That one word “settled” can feel heavier than the debt itself.

You may have finally escaped the pressure of EMIs, recovery calls, and sleepless nights… but now a new fear begins: Will my CIBIL score ever recover?

If you’ve gone through a loan settlement, you’re not alone. Many people choose this path during financial hardship. The good news is that settlement is not the end of your financial journey. With the right steps, you can rebuild your credit profile, improve your CIBIL score, and regain lender trust.

In this guide, you’ll learn how to improve your cibil score after loan settlement, what the loan settlement process really means, and how platforms like Zavo can support you during this difficult phase.

What Is Loan Settlement?

Loan settlement happens when a lender agrees to accept less than the total outstanding loan amount as final payment. This usually happens when the borrower is unable to repay the full amount due to financial stress.

For example:

- Total loan due = ₹2,00,000

- Lender agrees to settle for = ₹1,20,000

- You pay ₹1,20,000

- The remaining amount is waived off

While this may bring immediate relief, the lender usually reports the account as “Settled” instead of “Closed” to credit bureaus.

That’s where the real problem begins.

Why Loan Settlement Hurts Your CIBIL Score

A debt settlement can negatively affect your credit score because lenders see it as partial repayment, not full repayment.

Closed vs Settled: What’s the Difference?

A closed loan means the borrower has repaid the entire loan amount, including all EMIs, exactly as per the original agreement. This status is usually considered positive or neutral in your credit report because it shows responsible repayment behaviour. In simple words, a closed loan tells future lenders that you managed your debt properly and completed repayment without any issues.

A settled loan, however, means the borrower could not repay the full outstanding amount and negotiated with the lender to pay only a part of it. The lender then marks the account as settled instead of closed. This can have a negative impact on your CIBIL score because lenders may view it as a sign of past repayment difficulty and higher credit risk. That is why many borrowers later search for how to improve their CIBIL score after loan settlement before applying for a new loan or credit card.

How to Improve CIBIL Score After Loan Settlement

Now let’s come to the most important part.

If your loan account has already been marked as settled, don’t panic. Here are the best practical steps to improve your credit score.

1. Check Your Credit Report Immediately

The first step is to download your latest CIBIL report and check all details carefully.

Look for:

- Loan marked as Settled

- Wrong overdue amount

- Duplicate entries

- Old loans still showing as active

- Closed accounts still open

Even a small reporting mistake can lower your score unnecessarily.

What to Do

- Review your credit report carefully

- Note any errors

- Raise a dispute with the credit bureau or lender if needed

Tip: Always check all major bureaus if possible, not just CIBIL.

2. Clear Any Remaining Dues

Sometimes, after settled loan, there may still be:

- Late payment charges

- Penalty fees

- Credit card balances

- Small pending EMIs

- Hidden charges not noticed earlier

If any dues are still unpaid, your score recovery will be slower.

Action Plan

- List all active credit accounts

- Clear any overdue balances

- Keep payment receipts safely

- Confirm the updated status after payment

If you truly want to know how to improve cibil score after loan settlement, start by removing all pending negatives from your profile.

3. Get a No Dues Certificate (NDC)

After the settlement process, never leave without proof.

Important Documents to Collect

- Settlement letter

- Payment receipt

- No Dues Certificate (NDC)

- Final written confirmation from the lender

This helps you because:

- It protects you from future disputes

- It proves the account is settled officially

- It helps if the lender reports incorrect data later

A proper settlement process should always end with documentation.

4. Try to Convert “Settled” to “Closed.”

This is one of the most powerful strategies.

If your financial condition improves later, contact the lender and ask:

- Can I pay the remaining waived amount?

- Can the account be updated from Settled to Closed?

If the lender agrees, this can improve how future lenders view your profile.

Steps to Follow

1 - Ask for the remaining amount in writing

2 - Pay through official bank channels

3 - Collect confirmation receipt

4 - Request a status update with the credit bureau

5 - Recheck your report after 30–60 days

Not all lenders allow this, but it’s always worth asking.

5. Start Rebuilding with a Secured Credit Card

After settlement loans, getting new unsecured credit can be difficult.

That’s why a secured credit card is often the best option.

Good Options

- FD-backed credit card

- Secured credit card

- Small secured credit line

Why It Helps

- Easier approval

- Builds fresh repayment history

- Shows lenders you can now manage credit responsibly

Best Usage Rule

- Use only 10% to 30% of your credit limit

- Pay the full bill on time every month

- Never miss the due date

This is one of the fastest ways to rebuild after settled loan

6. Keep Credit Utilization Low

Credit utilization means how much of your available credit you are using.

For example:

- Credit limit = ₹50,000

- Good usage = Below ₹15,000

- Best usage = Below ₹10,000

If you use too much of your credit limit, lenders may think you are financially dependent on borrowing.

Golden Rule

- Keep utilization below 30%

- Ideally stay under 20%

- Pay in full before the due date

Low utilization plays a major role in how to improve cibil score after settlement.

7. Never Miss Another EMI or Bill

From this point onward, your repayment discipline matters more than anything else.

Pay on Time

- Credit card bills

- Personal loan EMIs

- Buy Now Pay Later dues

- Consumer durable EMIs

- Auto loan EMIs

- Any co-borrowed loans

Smart Habits

- Enable auto-pay

- Set reminders 3–5 days early

- Keep buffer balance in your bank account

One missed payment after loan settlement can slow your recovery even more.

Loan Settlement Process: What You Should Know

Before anyone chooses debt settlement , they should understand the correct loan settlement process.

A Proper Settlement Process Includes:

1 - Review your total outstanding loan amount

2 - Talk to the lender directly

3 - Negotiate a realistic settlement amount

4 - Get the offer in writing

5 - Pay only through official channels

6 - Collect the settlement letter and NDC

7 - Track your credit report after settlement

Important Warning

Never:

- Pay in cash to unknown agents

- Accept verbal settlement promises

- Ignore written proof

- Assume the lender updated your report automatically

A safe loan settlement process protects both your money and your credit future.

When Do Settlement Loans Make Sense?

Settlement loans should usually be a last option, not the first.

It May Make Sense If:

- You’ve lost income suddenly

- You are facing severe financial hardship

- EMIs are completely unmanageable

- Recovery pressure is increasing

- Legal escalation is likely

- No restructuring option is available

It May Not Be the Best Choice If:

- You can still manage a revised EMI

- You can restructure the loan

- You can negotiate a temporary moratorium

- You can arrange part-payment without settlement

Always compare all options before choosing loan settlement.

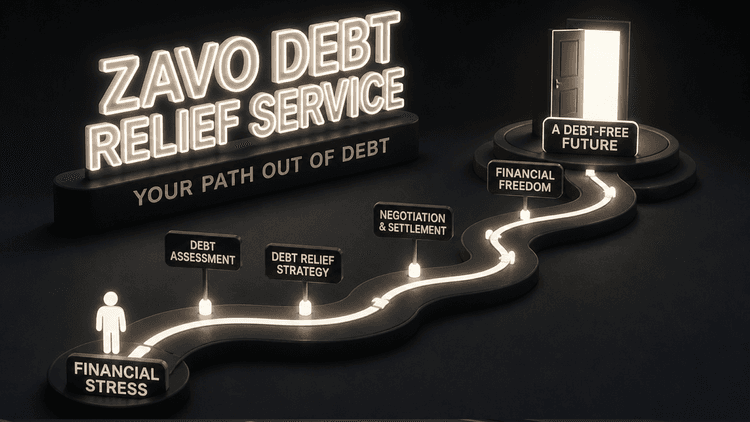

How Zavo Can Help in Loan Settlement

If someone feels confused, stressed, or overwhelmed during this stage, Zavo can be a useful support platform.

How Zavo May Help

- Support with the loan settlement process

- Help in understanding settlement options

- Guidance for managing EMI stress

- Structured support instead of handling lenders blindly

- Credit rebuilding support after loan settlement

Why This Matters

Many borrowers make mistakes because they:

- Settle without documentation

- Don’t understand the credit impact

- Ignore future recovery planning

A platform like Zavo can help make the process more organized and less emotionally draining.

Best Tips to Rebuild Your Score Faster

If you want a faster recovery after loan settlement, follow this 90-day plan.

First 30 Days

- Download credit report

- Verify settled status

- Collect all settlement documents

- Clear all remaining dues

- Stop applying for new loans

Next 30–60 Days

- Start using secured credit

- Keep utilization below 30%

- Set auto-pay for all bills

- Track updates in the credit report

Next 60–90 Days

- Build 2–3 months of clean payment history

- Avoid unnecessary credit inquiries

- Keep healthy old accounts active

- Maintain low spending on credit

Consistency is what improves your score, not quick tricks.

Conclusion

Loan settlement may close the immediate debt pressure, but it doesn’t have to close your financial future.

Yes, your CIBIL score may drop.

Yes, lenders may hesitate for a while.

But that doesn’t mean you’re stuck forever.

If you follow the right steps, check your report, clear dues, collect documents, use secured credit wisely, and never miss a payment you can absolutely recover. And if you need extra guidance, platforms like Zavo can help make the loan settlement process and recovery journey feel more manageable.

You survived the hardest part.

Now it’s time to rebuild stronger, smarter, and with more confidence than before.

Frequently Asked Questions (FAQs)

1. Can I improve my CIBIL score after loan settlement?

Yes, absolutely. While settlement hurts your credit score, regular on-time payments, low credit usage, and good credit habits can improve it over time.

2. How long does it take to improve the CIBIL score after settlement?

Most people may start seeing improvement in 6–12 months, while a stronger recovery can take 12–24 months, depending on repayment behavior.

3. Does a settled loan remain forever in the credit report?

No, but it can remain visible for several years. During that time, it may affect loan approvals and interest rates.

4. Is loan settlement better than default?

Yes. Loan settlement is generally better than leaving the loan unpaid completely. However, it is still worse than full repayment.

5. Is Zavo useful for loan settlement support?

Yes, if you need structured help with understanding the settlement process and managing your next steps, Zavo can be a useful option to explore.