Missed payments can be a stressful experience, especially when they lead to a sharp drop in your credit score. In India, a good credit score is essential for securing loans, credit cards, or even renting an apartment. Your financial health relies heavily on maintaining a strong CIBIL score, which represents your creditworthiness. But if life’s uncertainties have caused you to miss payments, don’t worry—there’s a way out.

Rebuilding your credit score is not an overnight process, but with a clear plan and disciplined effort, you can restore your financial credibility.

Let’s dive into a comprehensive blog tailored for Indian consumers to help you regain control of your credit score.

What is a CIBIL Score and Why is it Important?

In India, the CIBIL score is the most recognized credit score, ranging from 300 to 900. Managed by TransUnion CIBIL, it reflects your credit behavior and repayment capacity. A score of 750 and above is considered excellent and opens doors to attractive loan offers and lower interest rates.

Your CIBIL score is calculated based on five major factors:

1. Repayment History (35%): Timely payments are critical; missed payments negatively affect this factor.

2. Credit Utilization Ratio (30%): Using too much of your available credit signals financial stress.

3. Length of Credit History (15%): A longer history of responsible credit usage boosts your score.

4. Credit Mix (10%): A healthy balance of secured (home loans) and unsecured (credit cards) credit helps.

5. New Credit Inquiries (10%): Frequent applications for credit can lower your score temporarily.

Understanding these components is the first step in rebuilding your credit score effectively.

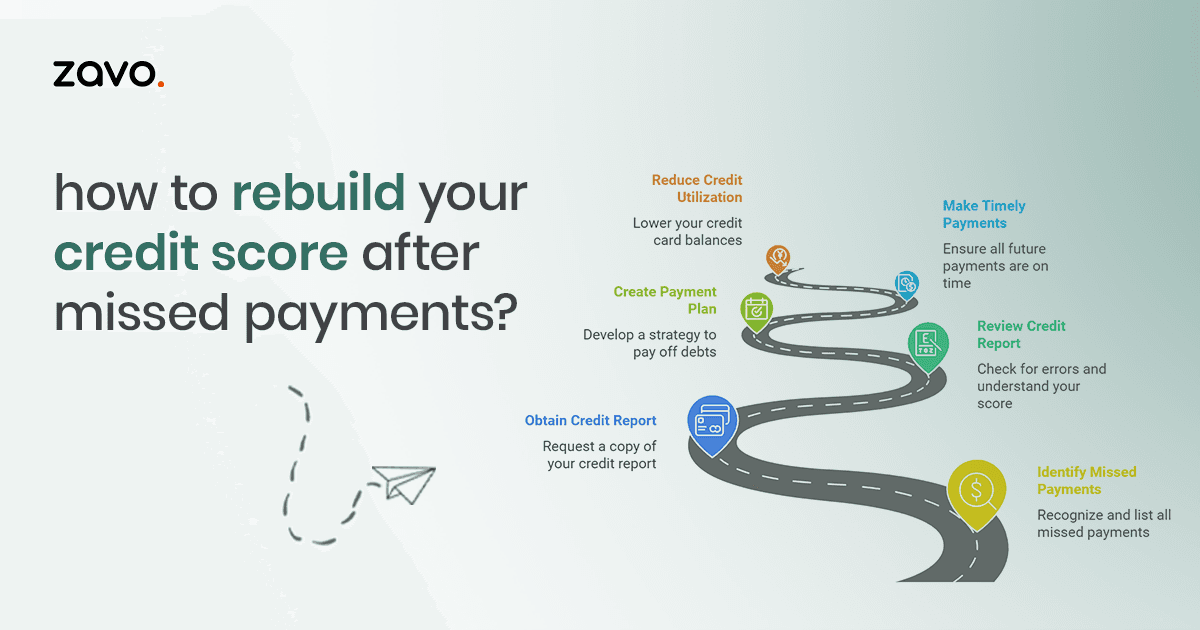

Step 1: Obtain and Review Your Credit Report

The foundation of rebuilding your credit score starts with understanding your current situation. You can request a free credit report once a year from credit bureaus like CIBIL, Experian, or CRIF High Mark.

What to Look for in Your Report?

Missed Payments: Identify the accounts where payments were delayed or defaulted.

-

Errors or Discrepancies: Check for inaccuracies, such as payments marked as missed when they were made.

-

Outstanding Balances: Note any unpaid dues that may still be impacting your score.

If you find errors, file a dispute with the respective credit bureau and provide supporting documents. Correcting inaccuracies can have an immediate positive effect on your score.

Step 2: Pay Off Outstanding Dues

Missed payments often lead to unpaid dues, which not only harm your credit score but also attract penalties and higher interest rates. Clearing these dues is a priority.

How to Clear Outstanding Balances?

-

Negotiate Settlements: Contact lenders to negotiate a repayment plan or settle for a lesser amount.

-

Prioritize High-Interest Debts: Focus on paying off credit card balances first, as they accrue high-interest charges.

-

Use the Debt Snowball or Avalanche Method: The snowball method targets smaller debts first, while the avalanche method focuses on high-interest debts.

Paying off dues demonstrates financial responsibility, which lenders value when calculating your score.

Step 3: Build a Timely Payment History

Timely payments account for the largest portion of your CIBIL score. Establishing a consistent repayment routine can gradually rebuild your creditworthiness.

Tips for Ensuring Timely Payments

-

Set Auto-Debit for Bills: Automate payments for EMIs, credit cards, and utility bills to avoid forgetting due dates.

-

Use Financial Apps: Apps like Paytm and CRED provide reminders and cashback incentives for timely payments.

-

Create a Budget: Allocate funds for fixed expenses, including loan repayments, and avoid unnecessary spending.

Even one year of on-time payments can significantly improve your score.

Step 4: Reduce Credit Utilization

A high credit utilization ratio (CUR) indicates that you’re relying too much on borrowed money, which can lower your score. Aim to keep your CUR below 30%.

How to Manage Credit Utilization?

-

Pay Down Balances Regularly: Prioritize reducing your credit card debt.

-

Request a Credit Limit Increase: A higher credit limit can lower your utilization ratio without additional payments.

-

Avoid Overusing Credit Cards: Use credit cards sparingly and only for planned expenses.

Reducing your CUR not only boosts your score but also enhances your financial stability.

Step 5: Use Secured Credit Products

If your credit score is too low to qualify for standard financial products, consider secured credit options to rebuild your profile.

Secured Credit Cards: Banks like HDFC, ICICI, and Axis Bank offer secured credit cards against fixed deposits. These cards function like regular credit cards but reduce the risk for the lender. Use them responsibly by paying the balance in full every month.

Credit-Builder Loans: Some Indian NBFCs offer loans specifically designed to help you build credit. These loans require small monthly payments, which contribute to a positive repayment history.

Step 6: Avoid Frequent Credit Inquiries

Each time you apply for credit, lenders perform a hard inquiry, which can temporarily lower your score. Multiple inquiries in a short period can signal financial distress.

Best Practices to Avoid Unnecessary Inquiries

-

Opt for Pre-Approved Offers: Pre-approved loans or credit cards don’t require hard inquiries.

-

Apply Sparingly: Only apply for credit when absolutely necessary.

-

Space Out Applications: Allow a few months between applications to minimize the impact on your score.

Being selective about new credit applications can prevent further damage to your score.

Step 7: Address Collections and Charge-Offs

If missed payments have resulted in accounts being sent to collections, it’s crucial to resolve them.

How to Handle Collection Accounts?

-

Verify the Debt: Ensure the debt is valid and belongs to you.

-

Negotiate Settlements: Work with collection agencies to pay off debts at a reduced amount.

-

Request a "Pay-for-Delete": Some agencies may agree to remove the account from your credit report after payment.

Clearing these accounts removes major negative marks from your report.

Step 8: Monitor Your Progress

Rebuilding your credit score takes time and patience. Regularly monitoring your credit report ensures that you stay on track and catch errors early.

Tools for Credit Monitoring in India

-

CIBIL Score and Report: Available on the official CIBIL website.

-

Credit Monitoring Apps: Apps like zavo, BankBazaar, MoneyView, and CreditMantri provide free updates on your score.

-

Bank Services: Many Indian banks, such as SBI and HDFC, offer free or discounted credit score monitoring.

Tracking your progress keeps you motivated and helps identify areas that need further improvement.

Step 9: Seek Professional Help if Needed

If the rebuilding process feels overwhelming, consider consulting a credit counselor or financial advisor. Reputable organizations like zavo offer tailored advice to manage debt and rebuild credit.

Conclusion

Rebuilding your credit score after missed payments in India is a journey that requires time, patience, and consistent effort. By clearing outstanding dues, making timely payments, reducing credit utilization, and responsibly using secured credit products, you can improve your CIBIL score and regain financial stability.

A strong credit score isn’t just a number—it’s the key to unlocking better opportunities and financial freedom. Start today, and with persistence, you’ll soon see your efforts reflected in a healthier credit profile.

Take charge of your financial health with zavo. Whether it’s building better financial habits, managing debt, or improving your credit score, we’re here to guide you every step of the way. Let zavo help you achieve a brighter financial future.

Frequently Asked Questions (FAQs)

1. How long does it take to rebuild a credit score after missed payments?

Rebuilding your credit score depends on the severity of missed payments and your efforts to improve it. Generally, it can take 6 to 12 months of consistent, on-time payments and responsible credit usage to see a noticeable improvement in your score. Severe cases, like accounts sent to collections, may take longer.

2. Can I remove missed payments from my credit report?

Missed payments typically remain on your credit report for up to 7 years. However, you can dispute inaccuracies if the missed payment was reported in error. Contact the respective credit bureau (like CIBIL) and provide necessary documents to rectify the issue. For valid missed payments, you can request a "goodwill adjustment" from your lender, though this is not guaranteed.

3. Will paying off all my debts immediately fix my credit score?

Paying off debts is a significant step, but it won't instantly restore your credit score. While reducing outstanding balances and clearing defaults improve your credit utilization ratio and repayment history, the score rebuilds gradually over time as you demonstrate consistent, responsible credit behavior.

4. Is using a secured credit card a good option to rebuild my score?

Yes, secured credit cards are an excellent tool to rebuild your credit score, especially if you have a low score. These cards require a fixed deposit as collateral, making them low-risk for lenders. Using the card responsibly and paying the balance in full each month contributes positively to your credit history.

5. How does credit utilization impact my credit score?

Credit utilization refers to the percentage of your total available credit that you are currently using. A high credit utilization ratio (over 30%) indicates financial stress and can lower your score. Keeping your credit utilization below 30% demonstrates better financial management and contributes positively to your score.