Have you ever wondered why some people get loans approved instantly while others face rejections or higher interest rates?

The answer often lies in one crucial three-digit number—your credit score. Whether you're planning to buy a house, a car, or even secure a personal loan, your credit score plays a pivotal role in determining not only whether you qualify but also the terms of the loan.

In this blog, we’ll explore what a credit score is, why it’s critical for loan approval, and how it impacts loan terms. We’ll also provide actionable tips to improve your score, so you’re better positioned for future financial opportunities.

What is a Credit Score and Why Does It Matter?

A credit score is a numerical representation of your creditworthiness, typically ranging from 300 to 900 in India. It’s calculated based on factors like your payment history, credit utilization, length of credit history, credit mix, and the number of credit inquiries. Lenders use this score to assess the risk of lending to you.

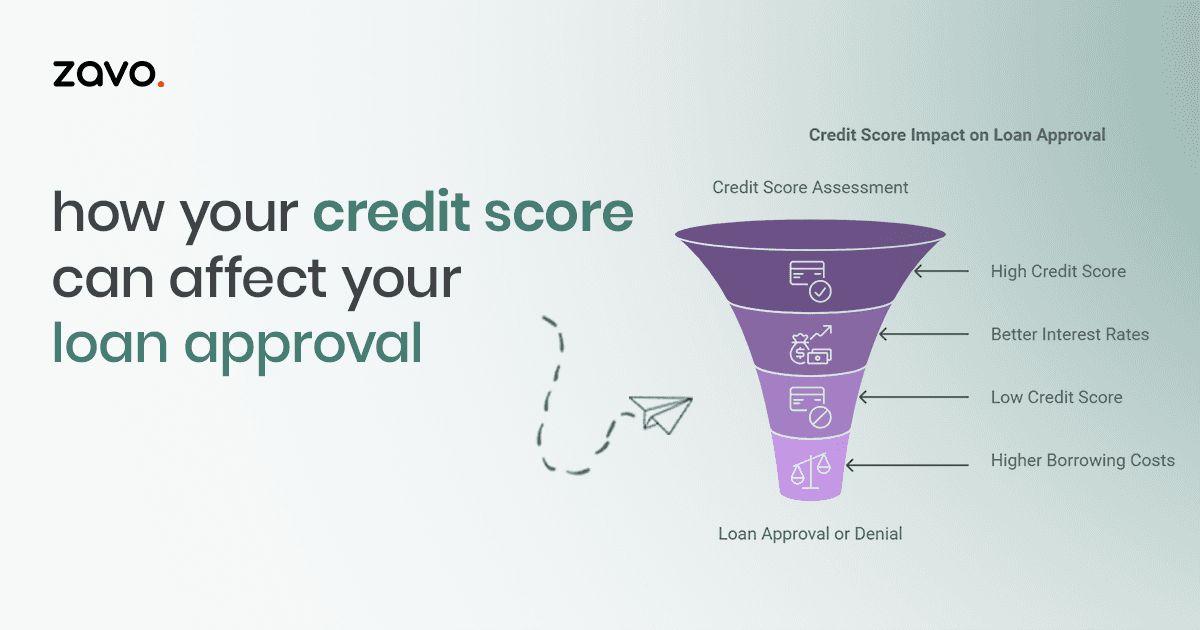

High Credit Score (750+): Indicates responsible financial behavior and increases your chances of loan approval with favorable terms.

-

Low Credit Score (<650): Suggests potential financial risks, making lenders hesitant to approve loans or offering them at higher interest rates.

Think of your credit score as a snapshot of your financial reliability. A strong score gives lenders confidence that you’re likely to repay the loan on time, while a poor score raises red flags.

How Credit Score Impacts Loan Approval?

1. Loan Eligibility: The first hurdle in the loan approval process is meeting the lender’s eligibility criteria, and your credit score is often the most critical requirement. A high score assures lenders of your financial stability, improving the chances of approval. Conversely, a low score can result in outright rejection or necessitate additional scrutiny, such as providing collateral or a guarantor.

2. Interest Rates: Your credit score doesn’t just influence whether you get approved—it also determines how much you’ll pay for the loan. Borrowers with high credit scores are typically rewarded with lower interest rates, which can save thousands over the loan term. For instance, a personal loan for someone with a 750+ score might have an interest rate of 11%, while someone with a 650 score might face rates of 16% or higher.

3. Loan Amount and Tenure: Lenders often cap the loan amount or shorten the repayment period for borrowers with low credit scores. For example, if you apply for a home loan but have a subpar credit score, the lender might approve only 70% of the requested amount instead of the full sum.

4. Loan Processing Speed: A high credit score can expedite the loan approval process. With automated systems and pre-approved offers, many lenders fast-track applications for individuals with excellent scores. On the other hand, a poor score may result in lengthy reviews, additional documentation requirements, or delays in disbursement.

The Role of Credit Score in Different Loan Types

1. Home Loans: For large-value loans like home loans, a good credit score is non-negotiable. Most banks and NBFCs (Non-Banking Financial Companies) in India require a score of at least 700 for approval. A higher score can fetch lower EMIs (Equated Monthly Installments), making home ownership more affordable.

2. Personal Loans: Personal loans are unsecured, meaning they don’t require collateral. Because of this, lenders heavily rely on your credit score to gauge risk. A score of 750+ improves approval chances and gets you better terms. Borrowers with lower scores may face outright rejection or higher interest rates.

3. Auto Loans: Auto loans are slightly more lenient as they are secured loans (the vehicle acts as collateral). However, a poor credit score can still result in higher interest rates or limited repayment tenure options.

4. Business Loans: For entrepreneurs seeking business loans, a personal credit score often becomes a deciding factor, especially for startups. A strong score not only helps in approval but can also unlock higher loan amounts for scaling operations.

5. Student Loans: While student loans often focus on future earning potential, a co-borrower’s credit score (usually a parent or guardian) can significantly impact approval and interest rates.

How to Improve Your Credit Score for Loan Approval?

If your credit score is holding you back from getting a loan, don’t worry—improving it is entirely possible with the right strategies:

1. Pay Your Bills on Time: Your payment history is the most significant factor affecting your credit score. Late or missed payments negatively impact your score. To improve this, set up reminders or automate payments for credit cards, loans, and other bills.

2. Reduce Credit Utilization: Credit utilization refers to the percentage of your credit limit that you’re using. For instance, if you have a credit limit of ₹1,00,000 and you’ve spent ₹50,000, your utilization is 50%. Aim to keep this below 30% to maintain a healthy score.

3. Avoid Frequent Credit Applications: Each loan or credit card application results in a hard inquiry on your credit report, which can lower your score temporarily. Limit applications to essential credit needs and space them out over time.

4. Diversify Your Credit Mix: Lenders prefer a mix of secured (like home loans) and unsecured (like credit cards) loans in your credit history. If you’re overly reliant on one type of credit, it could negatively impact your score.

5. Monitor Your Credit Report Regularly: Errors or inaccuracies in your credit report can drag down your score. Regularly review your report and dispute any discrepancies with the credit bureau to ensure your score reflects accurate information.

Common Credit Score Myths and Misconceptions

1. Checking Your Credit Score Lowers It: Many people avoid checking their credit score, fearing it might reduce the number. In reality, checking your own score is considered a soft inquiry and has no impact on your credit.

2. Closing Old Accounts Boosts Your Score: Closing old credit card accounts can reduce your credit history length, negatively affecting your score. Instead of closing accounts, aim to use them responsibly.

3. Zero Debt Equals a Perfect Score: While being debt-free is great, having no credit history can make it difficult for lenders to assess your creditworthiness. Using credit wisely and paying it off on time builds a positive credit history.

4. All Loans Have the Same Impact on Your Score: Different loans affect your score differently. For example, a default on a secured loan like a home loan may have a more severe impact than missing a credit card payment.

Conclusion

Your credit score is more than just a number—it’s a financial passport that determines your access to loans and credit. A high score opens doors to competitive interest rates, higher loan amounts, and faster approvals, while a low score can lead to limited options and higher costs.

By understanding the impact of your credit score on loan approvals and taking proactive steps to improve it, you can secure your financial future. Whether you’re aiming for a dream home, a new car, or a business expansion, a strong credit score is your key to unlocking better opportunities.

Managing your credit score can feel overwhelming, but tools like zavo make it simple and effective. With zavo, you can:

-

Monitor your credit score regularly without impacting it.

-

Get personalized tips to improve your score.

-

Access resources to build strong credit habits and achieve financial goals.

Download the zavo app today and take control of your credit journey, ensuring better loan approvals and financial stability!

Frequently Asked Questions (FAQs)

1. What is the minimum credit score required for loan approval?

Most lenders in India require a minimum score of 650-700 for loan approval. However, higher scores (750+) increase approval chances and offer better terms.

2. Can I get a loan with a low credit score?

Yes, but you may face higher interest rates, lower loan amounts, or the need to provide collateral or a guarantor.

3. How long does it take to improve a credit score?

Improving your credit score is a gradual process and can take 6 months to 2 years depending on the severity of issues and your financial habits.

4. Do different lenders view credit scores differently?

Yes, each lender has its own criteria for assessing creditworthiness. Some may focus on your overall score, while others consider specific factors like repayment history.

5. How can I check my credit score?

You can check your credit score through credit bureaus like CIBIL, Experian, or Equifax. Many banks and financial apps also offer free credit score checks.