Do overdue loans keep you up at night? You're not alone. Thousands of Indians are quietly dealing with the same pressure, and a loan settlement service might be the honest way out.

What Is Loan Settlement, Really?

Let's skip the jargon.

Loan settlement is when you and your lender agree to close your loan for less than what you originally owed. You pay a one-time negotiated amount, the lender marks the account as "settled," and the pressure finally lifts.

It's not a magic trick. It's not running away from your debt. It's a legitimate financial tool that banks and NBFCs themselves use to recover money from borrowers who genuinely can't repay the full amount.

Think of it this way, a lender would rather recover ₹50,000 from you today than chase ₹80,000 for the next three years. That's the logic behind settlement. And when done right, it works for both sides.

Who Actually Needs Loan Settlement?

Not everyone. But if you're checking one or more of these boxes, it might be worth exploring:

- Your EMIs have been overdue for 90+ days

- You've lost your job, faced a medical emergency, or had a business setback

- Collection calls are coming in daily and causing stress

- You want to close the chapter on an old loan and start fresh

- Paying the full outstanding amount feels impossible right now

If any of that sounds familiar, loan settlement isn't giving up it's making a smart move with the cards you have.

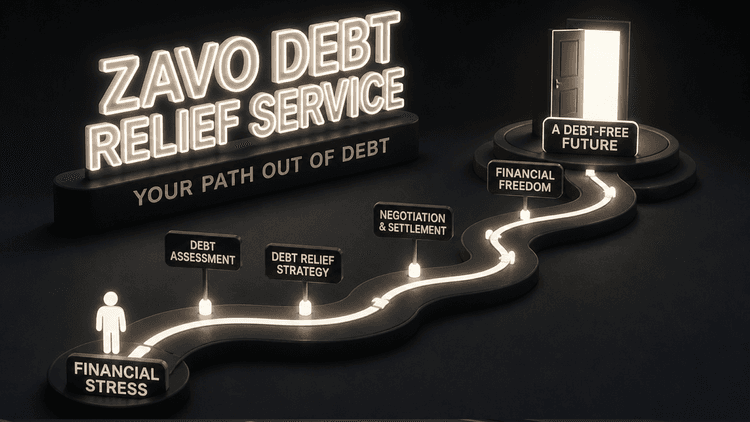

How Does the Loan Settlement Process Work?

The process sounds complicated, but it really isn't. Here's how it typically goes:

Step 1: Assess your situation - Before anything else, get clear on how much you owe, how many EMIs you've missed, and what you can realistically pay right now. Be honest with yourself here.

Step 2: Reach out to your lender - You (or a platform like Zavo) contact the lender and express that you're facing financial difficulty and want to explore settlement. Most lenders have a dedicated team for this.

Step 3: Negotiate the amount - This is where it matters. The lender will propose a settlement amount, usually the principal minus some portion of interest and penalties. You negotiate. Sometimes you go back and forth a couple of times.

Step 4: Get it in writing - Never settle verbally. Always ask for a written settlement agreement before paying anything. This protects you.

Step 5: Pay and get your NOC - Once you pay the agreed amount, the lender gives you a No Objection Certificate (NOC) and marks the loan as settled in their books.

That's it. The account is closed.

If negotiating directly with lenders sounds nerve-wracking, platforms like Zavo handle the entire process for you, including talking to the lender, drafting paperwork, and making sure you don't overpay. They work directly with lenders, which means no middlemen eat into your settlement.

What Happens to Your CIBIL Score After Settlement?

This is the question everyone asks. Let's be straight with you.

When a loan is settled (rather than fully repaid), your credit report will show the status as "Settled" instead of "Closed." These are two different things in the eyes of a credit bureau.

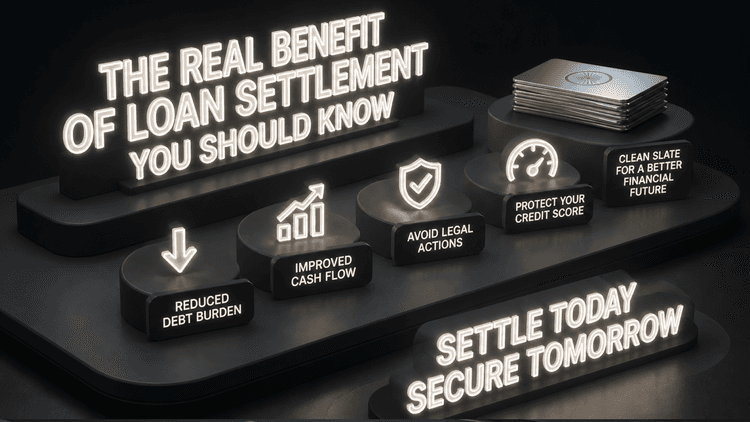

"Settled" does impact your CIBIL score there's no sugarcoating that. However, here's the fuller picture:

- If your loan was already 90–180 days overdue, your score has already taken a hit

- Settling actually stops the damage from getting worse

- Over time, with responsible credit behaviour, your score can recover

- Many people use services like a credit builder after settlement to actively repair their score

So yes, a settlement affects your credit report. But for someone already in default, it's often the first step toward recovery, not another step backward.

The goal isn't to avoid the impact. It's to stop the bleeding and start healing.

Loan Settlement vs Loan Closure: What's the Difference?

People mix these up all the time.

Loan Closure means you've repaid every rupee you owed, principal, interest, everything. The account closes with a clean "Closed" status. Best outcome for your credit.

Loan Settlement means the lender agreed to accept less than the full amount. The account closes, but with a "Settled" tag on your report.

If you can fully repay, always do that and explore EMI relief options that might reduce your burden while keeping your credit intact. But if full repayment isn't possible, settlement is the realistic alternative that still lets you move forward.

Common Myths About Loan Settlement

Myth 1: "Loan settlement is illegal." Completely false. It's a standard banking practice. RBI guidelines even account for it. Lenders negotiate settlements every day.

Myth 2: "My lender will never agree." Lenders are more flexible than people think, especially for accounts that have been in default for a long time. They'd rather recover something than nothing.

Myth 3: "I have to be completely broke to settle." Not true. You need to demonstrate genuine financial hardship, but you don't have to be in a crisis. Even a documented job loss or income reduction can open the door.

Myth 4: "I can do this myself for free, no platform needed." Technically yes. But negotiating with a lender without knowing their internal processes, benchmarks, or settlement patterns often means you settle for more than you needed to. Platforms with lender relationships (like Zavo) often get better deals.

How Zavo Makes Loan Settlement Less Scary

Let's be real, most people don't know how to talk to a bank about a settlement. And even if they do, they worry they'll say the wrong thing, accept a bad deal, or get misled.

That's exactly what Zavo was built to fix.

Here's what makes it different:

Zero settlement fees - You don't pay Zavo to settle your loan. They've removed the cost barrier that other services charge.

Direct lender access - No middlemen. Zavo works directly with banks and NBFCs, which means faster resolution and better terms.

97% success rate - This isn't a marketing number pulled from thin air. It reflects real settlements across 10 lakh+ verified users.

Cashback on successful settlement - You actually get money back when your settlement goes through. That's genuinely rare in this space.

Collection pressure eases - Once the settlement process starts with Zavo, those daily collection calls naturally begin to reduce.

After settlement, many Zavo users also use the credit builder feature to actively rebuild their credit score because closing the loan is step one, but getting back to financial health is the real goal.

A Quick Word on Timing

If you're thinking about loan settlement, don't wait too long.

The longer an account stays in default, the harder it becomes to negotiate reasonable terms and the more damage accumulates on your credit report. Lenders are also more likely to transfer your account to aggressive recovery agencies the longer it sits.

Acting early (or at least not delaying once you've decided) almost always leads to better settlement terms.

Is Loan Settlement Right for You?

Here's a simple gut-check:

You have one or more loans in default or near-default. Full repayment isn't realistic in the near term. You want to close the debt and move on. You're okay with a temporary credit report impact in exchange for a fresh start

If you said yes to most of these, loan settlement is worth exploring seriously and soon.

Final Thoughts

Debt is stressful. But staying stuck in it because you don't know your options is worse.

Loan settlement isn't a failure. It's a financial decision that millions of people make every year to get their lives back on track. When done correctly, with the right support, it can be the reset button you've been looking for.

If you're ready to explore what settlement could look like for your specific loans, Zavo's platform makes it straightforward, transparent, and surprisingly human.

Settle smart. Start fresh.

Looking to protect your EMIs before things get worse? Explore EMI relief options on Zavo. Already settled and want to repair your score? Check out how to rebuild your credit score with Zavo's Credit Builder.

Frequently Asked Questions

Q1. Is loan settlement legal in India?

Yes, completely legal. It is a standard banking practice recognized under RBI guidelines. Lenders negotiate settlements regularly with borrowers who are genuinely unable to repay the full amount.

Q2. Will a loan settlement affect my CIBIL score?

Yes, your credit report will show "Settled" instead of "Closed." It does impact your score temporarily but if your loan is already in default, settlement stops further damage and becomes your first step toward recovery.

Q3. How much can I save through loan settlement?

It depends on your lender, loan type, and how long the account has been overdue. In many cases, borrowers close their debt by paying 40–60% of the total outstanding amount.

Q4. How long does the loan settlement process take?

Usually 2 to 8 weeks. It depends on how quickly you and the lender agree on an amount. With Zavo's direct lender access, the process moves significantly faster.

Q5. Can I rebuild my CIBIL score after loan settlement?

Yes, absolutely. Using a credit builder and maintaining healthy financial habits, timely payments, low credit utilization your score can recover steadily after settlement.