based on your creditworthiness, which includes factors like your credit score (higher scores usually mean better rates), income (proving you can repay), and debt-to-income ratio (a lower ratio indicates less financial strain).

People often use personal loans for flexible purposes such as consolidating high-interest debts, covering emergency medical expenses, paying for weddings, or funding vacations. Approval and funding can be fast, sometimes within a few days, which makes personal loans appealing for urgent needs.

However, the absence of collateral increases the lender's risk, so personal loans usually have higher interest rates than secured loans like mortgages. Loan amounts may also be limited, often capped around $50,000. Despite these drawbacks, personal loans remain popular for their flexibility and accessibility, especially for those with a strong financial profile.

For instance, imagine you need ₹10,000 for a destination wedding. A personal loan allows you to cover the cost without waiting months to save or risking assets. However, it’s essential to consider the total cost, including interest and fees, before committing.

What is a Home Equity Loan?

A home equity loan, often called a "second mortgage," is a secured loan that allows homeowners to borrow a lump sum against the equity they’ve built in their property, typically up to 80-90% of their home’s value. These loans feature fixed interest rates and repayment terms ranging from 5 to 30 years, offering predictable monthly payments. Because the loan is secured by the home, interest rates are generally lower than those of personal loans or credit cards. Common uses include home renovations, college tuition, or debt consolidation. Additionally, the interest may be tax-deductible if the loan is used for home improvements, though this should be confirmed with a tax advisor. While these loans provide access to large funds and manageable payments, the risk lies in potentially losing your home if repayments are not made.

Key Differences Between Personal Loans and Home Equity Loans

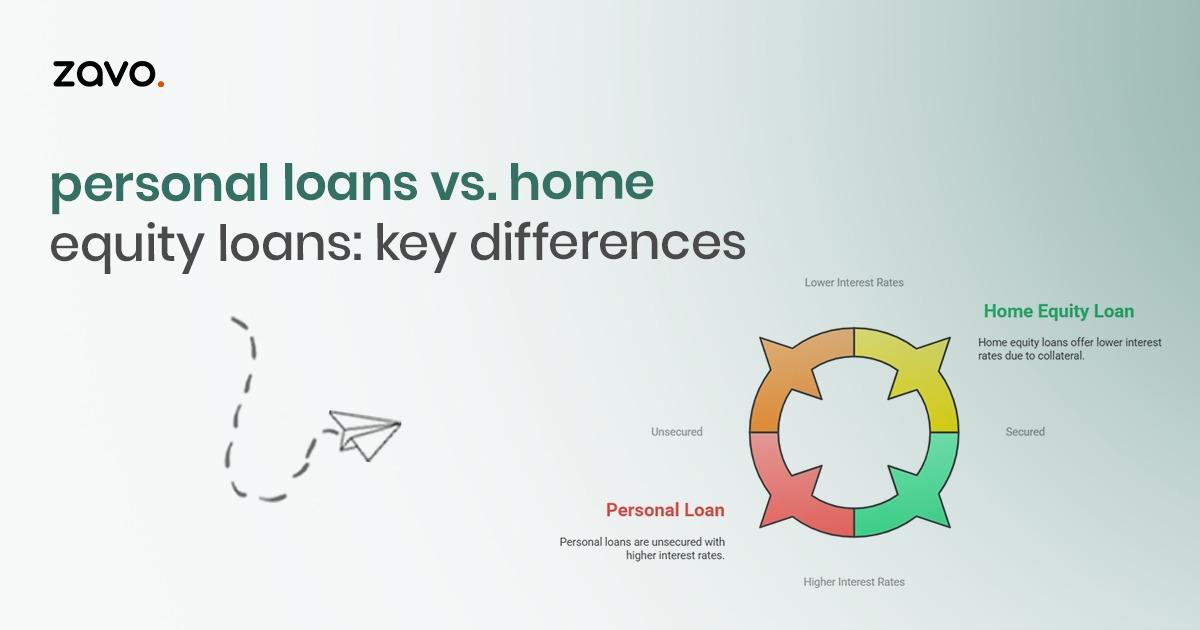

1. Collateral Requirement: Personal loans are unsecured, while home equity loans require you to use your home as collateral. This difference significantly impacts eligibility, interest rates, and risk.

2. Interest Rates: Since home equity loans are secured, they usually offer lower interest rates than personal loans. Personal loans may have higher rates, but don’t put your home at risk.

3. Approval Process: Personal loans typically have a quicker approval process, often within a day or two. Home equity loans take longer, as they require an appraisal and a deeper financial review.

4. Loan Amounts: Home equity loans generally allow you to borrow larger sums because they’re tied to your property’s value. Personal loans usually have lower borrowing limits, often capped at ₹50,000 or less.

5. Use Cases: Personal loans are versatile and can be used for nearly anything. Home equity loans are better suited for substantial, long-term investments, like home improvements.

Factors to Consider When Choosing

1. Risk Tolerance: When deciding between a personal loan and a home equity loan, your comfort with risk is a critical factor. A home equity loan uses your home as collateral, meaning failure to repay the loan could result in losing your property. This makes it a higher-risk option, especially for those who might face financial instability during the loan term. On the other hand, personal loans are unsecured, so your assets aren’t at risk. If you’re uncomfortable with the idea of leveraging your home or fear the possibility of foreclosure, a personal loan is a safer alternative.

2. Credit Score: Your credit score plays a significant role in determining the interest rates and approval for both loan types. If you have an excellent credit score, you’re likely to secure a personal loan with a competitive interest rate. However, if your credit score is moderate or poor, personal loans may come with higher rates or stricter terms. In such cases, a home equity loan might be advantageous because it’s secured by your home, often resulting in lower rates despite a lower credit score.

3. Urgency: How quickly you need the funds can influence your choice. Personal loans are typically faster to secure, with some lenders approving applications and disbursing funds within 1-3 business days. Home equity loans, however, involve a more extensive process, including property appraisals and a detailed financial review, which can take weeks. If time is of the essence, a personal loan is generally the quicker option.

4. Loan Purpose: The intended use of the loan can also determine the better choice. Home equity loans are ideal for significant, long-term expenses like home renovations, education, or debt consolidation due to their larger borrowing limits and lower interest rates. In contrast, personal loans are more suitable for smaller, short-term needs like medical bills, vacations, or wedding expenses. Their flexibility and speed of approval make them convenient for immediate, diverse financial needs.

Understanding these factors will help you make an informed decision that aligns with your financial goals and circumstances. Let me know if you'd like to expand on any of these points further!

Conclusion: Which One Is Right for You?

Both personal loans and home equity loans have their merits, depending on your financial situation and needs. Personal loans are ideal for smaller, short-term financial needs, while home equity loans work better for significant, long-term expenses. Whichever option you choose, ensure it aligns with your goals and financial stability.

Ready to make your move? zavo’s team of loan experts is here to help you find the perfect solution. Whether you’re leaning towards a personal loan or a home equity loan, we’ll guide you every step of the way. Contact us today for personalized assistance and competitive rates.

Frequently Asked Questions

1. Which is better: a personal loan or a home equity loan?

The better options depend on your needs. A personal loan is usually better for smaller expenses and faster funding, while a home equity loan is amounts if you want lower interest rates and already own a home.

2. Is a personal loan safer than a home equity loan?

Yes, in many cases, a Personal loan is considered safer because it does not require your home as collateral. With a home equity loan, your property is at risk if you fail to make repayments.

3. Do home equity loans have lower interest rates than personal loans?

Generally, yes. Home equity loans often come with lower interest rates because they are secured against your home. Personal loans are unsecured, so lenders may charge higher rates.

4. Can I get a personal loan faster than a home equity loan?

Yes. Personal loans are usually approved and disbursed faster, sometimes within a few business days . Home equity loans often take longer because they may require property valuation and additional documentation.

5. Can I get a personal loan with bad credit?

It's possible, but you’ll likely face higher interest rates and stricter terms. Improving your credit score can help you secure better options.