Did you know that one small error in your credit report could cost you thousands of rupees in higher interest rates or even lead to a loan rejection?

Imagine applying for a home loan and being denied because of a late payment mark that never actually happened. Mistakes in credit reports are more common than you might think, and they can have a significant impact on your financial health. The good news is that these errors are not permanent, and with a systematic approach, you can dispute them and potentially improve your credit score.

This blog walks you through everything you need to know about identifying, disputing, and preventing errors in your credit report, offering a comprehensive roadmap to safeguarding your financial future.

The Role of Your Credit Report in Financial Decisions

Your credit report is like your financial résumé. It’s a record of your borrowing and repayment behavior, providing lenders, landlords, and sometimes even employers with insights into your financial trustworthiness. The information in your credit report is used to calculate your credit score, which determines whether you qualify for loans, credit cards, and other financial products—and on what terms.

An accurate credit report can help you secure:

Loans with low-interest rates

-

High-limit credit cards

-

Favorable repayment terms on mortgages or personal loans

However, an error on your credit report could jeopardize these opportunities. For instance, an incorrectly reported late payment or a fraudulent account could lower your credit score, resulting in higher borrowing costs or outright rejections. This makes it critical to ensure that your credit report accurately reflects your financial history.

Common Errors Found in Credit Reports

Errors in credit reports are more frequent than many people realize. These mistakes can arise from data entry issues, reporting lapses by creditors, or even identity theft. Below are the most common types of errors to watch for:

1. Errors in Personal Information

Mistakes in your personal details might seem minor, but they can lead to confusion or mix-ups with other borrowers’ information. Examples include:

-

Misspelled names

-

Incorrect addresses

-

Outdated contact details

2. Account Errors

Errors in account details can have a direct impact on your credit score. Common issues include:

-

Accounts that don’t belong to you (due to mixed files or identity theft)

-

Duplicate accounts showing the same debt twice

-

Incorrect credit limits or balances

3. Payment History Mistakes

Your payment history is one of the most important factors in determining your credit score. Errors here can be particularly damaging, such as:

-

Payments marked as late even though they were made on time

-

Records of missed payments that never occurred

4. Outdated Information

Some information on your credit report is only supposed to remain for a limited period, such as:

-

Closed accounts still reported as active

-

Old debts that should have been removed after seven years

5. Fraudulent Accounts

If someone has stolen your identity and opened accounts in your name, these fraudulent accounts could severely damage your credit score. Identifying and disputing such accounts is crucial to restoring your financial health.

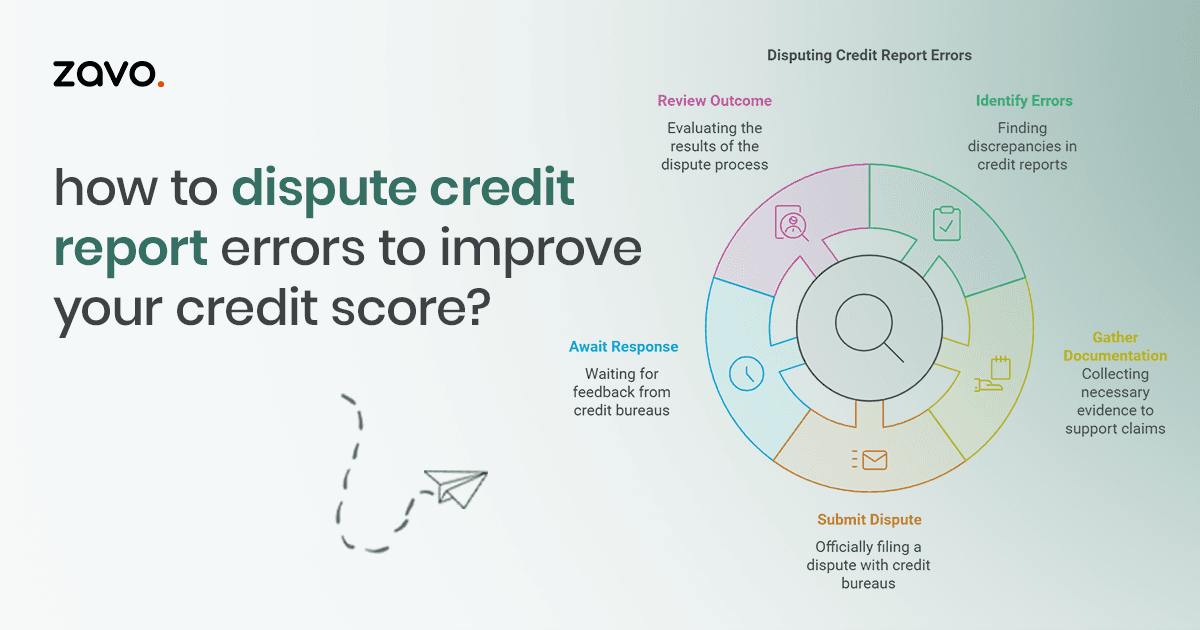

How to Obtain and Review Your Credit Report?

To dispute errors, you first need to identify them—and that starts with reviewing your credit report. Here’s how:

Step 1: Obtain Your Credit Report

In India, you are entitled to one free credit report annually from each of the four major credit bureaus:

- CIBIL

-

Experian

-

Equifax

-

CRIF High Mark

Request your credit report from all four bureaus, as each may have slightly different information. For convenience, you can access these reports online through their respective websites.

Step 2: Review the Report in Detail

Once you have your credit reports, examine them thoroughly. Pay close attention to:

-

Personal information (name, address, PAN, etc.)

-

Account details (account numbers, balances, credit limits)

-

Payment history (missed payments, late payments)

-

Negative items (defaults, collections, or judgments)

Highlight any discrepancies or entries that seem unfamiliar.

Step 3: Organize Your Findings

List all the errors you’ve identified and gather supporting documents that can help you dispute them. For example:

-

Bank statements to verify on-time payments

-

Loan closure certificates to confirm account status

-

Identity proof for correcting personal details

Step-by-Step Guide to Disputing Credit Report Errors

Correcting errors in your credit report is a multi-step process, but it’s manageable if you approach it systematically. Follow these steps to ensure a successful dispute:

1. Gather Evidence

Your dispute will be stronger if you can provide supporting documents. Depending on the nature of the error, this could include:

-

Bank statements showing payment dates and amounts

-

Correspondence with creditors about account closures

-

Police reports in cases of identity theft

Ensure you have both physical and digital copies of all evidence.

2. Contact the Credit Bureau

Each credit bureau has a specific process for handling disputes. Most offer online portals where you can file a complaint, but you can also submit your dispute via email or postal mail.

Steps to File a Dispute Online:

-

Visit the bureau’s official website.

-

Locate the dispute resolution section.

-

Fill out the dispute form, providing details about the error.

-

Attach supporting documents.

-

Submit your complaint and note down the reference number for future follow-ups.

3. Write a Dispute Letter

If you choose to file your dispute via mail, a detailed and professional dispute letter can make a significant difference.

Sample Dispute Letter:

Subject: Request for Correction of Errors in Credit Report

Dear [Credit Bureau Name],

I am writing to dispute an error in my credit report dated xx-xx-xxxx.

The specific error(s) I have identified include:

[Description of error, e.g., “Account No. xxxxx marked as late on [Date], but the payment was made on time as per the attached bank statement.”]

Enclosed are the relevant documents to support my claim. Kindly investigate the matter and update my credit report to reflect the corrected information.

Thank you for your prompt attention to this matter. I look forward to hearing from you within the legally mandated 30-day resolution period.

Sincerely,

[Your Name]

4. Contact the Lender or Creditor

If the error originates from a lender, such as a bank or credit card company, you’ll need to address it directly with them. Contact their grievance redressal team and provide evidence of the discrepancy. Resolving the issue at the lender’s level can speed up the correction process with the credit bureau.

5. Follow Up Regularly

Credit bureaus are required to resolve disputes within 30 days. During this period, they will investigate the error, often coordinating with the lender involved. Stay proactive by regularly checking the status of your dispute.

6. Verify Corrections

Once the dispute is resolved, request an updated copy of your credit report to ensure that the error has been corrected. If the issue persists, consider escalating your complaint to the Reserve Bank of India’s Ombudsman or seeking legal advice.

How Correcting Errors Can Improve Your Credit Score?

Disputing and correcting errors on your credit report can lead to significant improvements in your credit score. Here’s how:

1. Accurate Payment History: Late or missed payments can drastically reduce your credit score. Removing incorrect entries ensures that your payment history accurately reflects your reliability.

2. Improved Credit Utilization: Errors in account balances or credit limits can inflate your credit utilization ratio—a key factor in credit scoring. Fixing these inaccuracies can lower your utilization rate, positively impacting your score.

3. Elimination of Negative Items: Removing outdated or incorrect negative items, such as collections or defaults, can restore your creditworthiness.

4. Enhanced Creditworthiness: A higher credit score increases your chances of securing loans and credit cards with better terms, including lower interest rates and higher limits.

Tips to Avoid Future Errors

While disputing errors is essential, preventing them from occurring in the first place is even better. Here are some tips to safeguard your credit report:

1. Monitor Your Credit Regularly: Check your credit report at least twice a year to catch errors early. Many financial apps and credit monitoring services offer free or low-cost credit score tracking.

2. Protect Your Identity: Identity theft is a major cause of fraudulent accounts. Use strong passwords, avoid sharing sensitive information, and monitor your accounts for unauthorized transactions.

3. Communicate with Lenders: When closing accounts or settling debts, request written confirmation from the lender. This documentation can prevent reporting errors.

4. Maintain Good Financial Habits: Timely payments and responsible credit usage reduce the likelihood of errors or disputes.

Conclusion

Errors in your credit report are more than just an inconvenience—they can derail your financial goals. By proactively reviewing and disputing inaccuracies, you take control of your financial narrative and set the stage for better borrowing opportunities. Remember, a clean credit report isn’t just about numbers; it’s about peace of mind and the confidence to pursue your financial dreams.

Frequently Asked Questions (FAQs)

1. Can disputing errors harm my credit score?

No, disputing errors will not lower your credit score. It’s a consumer right protected by law.

2. What happens if my dispute is rejected?

If your dispute is denied, you can request a detailed explanation. Provide additional evidence or escalate the matter to the Reserve Bank of India’s Ombudsman.

3. How long does it take to resolve a dispute?

Credit bureaus typically resolve disputes within 30 days. However, complex cases may take longer.

4. Can I dispute errors on my own, or should I hire a service?

You can dispute errors independently at no cost. However, professional services can assist if the errors are complex or involve legal issues.

5. Will all errors be removed after a dispute?

Not necessarily. If the investigation finds the reported information accurate, the error will remain on your report.