It starts with a few missed calls. Then it becomes ten calls a day. Then they start calling your family, your colleagues, maybe even showing up at your home.

If you're dealing with loan recovery agent harassment, you're not alone, and more importantly, you're not without options.

This article covers what recovery agents are legally allowed to do, where they cross the line, and crucially, how resolving your loan through a structured settlement can stop the pressure entirely.

What Is Loan Recovery Agent Harassment?

When you miss EMIs on a personal loan, credit card, or any other unsecured loan, lenders typically assign your account to a recovery or collections team. In many cases, especially once the loan is significantly overdue, this gets handed to a third-party recovery agency.

These agents are tasked with recovering the outstanding dues, and unfortunately, many go far beyond what is legally acceptable in how they do it.

Loan recovery agent harassment typically includes:

- Calling you more than 4 to 5 times a day, at odd hours

- Contacting your family members, employer, or neighbours

- Using threatening, abusive, or humiliating language

- Visiting your home or office without prior notice and in an intimidating manner

- Misrepresenting themselves as legal or court officials

- Sharing your personal loan details with third parties without consent

If any of this sounds familiar, what you're experiencing isn't just unpleasant; it may be illegal under Indian law.

What the RBI Says: Your Rights as a Borrower

The Reserve Bank of India (RBI) has clear guidelines on how recovery agents must conduct themselves. These aren't suggestions; they are enforceable rules that banks and their agents are required to follow.

Under the RBI's Fair Practices Code and the guidelines on engagement of recovery agents, here is what is explicitly prohibited:

Calling hours: Recovery agents can only contact you between 8:00 AM and 7:00 PM. Calls outside these hours are a violation.

No harassment or coercion: Agents cannot use threatening language, intimidation, or physical force of any kind. This includes verbal abuse or messages designed to humiliate you.

No third-party contact for pressure: Agents can contact your references only to locate you, not to shame, pressure, or reveal details of your loan to them.

No misrepresentation: Agents cannot claim to be police officers, court officials, or legal enforcement representatives. They must clearly identify themselves and the institution they represent.

Right to complain: You have the right to escalate recovery misconduct to the bank's grievance cell, the Banking Ombudsman, or even the police if there's harassment or criminal intimidation.

Knowing your rights is step one. But knowing your rights alone doesn't make the calls stop.

Why Recovery Pressure Keeps Escalating (And When It Gets Worse)

Here's something most people don't fully understand: recovery intensity is directly linked to how long a loan stays unresolved.

When you first miss an EMI, the lender's internal team follows up. When the loan crosses 60–90 days without payment, it may be classified as NPA (Non-Performing Asset). At this stage, the file often moves to an external recovery agency, and the pressure typically escalates.

The longer the loan stays in default, the more aggressive the recovery activity tends to become. Interest and penalties keep accumulating. Calls increase. Legal notices may follow.

The most effective way to stop this cycle isn't just to know your rights; it's to resolve the underlying debt. And that's where loan settlement comes in.

How Loan Settlement Can Stop Recovery Harassment Permanently

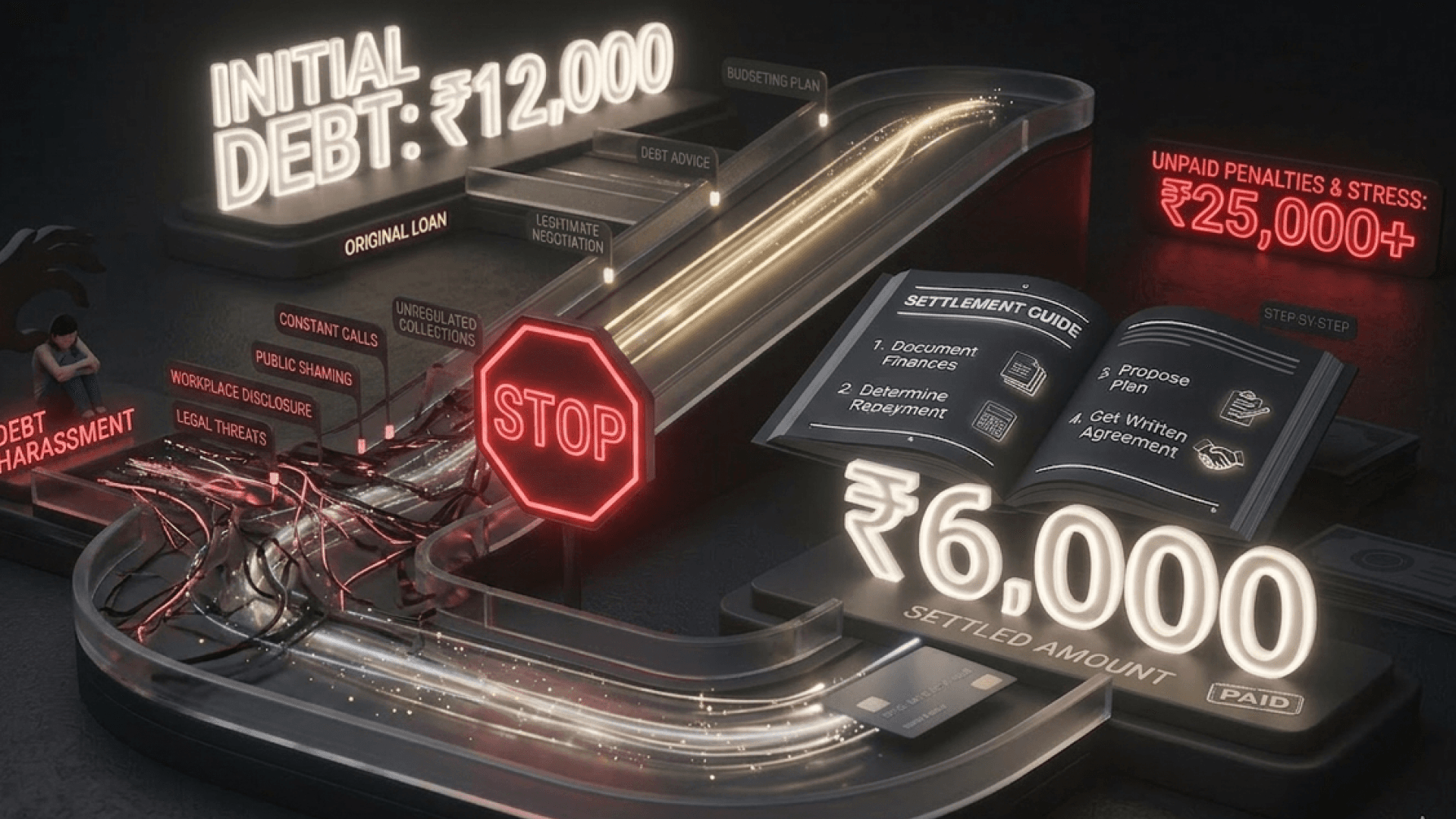

Loan settlement is a formal process where you and your lender agree on a reduced amount to fully close your loan account. Once a settlement is agreed upon and the amount is paid, the loan is officially closed and all recovery activity stops.

This is not a workaround. It is a legitimate, legally recognized resolution mechanism that banks and NBFCs use regularly when a borrower is genuinely unable to repay the full outstanding amount.

Here's how it addresses recovery harassment directly:

It removes the reason for collection pressure. Recovery agents are chasing you because there's an outstanding debt. Once you enter a structured settlement process, the lender is engaged in resolution, not recovery. Collection activity naturally reduces.

It ends the compounding of dues. Every day a loan sits in default, interest and penalties add up. Settlement stops this clock and gives you a defined, manageable number to close the account.

It is faster than you might think. With the right platform, a settlement process can begin almost immediately, and lender-approved offers can come through without months of back-and-forth.

What the Loan Settlement Process Looks Like with Zavo

Zavo is India's loan and credit card settlement platform. With a 97% success rate, Zavo works directly with lenders on your behalf, no middlemen, no hidden costs.

Here's what the process looks like:

Step 1 - You share your loan details. Zavo reviews your outstanding dues, loan type, and default status to assess your situation.

Step 2 - Zavo approaches the lender directly. Rather than you navigating awkward bank conversations alone, Zavo engages the lender's settlement team on your behalf. This is done transparently, with no third-party agents eating into your settlement amount.

Step 3 - A settlement offer is negotiated. Based on your financial situation and the lender's assessment, a settlement figure is proposed. Zavo helps you get a deal that works for what you can realistically pay.

Step 4 - Collection pressure begins to ease. Once settlement discussions are underway, recovery calls typically reduce. The lender knows you're in resolution mode, not ignoring the debt.

Step 5 - You pay and receive your No Dues Certificate. The agreed amount is paid directly to the lender. You get a formal settlement letter and a No Dues Certificate confirming the loan is closed.

"But Will Settling My Loan Hurt My Credit Score?"

Yes, and it's important to be honest about this.

When a loan is settled (rather than fully repaid), your CIBIL report reflects a "Settled" status instead of "Closed." This can affect your ability to get new credit for a period of time.

But here's the context that matters: if you've already been missing EMIs for months, your credit score has likely already dropped significantly. Each unpaid EMI is a negative mark. The longer the loan stays unresolved, the worse the damage.

Settlement stops further damage. It gives you a clean starting point. And with disciplined financial behaviour after settlement using secured credit products, paying on time, your score can be rebuilt over time.

For most people in genuine financial distress, the choice isn't between a perfect credit score and a settled one. It's between ongoing harassment and a debt spiral versus a structured resolution that lets you move forward.

When Should You Consider Loan Settlement Over Other Options?

Loan settlement is the right path when:

- You have missed multiple EMIs, and the loan is significantly overdue

- You are facing recovery calls, legal notices, or visit-based harassment

- You have no realistic ability to repay the full outstanding amount in the near term

- You have some lump sum available that could go toward a negotiated settlement

It may not be the right option if you're only slightly behind on payments; in that case, restructuring or a repayment plan may work better. Zavo can help you assess which route makes the most sense for

your specific situation.

What to Do Right Now If You're Being Harassed

If you're currently dealing with aggressive recovery agent behaviour, here are immediate steps:

1 - Document everything. Save call logs, screenshots of messages, and note the time and nature of each contact. This evidence matters if you escalate.

2 - Send a written complaint to the bank. Every bank has a grievance redressal process. Put your complaint in writing via email to their nodal officer.

3 - File a complaint with the Banking Ombudsman if the bank doesn't respond within 30 days.

4 - Approach a structured settlement platform. Getting into formal resolution is the fastest way to reduce collection pressure because it addresses the root cause.

The Bottom Line

Loan recovery agent harassment is something thousands of Indians deal with silently every month. You have legal rights. You have recourse. And you have a practical path out of the situation, not just temporarily, but permanently.

Loan settlement isn't about escaping your debt. It's about resolving it in a way that works for your reality so the calls stop, the interest stops growing, and you can get back to building your financial life.

If you're ready to explore whether settlement is right for your situation, Zavo's team can walk you through your options with zero fees and zero pressure.