If you've been searching for a debt relief app, chances are you're already under a lot of pressure, missed EMIs, non-stop collection calls, or a loan that's started to feel bigger than your entire monthly salary. You're not alone, and more importantly, you're not out of options.

What Is a Debt Relief App And What Can It Actually Do?

A debt relief app is a digital platform designed to help borrowers get out from under unmanageable loan or credit card debt. But the term is used very loosely. Some apps just remind you about EMI due dates. Some help you consolidate debt on paper. And then there are platforms that actually go to bat for you negotiating with lenders and helping you close the loan at a reduced amount.

That last category is what most people really need when they search for debt relief. Not a budgeting tool. Not a tracker. Something that actually reduces what they owe and gives them a real path out.

This is exactly where loan settlement comes in and it's one of the most underused yet effective options available to Indian borrowers today.

Why So Many Indians Are Struggling With Debt Right Now

India's digital lending market grew extremely fast over the last several years. Instant personal loans, buy-now-pay-later schemes, and easy credit card approvals meant that borrowing became very simple, sometimes too simple. People took loans during job losses, medical emergencies, or just to manage day-to-day expenses. And then the EMIs started piling up.

Today, a large number of borrowers are in a situation where they're either paying only the interest every month watching the principal never move or they've already started missing payments and are getting daily calls from recovery agents. The anxiety this creates is real. It affects sleep, relationships, and the ability to think clearly about a solution.

The good news is there is a structured, legal solution. It's not talked about enough, but it works.

What Is Loan Settlement and How Is It Different?

Loan settlement is when you and your lender mutually agree to close the loan at a lower amount than the total outstanding. Instead of continuing to pay EMIs indefinitely or letting defaults stack up, you make a one-time negotiated payment and the loan is officially closed.

This is completely legal in India. Banks and NBFCs actually prefer this over a long-running NPA (Non-Performing Asset) situation, because it recovers some value rather than none. So when a borrower genuinely cannot pay the full amount, many lenders are open to a settlement they just don't advertise it.

Most people don't know this is even an option. They assume they're stuck paying what the bank says, for as long as the bank says. That's not true. The outstanding amount on your loan is often negotiable, especially if you're already in default.

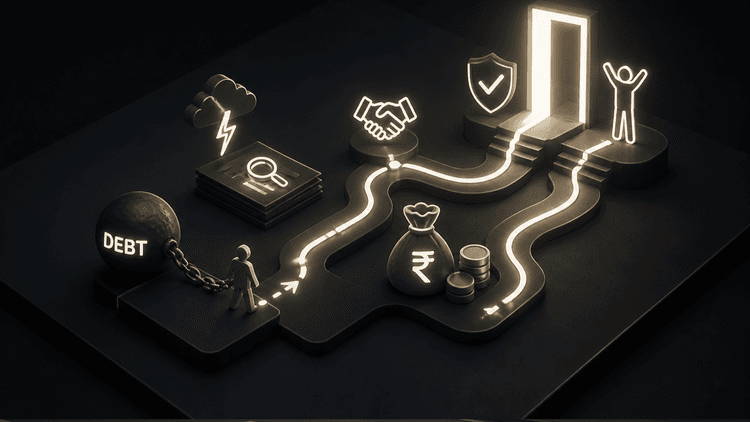

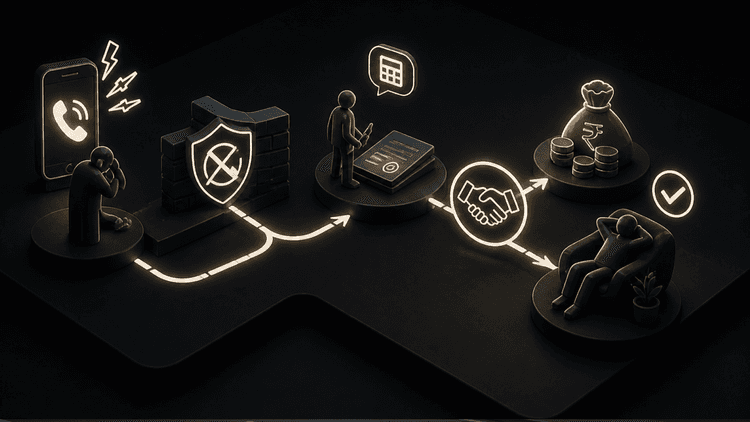

How the Loan Settlement Process Works Step by Step

The process is simpler than most people expect. First, you share your loan details with a settlement platform things like the lender name, outstanding amount, and how long you've been in default. The platform then evaluates your situation and figures out what a realistic settlement offer looks like for your specific case.

From there, the platform negotiates directly with your lender on your behalf. Once the lender agrees to a settlement amount, you make that payment and the loan is closed. The collection pressure naturally begins to ease as the process moves forward, because the lender can see a resolution is underway.

The whole thing is transparent; you know the offer before you commit to anything, and you only proceed when you're comfortable with the terms.

Key point: Loan settlement isn't the same as defaulting and disappearing. It's a formal, documented process that legally closes your loan. The lender issues a No Dues Certificate once settled.

Will Loan Settlement Hurt My CIBIL Score?

This is the question almost everyone asks first, and it deserves an honest answer. Yes a settled loan does show up as "Settled" on your CIBIL report rather than "Closed," and this does affect your credit score temporarily. But here's the part people miss: if you're already missing EMIs, your credit score is being damaged every single month right now.

Continued defaults are far more harmful to your CIBIL score than a settlement. Every missed payment gets reported. Every month you delay the damage compounds. Settlement, on the other hand, draws a line under the problem. It stops the ongoing harm and gives you a clean slate to rebuild from.

Most people who go through settlement are able to meaningfully improve their credit score over 12 to 24 months by responsibly using a secured credit card, maintaining a savings account, and staying on top of any remaining financial obligations. It's a reset, not a permanent mark.

How Zavo Helps You Settle Your Loan

Zavo's loan settlement service is built specifically for borrowers who are in genuine financial difficulty and need a real way out, not more advice, not more tips, but an actual resolution.

Zavo works directly with lenders, with no middlemen involved. There are no agents taking cuts in the middle. The negotiation happens between Zavo and your lender directly, which means the settlement offer you get is as clean and favourable as possible. Zavo also charges zero fees on a successful settlement meaning you don't pay anything unless the loan actually gets settled.

The platform has a 97% success rate and has served over 10 lakh verified users. Once your settlement process starts, collection pressure naturally begins to reduce as the lender is aware that a formal resolution is in progress. And there's even a cashback offer on successful settlement, something that's genuinely rare in this space.

Zavo handles both personal loans and credit card dues, so if you're drowning in either or both, there's a path forward.

Things to Keep in Mind Before You Choose Any Debt Relief Platform

The debt relief space has a mix of genuine platforms and ones that take your money without delivering results. Before you sign up anywhere, make sure you understand whether they actually negotiate with lenders or just give you advice. Ask them what their process looks like in writing. Find out if there are any upfront charges before any settlement has happened. A trustworthy platform should not charge you before delivering results.

Also ask specifically about the CIBIL impact and how they communicate with your lender throughout the process. Transparency is everything. If a platform can't clearly explain what happens at each step, that's a warning sign.

Final Thoughts

Searching for a debt relief app is often the first honest step someone takes after months of avoiding the problem. And it matters. The fact that you're looking means you're ready to find a way through, not just around.

Loan settlement isn't a shortcut or a loophole. It's a structured, legal process that thousands of Indians have used to close their loans, stop the collection pressure, and start rebuilding. If you're in genuine financial difficulty and the loan feels impossible to repay in full, it's absolutely worth exploring.

Frequently Asked Questions

What is a debt relief app?

A debt relief app is a digital platform that helps borrowers manage, reduce, or settle their outstanding loans and credit card dues often through loan settlement, restructuring, or direct negotiation with lenders.

Is loan settlement legal in India?

Yes, completely. Loan settlement is a mutual agreement between the borrower and the lender to close the loan at a reduced amount. Banks often prefer this over a prolonged NPA situation, making it a legitimate and common resolution path.

Does loan settlement affect my CIBIL score?

Yes, temporarily. A settled loan shows as "Settled" on your credit report, which impacts your score. But if you're already defaulting, your score is being damaged every month. Settlement stops the ongoing damage and gives you a starting point to rebuild.

How does Zavo help with loan settlement?

Zavo negotiates directly with your lender to settle your loan at a reduced amount, with zero middlemen and no upfront fees. The process is transparent, and collection pressure naturally eases once the settlement is underway.

Can I settle credit card debt too?

Yes. Zavo handles both personal loan settlement and credit card settlement, helping you close outstanding balances at an amount that works for your current financial situation.