When loan repayments start becoming difficult, many borrowers feel stuck. A sudden job loss, salary cut, medical emergency, or rising monthly expenses can make even one EMI feel stressed. In these situations, people often start searching for one practical question: how to negotiate personal loan settlement without making the situation worse.

It’s an understandable concern. When money is tight, the goal is not to avoid responsibility; it is to find a realistic way to manage it. But settlement is not something that should be rushed into. It involves talking to the lender, understanding the terms, checking the risks, and making sure everything is properly documented.

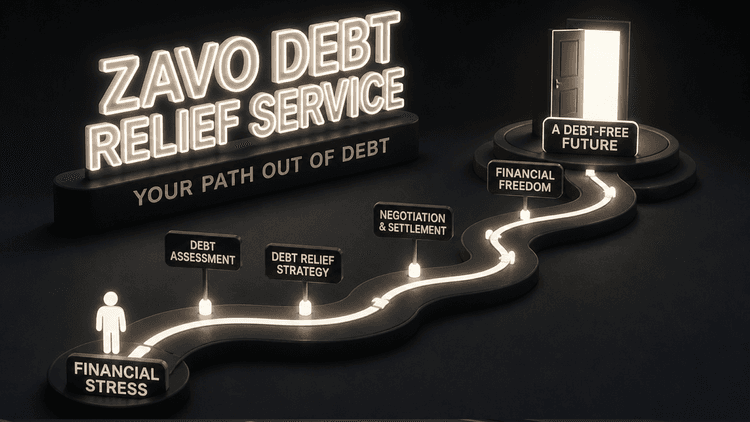

At The Zavo, we believe borrowers should first understand the process clearly before making any financial decision. That is why this guide focuses on simple, practical information. If you are trying to understand how to negotiate a personal loan settlement, this article will help you learn what it means, when it may be considered, how to speak with the lender, what mistakes to avoid, and what alternatives may be worth checking first.

What Does Personal Loan Settlement Actually Mean?

Before learning how to negotiate personal loan settlement, it is important to understand what personal loan settlement means.

A personal loan settlement happens when a borrower and lender agree to close the loan by accepting an amount that is less than the full outstanding balance. This usually happens when the borrower is facing genuine financial hardship and cannot continue repaying the loan through normal EMIs.

In simple words:

- You took a personal loan

- Loan repayments became difficult

- You could not continue the full EMI cycle

- The lender agreed to accept a reduced amount

- The account was resolved as settled, not fully paid

This last part matters a lot. A loan marked as settled is not the same as a loan marked as closed or paid in full. That is why borrowers should understand the long-term impact before starting a settlement discussion.

When Do People Usually Try to Negotiate a Personal Loan Settlement?

Most people do not take a personal loan expecting that they will need to settle later. Usually, this option comes up only when something serious changes financially.

Common reasons include:

- Sudden job loss

- Salary cut or unstable income

- Medical emergencies

- Business losses

- Multiple EMIs are becoming unmanageable

- Family emergencies

- Long overdue payments that are getting harder to recover from

In such cases, the borrower may feel that full repayment is no longer realistic in the short term. That is where understanding how to negotiate personal loan settlement becomes useful.

Still, settlement should usually be treated as a last-resort option, not the first one. If the issue is temporary, there may be less damaging alternatives such as EMI restructuring or a tenure extension.

How to Negotiate Personal Loan Settlement Step by Step

If you are seriously considering this route, the best approach is to stay calm and handle the conversation carefully. Personal loan settlement is not just about asking for a lower amount. It is about showing the lender that your hardship is genuine and that you want to resolve the matter practically.

1. Understand Your Current Financial Position

Before speaking to the lender, be honest with yourself.

Ask:

- Can I still manage EMIs with some adjustment?

- Is my problem temporary or long-term?

- Can I arrange a one-time amount from savings or family support?

- Is settlement the only realistic option right now?

This step matters because you need to know what you can actually offer. If you do not know your own limit, you may agree to something you still cannot afford.

At The Zavo, one of the most important things we encourage borrowers to do is to understand their repayment capacity before discussing any settlement amount. A rushed decision often creates more stress later.

2. Contact the Lender Early, Not Too Late

If repayments are already becoming difficult, do not wait until the situation gets worse.

Many borrowers delay the conversation because they feel embarrassed or afraid. But in reality, early communication often gives you a better chance of finding a structured solution.

When you speak to the lender:

- Explain why repayments have become difficult

- Mention if the hardship is temporary or ongoing

- Be clear that you want to resolve the loan responsibly

- Avoid emotional promises you may not be able to keep

2. Contact the Lender Early, Not Too Late

If repayments are already becoming difficult, do not wait until the situation gets worse.

Many borrowers delay the conversation because they feel embarrassed or afraid. But in reality, early communication often gives you a better chance of finding a structured solution.

When you speak to the lender:

- Explain why repayments have become difficult

- Mention if the hardship is temporary or ongoing

- Be clear that you want to resolve the loan responsibly

- Avoid emotional promises you may not be able to keep

If you are trying to learn how to negotiate a personal loan settlement, this is one of the most important points: communication matters more than silence.

Ignoring calls or delaying contact can lead to more penalties, more pressure, and fewer flexible options.

4. Never Rely Only on Verbal Promises

This is where many borrowers make mistakes.

Sometimes people receive calls from collection agents or informal representatives who pressure them to pay quickly. But when it comes to settlement, nothing should be treated as final unless it is documented.

Always ask for:

- Total dues outstanding

- Proposed settlement amount

- Payment deadline

- Official account details

- Written confirmation from the lender or authorised channel

- Clear mention that the payment is part of a final settlement arrangement

If you are researching how to negotiate a personal loan settlement, remember this clearly:

No written proof = no safe settlement

This is one of the smartest habits any borrower can follow.

5. Ask for a Proper Settlement Letter

Before making any final payment, ask for a settlement letter.

A proper letter should ideally include:

- Your loan account number

- Outstanding amount

- Agreed settlement amount

- Last date for payment

- Confirmation that the payment is treated as a full and final settlement

This is not a small formality. It is a critical part of the process.

At The Zavo, we always suggest that borrowers focus on documentation first. A well-documented settlement discussion is safer than a rushed payment made under pressure.

6. Make the Payment Through Official Channels Only

Once everything is clear and properly documented:

- Pay only to official lender-approved accounts

- Avoid cash transactions if possible

- Save bank receipts

- Keep screenshots, emails, or letters

- Store every proof carefully

After the payment is done, follow up and make sure the account status is updated properly.

What Should You Avoid During Personal Loan Settlement Negotiation?

If you are learning how to negotiate a personal loan settlement, knowing what not to do is just as important.

Common mistakes include:

- Waiting too long to contact the lender

- Trusting unknown agents without verification

- Paying based only on phone calls or WhatsApp messages

- Assuming settlement is the same as full closure

- Not checking the credit report later

- Agreeing to an amount you still cannot afford

A settlement should reduce financial pressure, not create a new problem.

Does Personal Loan Settlement Affect Your Credit Score?

Yes, it can.

This is the part many borrowers underestimate.

When a lender accepts less than the full outstanding amount, the account is often reported as settled instead of closed. That difference can matter in your credit history.

A settled account may lead to:

- Lower chances of future loan approval

- Extra scrutiny from lenders

- Higher interest rates later

- Smaller approved amounts

- More time needed to rebuild credit trust

This does not mean your financial future is finished. It simply means you should enter a settlement with full awareness.

That is why anyone trying to understand how to negotiate personal loan settlement should also understand the credit impact before agreeing to the final terms.

Are There Better Alternatives Before Settlement?

Sometimes, yes.

Before choosing a settlement, it is worth asking whether another option may solve the problem with less long-term damage.

Possible alternatives include:

- EMI restructuring

- Temporary lower instalments

- Extended loan tenure

- Short-term hardship support

- Partial payment arrangements

- Temporary relief options offered by the lender

If your problem is temporary, these options may protect your credit profile better than a settlement.

This is also where Zavo can be mentioned naturally in an informational way: borrowers often benefit from understanding the process, risks, and alternatives clearly before choosing a final path. The value is not in rushing toward settlement, but in understanding whether it is truly the right option for the situation.

Why Zavo’s Approach Feels More Practical for Borrowers

What makes Zavo feel useful in this topic is not just the idea of settlement itself, but the focus on clarity.

Borrowers dealing with repayment stress are often confused by:

- unclear terms

- pressure conversations

- credit score fears

- uncertainty about documents

- confusion between “settled” and “closed.”

That is why an informational, structured approach matters. At The Zavo, the strength of the platform is that it helps borrowers think through the process in a more organised way, understanding the risks, comparing alternatives, and looking at settlement as a serious financial decision rather than a shortcut.

That makes the topic more responsible, more educational, and more useful for the user.

Final Thoughts

If you are trying to understand how to negotiate a personal loan settlement, the most important thing to remember is this: settlement should be approached with patience, clarity, and proper documentation.

It may help when genuine financial hardship makes normal repayment impossible. But it is not something to enter casually.

Before moving ahead:

- understand your repayment ability

- Speak to the lender early

- ask for written confirmation

- avoid verbal-only promises

- Compare alternatives first

- know the credit impact

The smartest financial decisions are not always the fastest ones. They are the ones made with full understanding.

Frequently Asked Questions

1. What does personal loan settlement mean?

Personal loan settlement means an agreement between the borrower and lender where the lender accepts a lower amount than the total outstanding loan amount because the borrower is facing financial difficulty. After payment, the loan is usually marked as settled instead of fully closed.

2. How do I negotiate a personal loan settlement with the lender?

To negotiate a personal loan settlement, first understand your financial situation, contact the lender early, explain your repayment difficulty honestly, and ask if a settlement option is available. Always discuss only what you can realistically pay, and make sure the final offer is confirmed in writing before making any payment.

3. Does personal loan settlement affect my credit score?

Yes, personal loan settlement can affect your credit score. When a loan is marked as settled instead of closed, future lenders may see that the full repayment was not completed. This can reduce your chances of getting new credit easily.

4. Is personal loan settlement better than missing EMIs continuously?

In some cases, personal loan settlement may be a better option than letting unpaid EMIs keep increasing. However, it should usually be considered only after checking alternatives like EMI restructuring or repayment relief, because settlement can still affect your credit profile.

5. What documents should I ask for before agreeing to a personal loan settlement?

Before agreeing to a personal loan settlement, you should ask for a written settlement letter that clearly mentions your loan account number, total outstanding amount, agreed settlement amount, payment deadline, and confirmation that the payment will be treated as a final settlement. This helps avoid confusion later.