Let's be honest, managing multiple loans at the same time is exhausting. There's the personal loan EMI hitting your account on the 5th, the credit card bill that seems to grow no matter how much you pay, and maybe a BNPL debt you almost forgot about. If this sounds like your life right now, you've probably searched for solutions and come across two terms that show up constantly: loan consolidation and loan settlement.

But here's what most articles won't tell you for a large number of borrowers in India, especially those already struggling with repayments, loan settlement might actually be the more practical and impactful route. Let's break this down in a way that actually makes sense for your situation.

What Is Loan Consolidation in India?

Loan consolidation is the process of combining multiple loans into a single loan ideally with a lower interest rate and one unified EMI. On paper, it sounds like a great idea. Instead of paying five different lenders every month, you pay just one.

In India, loan consolidation is typically offered through personal loans used to pay off existing debts, balance transfer facilities (especially for credit card debt), and top-up loans from existing lenders.

If your credit score is still healthy and you have a stable income, consolidation can genuinely reduce your monthly burden and simplify your finances. But here's the catch most banks and NBFCs only approve consolidation loans for people who are currently repaying on time. If you've already missed EMIs or are drowning in debt, getting approved for a new loan to repay old ones becomes very difficult. That's where loan settlement becomes relevant.

Loan Settlement vs. Loan Consolidation: What's the Real Difference?

These two options sound similar but work in completely different ways.

Loan consolidation restructures your debt you still owe the full amount, just to a different lender or under new terms. Your total outstanding principal doesn't go down. You're essentially shifting the problem, not resolving it.

Loan settlement, on the other hand, is a negotiated agreement where your lender agrees to accept less than the full amount you owe as a final closure of the loan. This happens when a borrower is genuinely unable to repay the full outstanding amount. Instead of letting the loan turn into a long, painful legal dispute, the lender agrees to a one-time settlement and you walk away debt-free.

Who Should Consider Loan Settlement Over Consolidation?

Loan settlement is not for everyone but for the right person, it can be life-changing. You might be a strong candidate for settlement if:

You have missed multiple EMIs and your loan is already in default or near-default status. You're facing constant collection calls that are affecting your mental health and daily life. Your income has dropped significantly due to job loss, medical issues, or a business slowdown. You've tried to negotiate with lenders on your own and hit a wall. You don't qualify for a new consolidation loan because your CIBIL score has taken a hit.

If any of these describe your situation, pursuing loan consolidation in India may not even be an option for you but loan settlement absolutely can be.

How Loan Settlement Works in India

The process might seem intimidating, but it's more structured than most people think. Here's a simplified overview of what typically happens:

Step 1: Assessment of Your Financial Situation

A settlement service provider like zavo evaluates your outstanding loans, your current income, and how much you can realistically offer as a settlement amount. This is not a random number; it's based on actual data.

Step 2: Negotiation With the Lender

This is where experience matters. Zavo's team negotiates directly with banks and NBFCs on your behalf. Lenders are often more willing to settle than borrowers realise, especially when the alternative is a prolonged legal process with uncertain recovery.

Step 3: Settlement Agreement

Once both sides agree on a figure, a formal settlement letter is issued by the lender. This document is crucial: it confirms the loan closure terms and protects you legally.

Step 4: Payment and Closure

You make the agreed settlement payment, and the loan is officially closed. Collection calls stop. The pressure lifts. You get your life back.

Why Zavo Is India's Most Trusted Loan Settlement Platform

There are plenty of people who claim to help with debt but very few who actually do it transparently, efficiently, and with real results. Zavo is different, and here's why that matters to you.

97% Success Rate: Zavo has helped over 10 lakh verified users navigate the settlement process. That's not a marketing number, it's a track record built case by case.

Direct Lender Access, No Middlemen: Zavo works directly with banks and NBFCs. There's no chain of agents or brokers adding delays and confusion. You get faster outcomes because there's no unnecessary back-and-forth.

Reduced Collection Pressure: Once Zavo initiates the settlement process on your behalf, the relentless collection calls begin to ease out. You can finally breathe again while the negotiation happens in the background.

Cashback on Successful Settlement: Zavo even offers cashback when your settlement is successfully closed, a rare and genuine commitment to ensuring the process genuinely benefits you.

Full Transparency: You'll know exactly what's happening at every step. No surprises, no hidden moves. Just clear communication and lender-approved options.

Zavo's platform has been rated 4.3 out of 5 by its users, and has earned the trust of over 3 million Indians who rely on it for all things EMI. That kind of trust isn't built overnight.

What Happens to Your CIBIL Score After Settlement?

This is the question everyone asks, and it deserves an honest answer. Yes, a settled loan does get marked on your CIBIL report; it typically appears as "settled" rather than "closed," which can affect your credit score in the short term.

However, here's the reality: if you're already missing EMIs, your credit score is likely already dropping. A loan that keeps defaulting can cause far more long-term damage than a settled account. Settlement, in many cases, is actually the beginning of credit recovery not the end of your financial life.

After settlement, Zavo also helps you understand how to use their Credit Builder feature to start rebuilding your score gradually. Debt-free is the first step. Better credit comes next.

Loan Consolidation in India: When Does It Still Make Sense?

To be fair, consolidation is the right choice in specific scenarios. If you have a good CIBIL score (above 700), stable employment, and you're not yet behind on payments, consolidating multiple high-interest loans into a single lower-interest loan can save you money and reduce complexity.

But for most people who are actively searching for debt relief, consolidation has already become inaccessible. They've already crossed the threshold where new loan approvals are unlikely. For them, the real question isn't consolidation vs. settlement; it's whether to keep struggling alone or to get professional help.

Take the First Step Towards a Debt-Free Life

Debt has a way of making everything feel impossible. The constant notifications, the awkward conversations, the feeling that there's no way forward weighs on you in ways that go far beyond money. But it doesn't have to stay that way.

Whether loan consolidation in India is on your radar or you're exploring loan settlement for the first time, the most important step is understanding your options clearly. And the fastest way to do that is to talk to experts who've seen it all before.

Zavo has helped over 10 lakh Indians settle their loans and reclaim their peace of mind. With a 97% success rate, direct lender access, and full transparency throughout the process the path to becoming debt-free is clearer than you might think.

Ready to explore your options? Ready Visit the Zavo loan Settlement and take the first step today

Frequently Asked Questions

Is loan settlement legal in India?

Yes, loan settlement is completely legal. It's a formal agreement between the borrower and the lender, documented in writing and governed by RBI guidelines.

How is loan consolidation different from loan settlement?

Consolidation combines your loans into one new loan you still owe the full amount. Settlement is a negotiated closure where the lender accepts less than the outstanding amount as full and final payment.

Will I be debt-free after settlement?

Yes. Once the settlement is completed and the agreed amount is paid, your loan is officially closed. You receive a settlement letter from the lender confirming this.

How long does the loan settlement process take with Zavo?

Timelines vary based on the lender and loan type, but Zavo's direct lender relationships help move things significantly faster than going it alone.

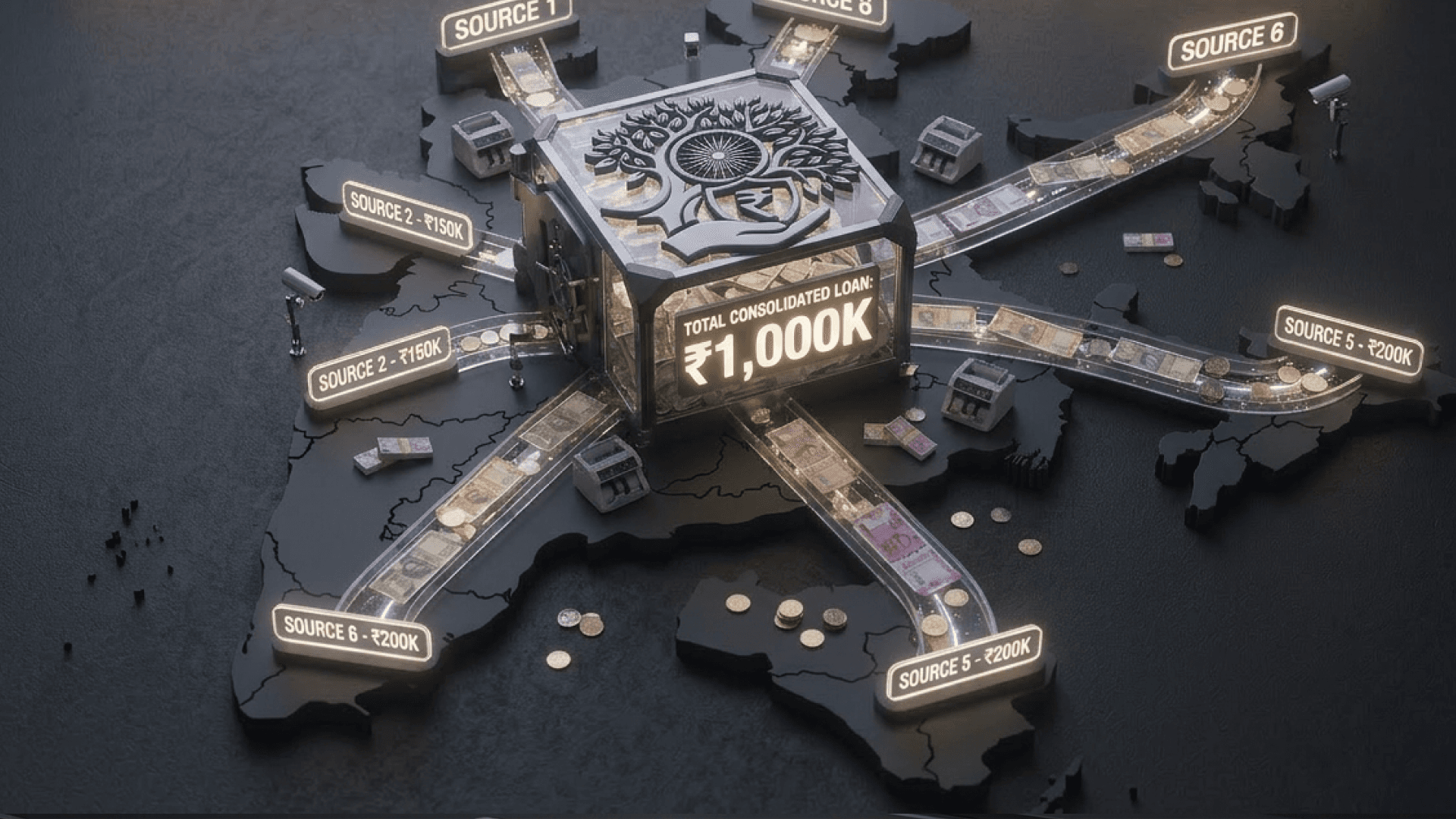

Can I settle multiple loans at the same time?

Yes. Zavo helps borrowers manage and settle multiple loans simultaneously which is one of its biggest advantages over trying to negotiate individually with each lender.