Managing a loan becomes difficult when life takes an unexpected turn. A job loss, medical emergency, income drop, or rising monthly obligations can quickly make regular EMIs feel overwhelming. In situations like these, many borrowers start looking into personal loan settlement as a possible way to reduce pressure and close the debt.

At first glance, it may sound like a simple fix: pay a lower amount, settle the loan, and move on. But the reality is more nuanced. While personal loan settlement can offer short-term breathing room, it may also affect your credit score, future loan eligibility, and overall financial reputation.

That’s why it’s important to understand how it works before making any decision.

In this guide, we’ll explain personal loan settlement in simple language, how the process works in India, what impact it can have on your credit profile, and what alternatives you should consider first. The goal here is not to push a decision, but to help borrowers make a more informed one.

What Is Personal Loan Settlement?

Personal loan settlement is a process in which a borrower and lender agree to close the loan by accepting an amount lower than the total outstanding balance.

This usually happens when the borrower is facing genuine financial hardship and is unable to continue repaying the full loan amount through regular EMIs. Instead of recovering the entire dues, the lender may agree to accept a reduced lump sum as a final payment.

In simple words:

- You took a personal loan

- Repayment became difficult

- You could not continue paying the full amount

- The lender agreed to accept a reduced amount

- The account was closed as settled, not fully paid

This last point is extremely important because a settled loan is not the same as a closed loan in credit reporting.

Personal Loan Settlement vs Full Loan Closure

Many borrowers confuse settlement with full repayment. They are not the same.

When you repay every EMI and clear the full dues, the loan is generally marked as:

- Closed

- Paid in full

But when a lender accepts less than the total outstanding amount, the account is often reported as:

- Settled

That “settled” status tells future lenders that the original dues were not fully repaid.

This is why personal loan settlement is usually seen as a last resort option, not the ideal

When Do People Usually Consider Personal Loan Settlement?

Most borrowers don’t start a loan expecting they’ll need a settlement later. In most cases, it becomes relevant only after a major financial disruption.

Common situations include:

- Sudden job loss

- Salary cut or unstable income

- Medical emergencies

- Business slowdown or losses

- High debt burden from multiple EMIs

- Family emergencies or urgent expenses

- Long-term repayment delays are getting worse

In such cases, borrowers are not necessarily trying to avoid loan repayment. More often, they are trying to prevent a bad situation from becoming even more difficult.

Sometimes, people first look for options like restructuring or EMI relief, and only consider settlement if those solutions don’t fully solve the problem.

How the Personal Loan Settlement Process Works in India

The exact process may differ slightly from lender to lender, but the overall flow is usually similar.

1. Review Your Financial Situation Honestly

Before starting any discussion, understand your current repayment ability.

Ask yourself:

- Can I continue paying EMIs with some adjustment?

- Can I arrange a one-time amount from savings or family support?

- Is settlement my only option right now?

This step matters because lenders are more likely to respond when you can clearly explain your hardship and propose a practical resolution.

2. Contact the Lender Early

If you already know your repayments are becoming difficult, don’t wait too long.

The earlier you communicate, the better your chances of finding a structured path forward. Ignoring calls or delaying conversations can make things worse.

When speaking to the lender, explain:

- Why repayment has become difficult

- Whether the problem is temporary or long-term

- What kind of repayment can you realistically manage

In some cases, lenders may first explore temporary support, restructuring, or emi relief before moving toward a final settlement discussion.

3. Negotiate Carefully and Only Through Official Channels

This is where many borrowers make mistakes.

Never depend only on:

- Verbal promises

- Pressure calls from unknown agents

- Informal WhatsApp assurances

- “Pay now, paperwork later” instructions

During a personal loan settlement, always insist on clarity.

You should ask for:

- The total outstanding amount

- The proposed settlement amount

- Payment deadline

- Account details for payment

- Written confirmation from the lender or authorised channel

4. Get a Written Settlement Letter

Before making the final payment, make sure there is proper documentation.

A settlement letter should ideally mention:

- Your loan account details

- Total dues outstanding

- Agreed reduced amount

- Final payment deadline

- Confirmation that the payment will be treated as a full and final settlement

This is one of the most important steps in the personal loan settlement process. Never skip it.

5. Keep Payment Proof and Follow Up

After payment:

- Save bank receipts

- Keep emails or letters

- Download any payment confirmation

- Track the status update on your loan account

- Later, check your credit report to confirm the account has been updated correctly

What Happens to Your Credit Score After Personal Loan Settlement?

This is the part borrowers often underestimate.

While personal loan settlement can reduce immediate financial stress, it can also affect your credit history because the lender reports that the full dues were not repaid.

A settled account can be viewed differently from a fully repaid account.

Why “Settled” Is Different From “Closed”

In your credit report:

- Closed means you repaid the loan in full

- Settled means the lender accepted less than the full amount

That difference matters.

A settled status may lead to:

- Lower future loan approval chances

- Extra scrutiny from lenders

- Higher interest rates in future applications

- Lower credit card limits

- Longer time to rebuild trust in your credit profile

This does not mean your financial future is over. It simply means that personal loan settlement should be considered carefully, with a full understanding of the trade-offs.

Pros and Cons of Personal Loan Settlement

Every financial decision has two sides. It’s important to look at both before choosing a path.

Potential Benefits

A personal loan settlement may offer:

- Immediate reduction in repayment pressure

- A practical path when full repayment is no longer possible

- Faster resolution than prolonged default

- Relief from continued collection pressure

- Mental and emotional breathing room during a tough phase

Possible Drawbacks

At the same time, it may also bring:

- Negative impact on credit score

- A “settled” remark on the credit report

- Difficulty in getting future loans quickly

- Lower lender confidence in future applications

- The need for careful credit rebuilding afterward

So yes, personal loan settlement can help in the short term, but it should be seen as a structured recovery step, not a shortcut.

Common Mistakes to Avoid During Personal Loan Settlement

When borrowers are stressed, rushed decisions become more likely. That’s exactly why avoiding common mistakes matters.

1. Waiting Too Long to Communicate

Delaying the conversation can increase penalties, stress, and collection pressure.

2. Trusting Unverified Third Parties

Be cautious if someone promises guaranteed results without clear authorisation or documentation.

3. Paying Without Written Proof

Never transfer money based only on calls or informal messages.

4. Assuming Settlement Equals Full Closure

This misunderstanding creates long-term surprises later when borrowers apply for credit again.

5. Ignoring Credit Report Updates

After a personal loan settlement, always check whether the lender has updated the account correctly.

Alternatives to Consider Before Choosing Settlement

Before finalising personal loan settlement, it’s wise to check whether a less damaging option is still possible.

Depending on the lender and your situation, alternatives may include:

- EMI restructuring

- Temporary repayment support

- Lower monthly instalments for a period

- Extended loan tenure

- Partial payment arrangements

- Moratorium or hardship support (if available)

If the financial issue is temporary, these options may protect your credit profile better than a settlement.

This is why borrowers should treat personal loan settlement as one option among many, not the automatic default choice.

If you want to review structured loan settlement support options after comparing alternatives, make sure you understand the process and credit impact first.

Can You Get a Loan Again After Personal Loan Settlement?

Yes, but not always immediately.

After a personal loan settlement, some lenders may be more cautious. That can result in:

- Rejected applications

- Smaller approved amounts

- Higher interest rates

- Stronger income verification requirements

- Longer waiting periods before approval

Whether you can borrow again depends on factors such as:

- How recent the settlement was

- Your current income stability

- Your debt-to-income ratio

- Your repayment behavior after settlement

- Whether you rebuilt your credit profile responsibly

How to Rebuild Credit After Personal Loan Settlement

If you go through personal loan settlement, the next important step is recovery.

The loan may be resolved, but your credit journey continues.

Here are practical ways to rebuild:

- Check your credit report after the lender updates the account

- Make sure the status is accurately reflected

- Never miss future EMIs or card payments

- Keep credit card usage low

- Avoid applying for multiple loans at once

- Build a steady repayment record over time

- Focus on financial discipline instead of quick borrowing

Credit recovery takes time, but consistent behavior matters more than speed.

Final Thoughts

A personal loan settlement can be helpful when life creates a genuine financial crisis and normal repayment is no longer possible. It can reduce pressure, create breathing room, and help borrowers avoid an even deeper debt spiral.

But it’s not a simple shortcut.

Before choosing a personal loan settlement, borrowers should understand:

- How the process works

- What documents matter

- How it affects credit reporting

- Whether alternatives are still available

- What recovery steps will be needed afterward

The smartest financial decisions are not always the fastest ones. They are the ones made with clarity, documentation, and a long-term view.

If repayment stress is building, it helps to compare all available options carefully before making a final call.

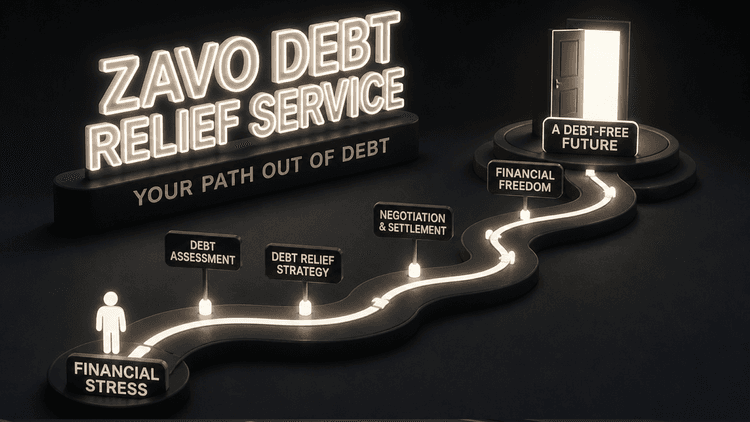

If you’re reviewing practical next steps, Zavo offers loan settlement support options designed to help borrowers understand structured resolution paths after comparing the process, risks, and alternatives.

Frequently Asked Questions

1. Is personal loan settlement legal in India?

Yes. It is a lender-approved resolution process where both borrower and lender agree on a reduced amount to close the account.

2. Is personal loan settlement a good option for everyone?

No. It is generally more suitable when there is genuine financial hardship and full repayment is no longer practical.

3. Does personal loan settlement affect CIBIL score?

It can affect your credit profile because the account may be reported as “settled” instead of “closed.”

4. Can I negotiate a personal loan settlement directly with the lender?

Yes. Many borrowers do this directly, but all terms should be documented in writing.

5. Is settlement better than ignoring the loan?

In many cases, a documented personal loan settlement is better than prolonged non-payment, but it still has consequences.