If you are searching for debt relief India, it usually means you are dealing with financial pressure. Maybe your EMIs are increasing, interest is piling up, or recovery calls have started. This situation can feel stressful, but you are not alone.

Today, many people across India are struggling with personal loans, credit card bills, and app-based debts. Situations like job loss, medical emergencies, or business losses can quickly make repayments difficult. The important thing to understand is this: debt relief India solutions are real, legal, and available.

This guide will help you understand everything in a simple way, what debt relief means, your options, and how you can move towards a debt-free life.

What Is Debt Relief India?

Debt relief India refers to legal methods that help reduce or manage your loan burden. It does not mean your debt disappears completely, but it makes repayment easier and more realistic.

Debt relief can include:

- Reducing the total amount you owe

- Changing repayment terms

- Combining multiple loans into one

- Settling the loan for a lower amount

These options are designed for people who are unable to repay loans under normal conditions.

Who Needs Debt Relief India?

You may need debt relief India if you are facing any of these problems:

- You are taking new loans to repay old ones

- You have missed multiple EMIs

- Your EMIs are more than 50% of your income

- You have faced job loss or income reduction

- Your loan interest is increasing quickly

- You are receiving recovery calls regularly

If these situations sound familiar, it is time to consider a structured solution instead of waiting.

Debt Relief India Options You Should Know

There are different ways to handle debt. Choosing the right debt relief India option depends on your situation.

1. Loan Settlement (Most Popular in Debt Relief India)

Loan settlement is one of the most effective debt relief methods in India. In this process, you negotiate with your lender to close your loan at a reduced amount.

For example:

If you owe ₹1,00,000, you may settle it for ₹50,000–₹70,000.

After settlement:

- Your loan is closed

- Interest stops

- Recovery calls end

This is widely used for personal loans and credit cards.

2. Loan Restructuring

In this debt relief India option, the total loan amount remains the same, but repayment terms are adjusted.

This may include:

- Lower EMIs

- Longer repayment period

- Temporary relief

This works best if your financial problem is temporary.

3. Debt Consolidation

Debt consolidation is another debt relief method in India where you take one loan to pay off multiple debts.

Benefits:

- One EMI instead of many

- Better payment management

- Possibly lower interest

However, you need a decent credit score to qualify.

4. EMI Moratorium

A moratorium allows you to pause EMIs temporarily.

Important:

- It gives short-term relief

- Interest continues

- Total debt does not reduce

This is useful only in temporary financial stress.

5. Insolvency (Legal Option)

For very large debts, insolvency is a legal debt relief process in India.

However:

- It takes time

- Affects credit heavily

- Not suitable for small loans

Which Debt Relief India Option Is Best?

For most borrowers, loan settlement is the most practical debt relief solution in India.

Why?

- It reduces total debt

- It closes loans faster

- It stops the recovery pressure

Other options may not be possible if your financial situation is already difficult.

Signs You Need Debt Relief India Immediately

Many people delay action, which makes things worse. Here are clear signs you need debt relief in India right now:

- You have missed EMIs for 90+ days

- Recovery agents are calling frequently

- You have received legal notices

- Your debt keeps increasing

- You feel mental stress due to finances

If you are facing these, taking action now can save you from bigger problems.

Why Loan Settlement Works in Debt Relief India

Loan settlement is widely used in debt relief in India because it benefits both lenders and borrowers.

From the lender’s side:

- Recovering some money is better than nothing

From your side:

- You pay less

- Your loan closes

- You get peace of mind

Benefits of settlement:

- Reduced total payment

- No more penalties

- End of recovery calls

- Official closure (NOC)

- Fresh financial start

Does Debt Relief India Affect Your Credit Score?

Yes, using debt relief India methods like settlement can impact your credit score.

After settlement:

- Status becomes “settled.”

- The score may drop temporarily

However:

- Defaulting continuously damages your score more

- The settlement stops further damage

How to recover your score:

- Pay EMIs on time

- Use credit responsibly

- Avoid unnecessary loans

- Maintain low credit usage

Most people improve their credit score within 12–24 months.

How Debt Relief India Services Help You

Handling lenders alone can be stressful. Professional services make the debt relief process easier.

They help by:

- Understanding your situation

- Negotiating with lenders

- Getting better settlement deals

- Managing the process

- Helping close loans properly

This saves time, reduces stress, and improves results.

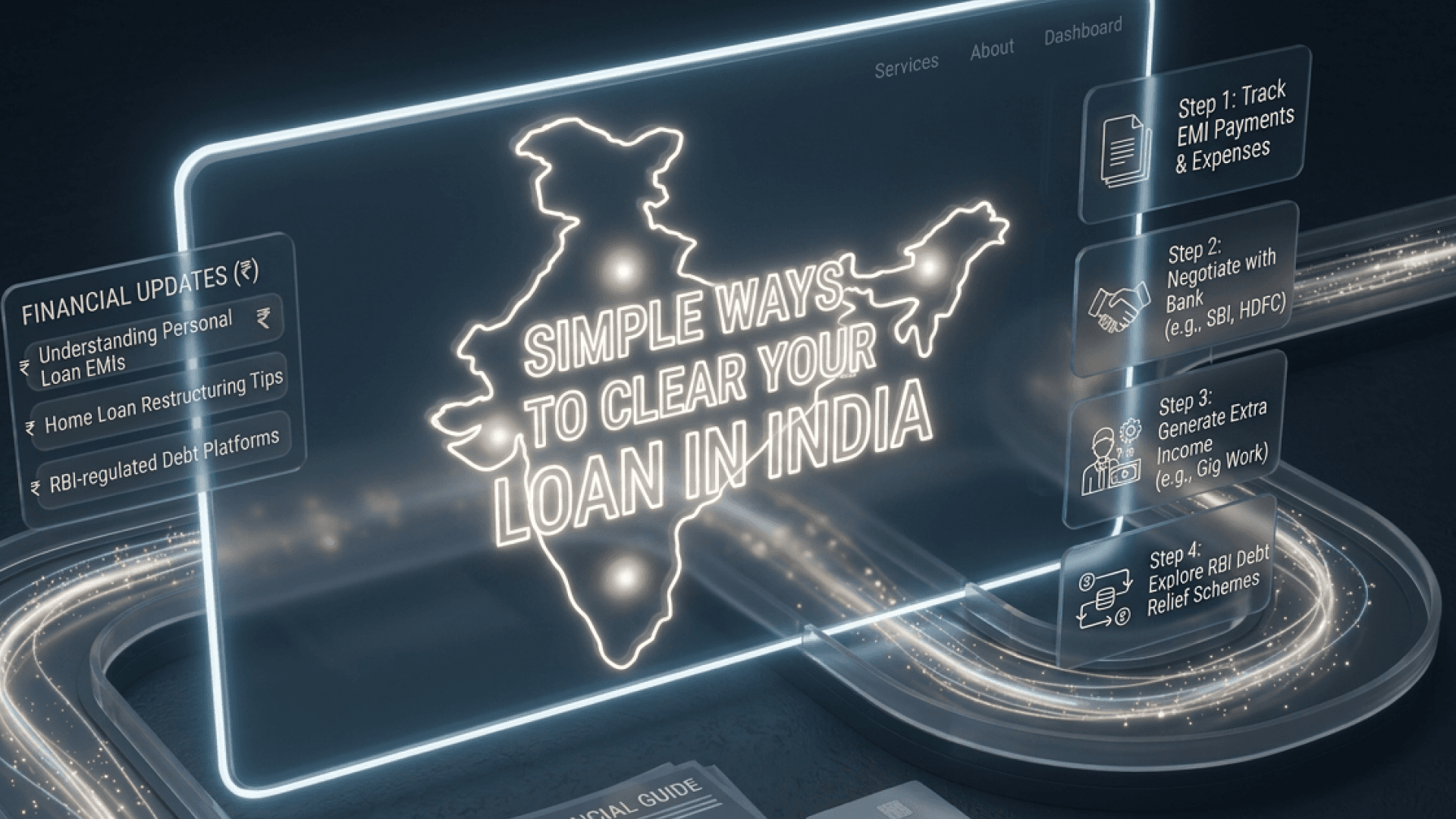

Step-by-Step Debt Relief India Process

Here is how the debt relief process in India works:

Step 1: Assessment

Your financial situation is reviewed

Step 2: Planning

The best solution is selected

Step 3: Negotiation

Lenders are contacted for settlement

Step 4: Agreement

The final amount is decided

Step 5: Closure

Payment is made, and the loan is closed

Final Thoughts

Dealing with debt can feel overwhelming, but it is not permanent. With the right debt relief India strategy, you can take control of your financial situation.

The key is to:

- Act early

- Choose the right option

- Stay consistent

Debt relief is not about avoiding responsibility; it is about finding a realistic way to move forward.

If your loans are becoming difficult to manage, starting your debt relief India journey today can help you avoid bigger problems tomorrow and move towards a debt-free future.

Frequently Asked Questions

Q: Is debt relief in India legal?

Yes, all debt relief India methods are legal and recognised.

Q: Will lenders agree to a settlement?

In most cases, yes, especially if loans are overdue.

Q: How much can I save?

Usually between 40% to 70% of the total amount.

Q: Will recovery calls stop?

Yes, they reduce during the process and stop after closure.

Q: Can I settle multiple loans?

Yes, each loan can be handled separately.