If you are searching for a loan settlement in India, chances are you are already under financial pressure. Maybe your EMIs have started slipping, lender calls are becoming frequent, or you simply want to know whether settling a loan is the right move before things get worse.

And honestly, that is a very real situation for many borrowers in India.

But here is the truth: most people do not explain clearly:

Loan settlement can give short-term relief, but if you do it the wrong way, it can affect your CIBIL score and make future borrowing difficult.

In this article, you will understand:

- What loan settlement really means,

- How the process works in India,

- When you should consider it,

- How it affects your CIBIL score,

- What mistakes to avoid,

- And whether a platform like Zavo can help before things become serious.

If you are already under EMI pressure, do not panic.

Read this carefully first. A smart decision today can save you from a bigger financial headache tomorrow.

What Is Loan Settlement in India?

In simple words, loan settlement means you and the lender agree that instead of paying the full outstanding amount, you pay a reduced amount, and the lender accepts it as a final negotiated payment.

This usually happens when a borrower is unable to continue regular EMI payments due to a serious financial problem.

Simple Example

Suppose:

- your personal loan outstanding is ₹5,00,000,

- you are unable to repay the full amount,

- the lender agrees to accept ₹3,20,000,

- and you pay it within the agreed timeline.

That is called loan settlement.

It sounds like relief and in many cases, it is.

But there is one important catch.

In your credit report, the account may be marked as:

- Settled

instead of

- Closed

That one word can make a big difference when you apply for a loan later.

Loan Settlement vs Loan Closure: Why This Difference Matters

A lot of borrowers think if the loan is over, it is all the same.

It is not.

A loan closure means you repaid the full amount exactly as agreed. A loan settlement means the lender accepted less than the full dues because you were unable to repay everything.

Quick Difference

- Loan Closed = full repayment done

- Loan Settled = partial negotiated repayment done

- Closed status = better for future borrowing

- Settled status = may create risk in future approvals

This matters because when you apply later for:

- a home loan,

- a car loan,

- a business loan,

- or even a credit card,

The next lender may check how your previous loan ended.

So yes, loan settlement may reduce today’s pressure, but it can create tomorrow’s borrowing challenge.

When Should You Consider Loan Settlement?

This is where many people go wrong.

Not every borrower who is struggling should jump straight into loan settlement.

If your income issue is temporary, or if you just need a little breathing space, settlement may not be the best option. In many cases, restructuring or EMI relief is a smarter first step.

You should consider loan settlement only if:

- You have lost your job,

- Your salary has reduced sharply,

- Your business cash flow has collapsed,

- You had a medical emergency,

- Multiple EMIs are already overdue,

- Recovery pressure is increasing,

- And you genuinely cannot repay the full amount.

You should avoid loan settlement if:

- you can still manage with a lower EMI,

- you only need temporary relief,

- you can refinance the loan,

- a family member can help you short term,

- or you plan to apply for a home loan soon.

Best Practical Rule

Before choosing loan settlement, always try this order first:

1 - EMI relief

2 - Tenure extension

3 - Penalty waiver

4 - Loan restructuring

5- Partial payment with revised EMI

6 - Only then consider loan settlement

That is the smartest borrower approach.

How to Do Loan Settlement in India: Step-by-Step Process

If loan settlement is your only realistic option, then the process matters a lot. Doing it the right way can reduce future problems. Doing it carelessly can create bigger trouble later.

1. Ask for the Exact Outstanding Amount

Do not negotiate blindly.

Before anything else, ask the lender for a complete breakup of your dues.

This should include:

- principal outstanding,

- interest outstanding,

- late payment charges,

- penal interest,

- bounce charges,

- overdue amount,

- and any legal or collection-related fees.

Sometimes the total looks huge only because penalties and charges have piled up. If you do not know about the breakup, you cannot negotiate smartly.

2. Explain Your Financial Hardship Clearly

Many borrowers make the mistake of disappearing.

They stop answering calls, ignore emails, and avoid the lender. That usually makes the situation worse.

Instead, speak directly and explain your genuine financial problem.

Common reasons lenders take seriously:

- job loss,

- salary cut,

- business slowdown,

- medical emergency,

- family crisis,

- sudden income disruption.

Helpful documents you can show:

- termination letter,

- reduced salary slip,

- medical bills,

- bank statements,

- ITR showing lower income,

- GST drop (for business owners).

The more genuine and documented your hardship is, the stronger your case becomes.

3. Ask for Restructuring Before Asking for Loan Settlement

This is one of the smartest things you can do.

Before saying, “I want loan settlement,” first ask whether the lender can help you continue the loan in a more manageable way.

Ask questions like:

- Can my EMI be reduced?

- Can the tenure be extended?

- Can late charges be waived?

- Can overdue amounts be adjusted into future EMIs?

- Can I get a temporary lower EMI plan?

If restructuring works, you may avoid the “Settled” remark in your credit report — and that can protect your future loan eligibility.

4. Negotiate the Loan Settlement Amount Carefully

This is where people expect a simple answer, but real banking does not work that way.

There is no fixed rule in India that says a lender must reduce your loan by 30%, 50%, or 70%.

The final settlement amount depends on:

- the type of loan,

- whether it is secured or unsecured,

- how old the default is,

- the number of missed EMIs,

- your current repayment ability,

- your financial hardship documents,

- whether legal action has started,

- and the lender’s internal policy.

Reality Check

In real cases, lenders may:

- waive penalties only,

- reduce part of the interest,

- offer partial negotiated settlement,

- or allow a lump-sum reduced closure.

So yes, negotiation is possible.

But guaranteed settlement percentages are usually a red flag.

5. Get the Settlement Offer in Writing

This is non-negotiable.

Before paying even ₹1, ask for an official written settlement letter or a formal email.

The settlement letter should mention:

- your name,

- loan account number,

- total outstanding amount,

- final agreed settlement amount,

- payment deadline,

- payment mode,

- whether payment is lump sum or in installments,

and confirmation that no further dues will remain after successful payment.

Never do these mistakes:

- do not pay cash to a field agent,

- do not trust only verbal promises,

- do not depend only on WhatsApp chats,

- do not believe “sir system mein ho jayega.”

In India, paperwork is protection.

6. Make Payment Only Through Safe Channels

Once the terms are clear, make the payment only through traceable methods.

Safe payment methods include:

- NEFT

- RTGS

- IMPS

- branch deposit

- cheque or DD

- official lender payment link

- verified UPI to the lender’s official account

Keep proof of everything:

- payment receipt,

- UTR number,

- screenshot,

- branch acknowledgment,

- confirmation email.

If there is any dispute later, these documents can save you.

7. Collect NOC and Check Your Credit Report

Many borrowers think the work ends after the payment.

It does not.

After completing loan settlement, collect:

- No Objection Certificate (NOC)

- Settlement confirmation letter

- Final account statement

- Email confirming no further dues

Then check your credit report after a few weeks and verify that the lender has updated the account correctly.

Never assume the system updated automatically.

How Loan Settlement Affects Your CIBIL Score

This is the part many borrowers understand too late.

Yes, the settlement process can affect your CIBIL score and future borrowing profile.

When a lender marks your account as “Settled,” it means you did not repay the full amount originally due. Future lenders may see this as a sign of financial stress.

What can happen later:

- loan approvals may become harder,

- interest rates may be higher,

- sanctioned amounts may be lower,

- document checks may become stricter,

- Home loan approval may become difficult.

So if you are planning any major borrowing in the next 1–3 years, think carefully before choosing settlement.

That is why loan settlement should be used only when necessary not casually.

What RBI-Style Borrower Protection Means During Recovery

One thing every borrower should remember:

Missing EMIs does not mean you lose your dignity.

Even if your loan is overdue, recovery should not turn into harassment.

Recovery should not involve:

- threats,

- abusive language,

- public humiliation,

- forced cash payments,

- fake legal threats,

- or pressure without proper documentation.

If recovery behavior becomes aggressive, stay calm and document everything.

What you should do:

- ask the agent’s name,

- ask which agency they represent,

- save messages and call details,

- email the lender’s grievance team,

- escalate in writing if needed.

In finance matters, written proof is your strongest shield.

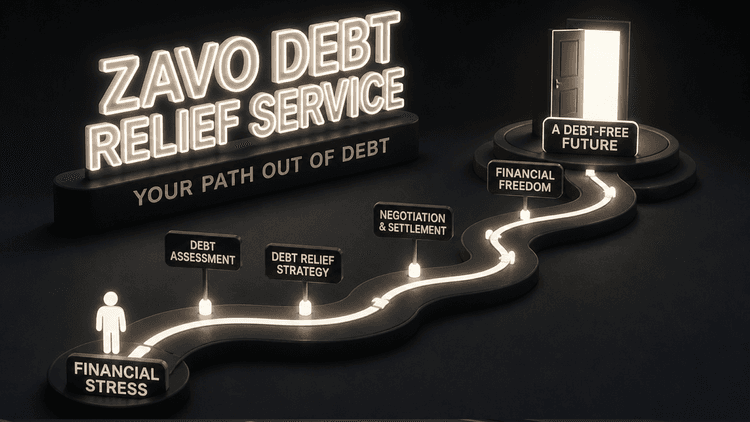

Can a Platform Like Zavo Help Before Loan Settlement?

Yes and this is where your article becomes more practical and useful.

Many borrowers do not actually need immediate loan settlement. What they need is early support before the situation becomes worse. They need clarity, structure, and a better understanding of their repayment options.

That is where a platform like Zavo can be mentioned naturally.

Instead of presenting it like a hard sales pitch, the more trustworthy approach is to position it as an early borrower support option.

How Zavo can fit in naturally:

- it may help borrowers explore repayment flexibility,

- it may help them understand lender-led options,

- it can be useful before default becomes more serious,

- and it may help people avoid depending on random offline “settlement agents

If you are already under EMI stress, a platform like Zavo may help you explore repayment flexibility or lender-led options before full default turns into a more serious problem. Always verify terms, lender coverage, and written conditions directly before proceeding.

Common Mistakes People Make During Loan Settlement

This section is very important because small mistakes during loan settlement can create big future problems.

Most common mistakes:

- trusting verbal promises,

- paying cash to field agents,

- not asking for a written settlement letter,

- confusing “Settled” with “Closed,”

- ignoring the CIBIL impact,

- skipping restructuring options,

- missing the payment deadline,

- not collecting NOC,

- not checking the credit report later.

Simple rule to remember:

If you do not have written proof, you do not have protection.

How to Rebuild Your Credit After Loan Settlement

If you have already completed a loan settlement, do not panic.

A settled account is not the end of your financial life. But yes, rebuilding trust with lenders takes time.

The first step is to become extremely disciplined with every current payment. Every EMI, every credit card bill, and every due should be paid on time without fail.

Best habits to rebuild your credit:

- pay all EMIs on time,

- clear credit card bills fully,

- keep card usage below 30%,

- avoid multiple new loan applications,

- maintain stable banking habits,

- check your credit report regularly,

- build 12–24 months of clean repayment history.

In some cases, if the lender allows it, you may even ask whether paying the waived balance later can help update the status from “Settled” to “Closed.” It is not guaranteed, but it is worth asking in writing.

Final Verdict: Should You Choose Loan Settlement?

Here is the honest answer.

If your financial situation is genuinely broken, if multiple EMIs are already overdue, if recovery pressure is increasing, and if restructuring is no longer possible, then loan settlement can be a practical damage-control option.

But if you still have a realistic path to repayment even through a reduced EMI, longer tenure, or revised plan then it is usually smarter to protect your credit profile and avoid settlement if possible.

Choose loan settlement if:

- your financial situation is severe,

- multiple EMIs are overdue,

- you genuinely cannot repay in full,

- restructuring has failed,

- and you need to stop the situation from getting worse.

Avoid loan settlement if:

- you can still manage with a revised EMI,

- you only need short-term breathing room,

- your credit profile can still be protected,

- or you are planning a home loan soon.

Loan settlement is not a shortcut.

It is an emergency financial decision.

And emergency decisions should always be handled carefully.

Conclusion

If you came here looking for the safest way to handle loan settlement in India, remember this one thing:

Do not rush.

Before agreeing to any settlement:

- understand your exact dues,

- talk to the lender directly,

- try restructuring first,

- get every term in writing,

- make payment only through official channels,

- and check how it affects your credit profile.

That is the real difference between a desperate borrower and a smart borrower.

Loan settlement can help but only when used at the right time, in the right way, and for the right reason.

FAQs About Loan Settlement in India

Is loan settlement legal in India?

Yes, loan settlement is legal. It is a negotiated arrangement between the borrower and the lender. However, the lender is not required to offer it.

Is loan settlement good or bad?

It can help in a genuine financial emergency, but it is usually less favorable than full repayment or restructuring because it may affect your credit profile.

Does settlement affect CIBIL?

Yes, it can. A settled account may be viewed negatively by future lenders because it shows the full dues were not repaid.

Can I get a home loan after loan settlement?

It is possible, but it may be harder. Some lenders may treat a recent settled account as a risk factor.

Is loan settlement better than ignoring the loan?

In many cases, yes. A structured and documented loan settlement is usually better than letting the account become worse.